Did you know that Truthout is a nonprofit and independently funded by readers like you? If you value what we do, please support our work with a donation.

David Brooks, perhaps realizing that it was a bad idea to swallow a politician’s PR bullet points whole, is now backpedaling. The Ryan Plan, which he originally hailed as “the most comprehensive and most courageous budget reform proposal any of us have seen in our lifetimes,” now has the principal virtue of existing: “Because he had the courage to take the initiative, Paul Ryan’s budget plan will be the starting point for future discussions.”

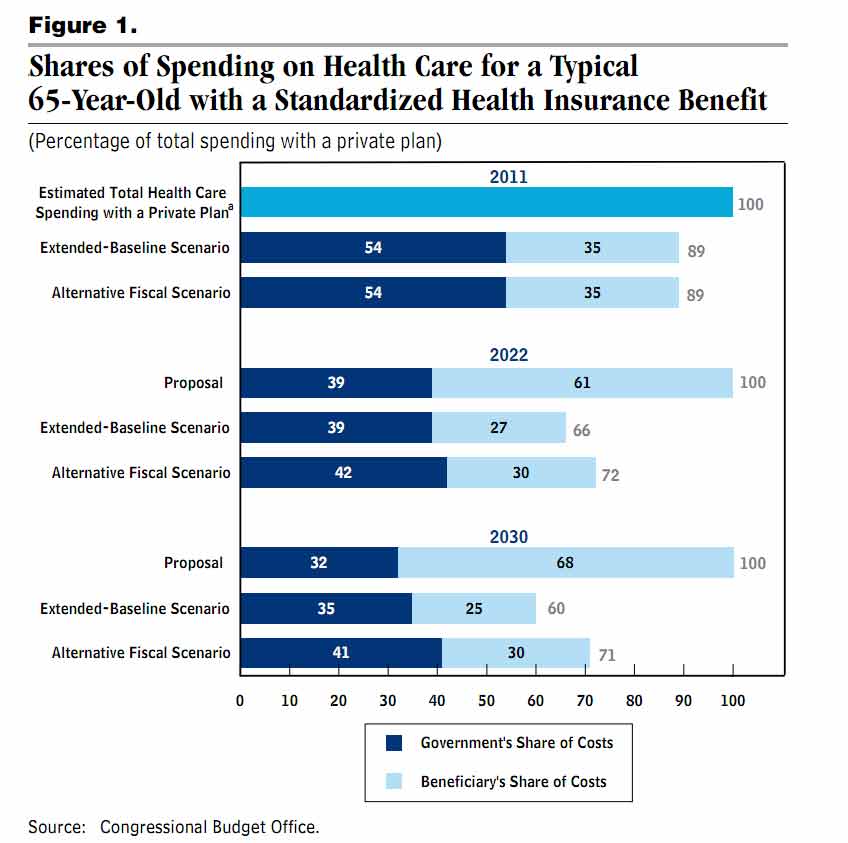

As I’ve discussed before, the Ryan Plan is just one bad idea dressed up with the false precision of lots of numbers: changing Medicare from a health insurance program to a cash redistribution program that gives up on managing health care costs. Here’s the key chart from the CBO report:

Click to view larger.

Click to view larger.Here’s how to read that chart. In 2030, under current law, a 65-year-old Medicare beneficiary’s health care will cost $60. (Obviously, this is using an index, not real dollars.) Medicare will pay $35 and the beneficiary will pay $25 in Part B premiums and cost sharing. Under the CBO’s more likely “alternative fiscal scenario,” her health care will cost $71, of which Medicare will pay $41. Under the Ryan plan, the same health care purchased in the private market will cost $100; “Medicare” will give her a $32 voucher, and she’ll pay the last $68 on her own.

The bottom line is that the Ryan Plan increases beneficiary costs more than it reduces government costs. In a weird sense, it’s a bizarrely pro-government plan: it helps the government’s bottom line at the expense of ordinary people.

So what should we do? Most importantly, we have to recognize that there are two separate problems, and they are not equal. The primary problem is health care inflation. The secondary problem is the long-term Medicare deficit. That’s a secondary problem because it’s largely a result of the primary problem.

Of these two, the Medicare deficit is the easier problem to solve: index the payroll tax to actual health care costs. This should automatically solve the Medicare deficit because as Medicare’s costs go up, its funding will go up at the same rate.[1]

This may sound like just raising taxes whenever the government wants to spend more. But the key is that the more taxes you pay, the more you get back. To see this, assume for now that Medicare is a pure price taker: it has no impact on health care costs but just has to pay what the market charges. Then, if health care costs go up by 5 percent, your taxes go up by 5 percent, but the expected value of your future Medicare benefits also goes up by 5 percent. You get all the insurance benefits of traditional Medicare, but now that insurance is worth 5 percent more, so you should be willing to pay 5 percent more.[2]

Raising taxes can have macroeconomic effects, but anything that solves the Medicare deficit problem will have macroeconomic effects: any solution involves either higher revenues or lower spending. Furthermore, increasing payroll taxes in line with health care costs is no different in substance than increasing premiums for employer-sponsored plans in line with health care costs, which has been going on every year for decades.

As commenter JD Johnson said previously, the assumption that Medicare is a price taker isn’t quite right because Medicare itself, as the largest insurance program in the country, has an impact on health care costs. So at the same time we should use Medicare to try to bring down system costs. But the question of bringing down overall system costs should be separated from the question of Medicare funding. And when it comes to Medicare funding, indexing the payroll tax to health care costs not only fills the budgetary gap, but it’s also fair: it maintains balance between the amount you pay and the value of your benefits. And most importantly, it balances the Medicare budget without eliminating the insurance benefits of Medicare, which are crucial to its long-term political support.

The primary problem — system costs — is harder, and I don’t have a better answer for that than the many health economists who have studied the problem. The first thing to point out, though, is that using Medicare to bring down system costs is exactly the approach of the Affordable Care Act — see Ezra Klein for all the details.

Robert Pear in the Times lists the following as some additional proposals in the air:

-

Increase the age of eligibility for Medicare to 67, from 65.

-

Charge co-payments for home health care services and laboratory tests.

-

Require beneficiaries to pay higher premiums.

-

Pay a lump sum to doctors and hospitals for all services in a course of treatment or an episode of care. The new health care law establishes a pilot program to test such “bundled payments,” starting in 2013.

-

Reduce Medicare payments to health care providers in parts of the country where spending per beneficiary is much higher than the national average. (Payments could be adjusted to reflect local prices and the “health status” of beneficiaries.)

-

Require drug companies to provide additional discounts, or rebates, to Medicare for brand-name drugs bought by low-income beneficiaries.

-

Reduce Medicare payments to teaching hospitals for the cost of training doctors.

I think those are all reasonable ideas except for #1. The problem with raising the eligibility age is that it makes the primary problem worse by shifting 65- and 66-year-olds from Medicare back onto their employers or into the individual market. I think #4 and #5 are the best, but the others should be on the table.

At the end of the day, we’re not sure how to bring down system costs, although lots of people have good ideas. The rate of cost growth will come down someday, one way or another; it’s not possible to have an economy that is 100 percent health care. My point is that while we’re trying to slow down health care inflation, as health care becomes more expensive, it makes sense for people to pay more for benefits that are becoming more valuable at the same time. It doesn’t make sense to eliminate the insurance component of Medicare because 2.9 percent is some magical ceiling dictated by the Founding Fathers.

My post earlier this week on the equivalence of tax increases and spending cuts received a large amount of criticism from the left because the example I used for illustrative purposes was increasing the Social Security payroll tax rate instead of eliminating the cap on wages subject to the tax. And there I was just trying to illustrate a principle. So this time I’m sure many people will object to the idea of raising the Medicare payroll tax, preferring to raise taxes on the rich instead.

In some abstract sense, I would prefer to raise taxes on the rich instead. But I think we should look other places rather than Medicare to make the tax system more progressive. Medicare, like Social Security, is a progressive system even though its taxes on their own are not. Because everyone gets the same benefit, there’s already a large amount of redistribution going on; in addition, that benefit is worth more to poor people, because they are less likely to have other sources of insurance. A flat percentage tax seems like a fair way to pay for it, but more importantly it’s the way we’ve paid for it for forty-six years, so for political reasons it doesn’t seem to me worth changing. Making the payroll tax itself progressive would also reduce political support for Medicare. If we want to “tax the rich,” we should do things like converting major tax deductions like the mortgage interest deduction into refundable credits or raising the tax rates on capital gains and dividends.

[1] There’s also the problem of Part B, which is funded by beneficiary premiums and general revenues. In principle, I think the answer is to increase the payroll tax to cover the contribution from general revenues and use the money freed up from general revenues to reduce some other tax in a progressive way (maybe extending the EITC phase-outs to reduce the super-high marginal tax rates that hit you as your earnings increase through the phase-out range). That has the benefit of strengthening the link between Medicare’s funding and costs, which is important for indexing.

[2] There is a demand elasticity issue, which is that as the price of health care increases the amount of it you want to buy may go down. I don’t have a perfect solution for this because Medicare is a one-size-fits-all program. But I think it’s mainly just a theoretical problem, for two reasons. First, the price elasticity of health care is very low, so the effect is small. Second, the fact is that when shopping today for an insurance plan that will cover you when you retire in the future, there is no other alternative that has a lower P and a lower Q. So given the alternatives that are actually available, forcing people to pay 5 percent more for a health care plan that’s worth 5 percent more does not deprive them of some other product they could buy that better suits their preferences.

Media that fights fascism

Truthout is funded almost entirely by readers — that’s why we can speak truth to power and cut against the mainstream narrative. But independent journalists at Truthout face mounting political repression under Trump.

We rely on your support to survive McCarthyist censorship. Please make a tax-deductible one-time or monthly donation.