Truthout is a vital news source and a living history of political struggle. If you think our work is valuable, support us with a donation of any size.

Contrary to the official story, Greece’s economy is not recovering, and the continuation of the Troika’s neoliberal austerity medicine assures the country a bleak economic and social future.

The official story about Greece is that its economy is recovering after being in the grips of a severe economic depression that has lasted six years, wiping out 25 percent of GDP and raising the official unemployment rate over 27 percent. The government points to the elimination of the current account deficit for 2013 (it is claimed that a primary surplus has been secured, which is the first one for Greece since 2002) as hard evidence that the economy is out of the woods. Thus, in spite of a government debt-to-GDP ratio which is hovering around 170 percent, the conservative Greek prime minister Antonis Samaras is confident that the debt level will become sustainable in 2014. Little wonder then that he has labeled the austerity experiment as a Greek “success story.”

To read more articles by C.J. Polychroniou and other authors in the Public Intellectual Project, click here.

This article not only debunks the myth of Greece as an economic “success story,” but shows that current trends and developments in the country make for a bleak economic future. The mindless austerity imposed on Greece by the European Commission, the European Central Bank and the International Monetary Fund – the so-called “troika” – as part of the bailout agreements has had a catastrophic effect on Greek economy and society while the policies of privatization and structural reforms including radical labor market restructuring have set the stage for the emergence of a type of economy in which economic inefficiency, brutal economic exploitation, severe inequality, foreign dependence and environmental degradation will be the primary characteristics. The claim made here is that the wild neoliberal experiment under way in Greece will produce an economy that will resemble features not of the Celtic Tiger of the mid-1990s to early 2000s – as the current government envisions – but that of an underdeveloped Latin American country of the 1960s.

Whether the conversion of Greece from a fairly developed economy into a colonial periphery is by design or not on the part of the nation’s international creditors is of secondary importance: This is the price Greece is paying for being a bankrupt nation as a member state of a currency union that has a deeply flawed institutional architecture and is being led by a hegemon that practices an extreme type of economic nationalism and “beggar thy neighbor” policies.

As long as Greece remains in the euro zone, and the euro zone remains what it is today, the country will most likely remain mired in its austerity trap for many years to come – with or without debt restructuring in the official sector. (Close to 90 percent of Greece’s public debt is now in the hands of the European Central Bank and of European governments). Even the IMF’s overly optimistic projections for a public debt-to-GDP ratio of 124 percent by 2020 imply commitment to fiscal discipline.

The current European Union is fully committed to antigrowth austerity policies, as reflected in various European laws, including the infamous Fiscal Compact. What it would take to reverse this situation is beyond the task of this article, but suffice it to say that European governments seem most determined to remain part of the euro zone under the current regime. In such an environment, euro zone member states that exhibit a proclivity for “fiscal profligacy” must be reformed by any means necessary or face the possibility of being forced out of the Euro area. This is clearly the story behind the drama that has been unfolding in Greece and the European Union since the outbreak of the global financial crisis of 2008.

A Cursory Look at Greece’s Fiscal Crisis under the Euro

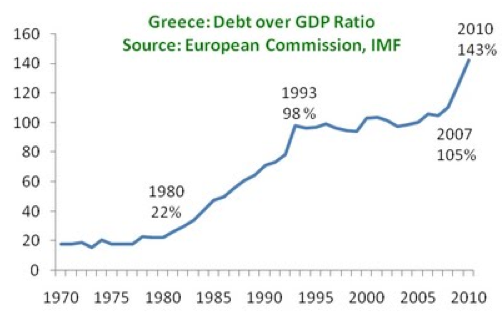

The economic problems of Greece that led to its bankruptcy have been attributed mainly to “fiscal profligacy,” a process aided by a deeply corrupt and inefficient political system. Indeed, the country lived beyond its means, if that what is meant by “fiscal profligacy.” As Figure 1 shows below, an upward trend in public debt started in the early 1980s, reaching its endgame in early 2010, when the country went bust and was forced into the arms of the “troika.”

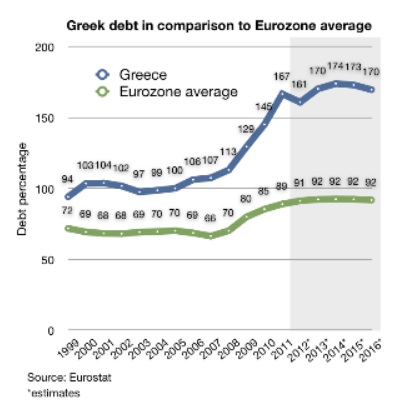

The “fiscal profligacy” argument in support of the cause behind Greece’s bankruptcy gains further credibility by the fact that Greece had by far the largest government debt in the euro area (Figure 2). And there is hardly anyone would deny the phenomenon of institutionalized corruption and the working of a kleptocratic state in contemporary Greece.

Nonetheless, Greece was allowed to enter the euro area with a government debt to GDP ratio that was already close to 100 percent, and its public debt load didn’t work its way up to unsustainable levels until the start of the global financial crisis. When it got close to the 130 percent mark in 2009 (Figure 2), the country was already in the midst of a major recession.

Thus, in spite of the high levels of public debt between 2001-2007, the Greek government was able to service the debt because the economy posted some seemingly impressive growth rates in real GDP, with an average of slightly less than 4 percent annually. With access to cheap credit, high growth rates were easier to attain for an economy with other severe structural economic weaknesses. Indeed, during the period under consideration, the yield on Greek 10-year bonds was just marginally higher (0.3 percent) than on their German counterpart. But the gap began to increase substantially by late 2009 and early 2010 – once the Greek deficit was discovered to have been double what it was originally believed to be (close to 13 percent of the GDP while later on it was revised to over 15 percent), with the public debt-to-GDP ratio standing close to 130 percent. By late 2010, the 10-year Greek government bond yield stood close to 12 percent.

The “growth performance” of the Greek economy had little to do with a dynamic capitalist economy. Growth relied on the twin pillars of state borrowing and European Union (EU) transfers. Between 2002-2006, EU transfers amounted to approximately 20 billion euros, which, according to some estimates, equals about 3.3 percent of annual GDP.

Of course, over-indebtedness and EU transfers to Greece represent only one side of the coin. The other side of the coin is the huge amount of funds paid to creditors. According to the Bank of Greece, for the seven-year period leading to 2004, Greece paid 208 billion euros to its creditors, and yet its debt did not decrease but rather increased, from 105 billion to 185.3 billion euros. This is the same ugly and vicious cycle of debt that many Latin American and other third world countries found themselves in at the height of western financial exploitation back in the 1960s and 1970s. Thus, by 2006, Greece had already posted the second largest public debt among the 27 EU member-states. In addition, Greece’s debt was mostly external. In 2009, Greece’s external public debt constituted 89 percent of GDP.

Greece’s fiscal woes were intensified by the huge discrepancy between expenditure and revenues. The data from show that the Greek government collected 7.9 percent of GDP from direct taxes when the average EU government collected 13.7 percent.

As further evidence of the weak foundations of growth in the Greek economy between 2001-2007, all-time historical levels of consumption were recorded in Greece (consumption reached close to 90 percent of GDP) by the early 2000s, but investment went down (it represented slightly over 20 percent of GDP). In plain economic terms, “this means that Greek citizens were consuming more, while less was spent on productive investment, such as factories and highways,” according to “The Economic Crisis in Greece: A Time of Reform and Opportunity,” a report by economists Costas Meghir, Dimitri Vayanos and Nikos Vettas.

Greece’s participation in the euro zone was imbricated in a host of other interesting and profound contradictions. Capital accumulation, for example, proceeded during the first five years of the country’s entry into the euro zone “at a rate which is equivalent to that of the growth of public deficit and debt rather than that of domestic consumption.”[1] Specifically, capital formation grew by 89 percent when domestic consumption registered a 39 percent growth. Thus, “this development deformed the real economy as capital formation developed, not in relation to the domestic and global market, but on the basis of the demands of finance capital.” In a similar vein, while labor productivity increased for the same five-year period by an average annual rate of 3 percent, real average wages increased by only 0.8 percent. [2]

In sum, Greek economic growth between 2001 and 2007 was largely based on overconsumption, ever-increasing debt levels, and a capital accumulation process divorced from the real economy. It was a period of economic growth in the midst of bubbles. Moreover, under the euro regime, Greece’s competitiveness declined by almost 25 percent – the icing on the cake to the nation’s participation in a currency union that has so far proven itself to be a massive failure. [3]

The Greek Bailout Disaster

Greece’s real problems with its participation in the euro zone began with the so-called “bailout” plan patched together by the European Union (EU) and the International Monetary Fund (IMF) when the country was effectively shut out of the international bond markets sometime in the spring of 2010 and faced the prospect of a default. Rushing to the judgment that the roots of the Greek financial crisis lay with a bloated public sector, the EU/IMF “bailout” plan involved a massive loan package accompanied by harsh antigrowth austerity measures at a time when the Greek economy was already shrinking as it found itself in the midst of a recession.

Specifically, the “bailout” plan that went into effect in May 2010 denied a bankrupt country the opportunity to restructure its debt, offering instead a massive loan package of 110 billion euros (at the usurious interest rate of 5 percent) to the Greek government that included onerous demands: a rapid fiscal consolidation program (intended to reduce deficits and the accumulation of debt) that hadn’t been seen in policymaking circles since the harsh economic adjustment program imposed by Ceausescu on the Romanians in the 1980s and a related set of economic policies based on long disproven assumptions (e.g., labor standards undermine competitiveness; flexible labor reduces unemployment; austerity boosts business confidence and generates growth – and privatization saves money). Accordingly, the structural adjustment and austerity programs implemented in Greece by the European Union (EU) and IMF featured sharp cuts in wages, pensions and social benefits; sharp increases in taxes; labor market liberalization; the blanket privatization of public assets and state-owned resources; and public sector layoffs.

Contrary to EU and Greek government propaganda, the “bailout” plan did not constitute an act of solidarity on the part of Greece’s EU partners and its financial backers. At stake were Europe’s banks, which were overexposed to Greek debt, and the stability of the euro. Even so, EU officials appeared quite confident in public that the bailout agreement would help Greece put its economy back on track in a relatively short time and allow it to return to international credit markets by the end of 2011 or early 2012. Of course, most economists across the ideological spectrum were not merely skeptical about the bailout deal, but actually thought that the measures that came attached to the rescue funds would sink the Greek economy into deeper recession.

The bailout agreement covered three years, with the plan’s primary objectives identified as lowering the deficit to 3 percent of GDP by 2013, restoring debt sustainability, achieving internal devaluation for the purpose of reducing domestic demand, improving competitiveness and increasing investments and exports. The fiscal consolidation strategy aiming to lower the deficit and restore debt sustainability involved a package of measures that amounted to 11 percent of the country’s GDP. With the corrections in place, the forecast called for the appearance of a primary surplus by 2012.

According to IMF expectations, the implementation of the structural adjustment program would allow the economy to quickly regain some of the competitiveness lost due to high labor costs and, after a slow increase, the debt would start declining after 2013. In the Memorandum of Understanding signed by Greece and its EU/IMF creditors, the Greek government was expected to carry out the required reforms with lightning speed, and the “troika” officials responsible for the supervision of the Greek structural adjustment program would review its progress on a quarterly basis to determine when the next installment of rescue funds (which were to be used exclusively for the country’s debt obligations) should be released.

This approach to dealing with a nation’s economic woes is rather typical of IMF thinking, which envisions a national economy being like a ship that can change course almost instantaneously at the command of its captain. As for the national culture, there was no reason why it could not be taken apart like a car engine and retooled in no time. The idea that the IMF has changed its philosophy and the tactics it pursues is hogwash. In fact, in spite of the much parroted claims of various senior-level officials that the organization has learned from its past mistakes and has altered the way it approaches nations in need of economic guidance and assistance, the mentality of the IMF (and its neoliberal acolytes everywhere) is still stuck in the era of the Pinochet regime in Chile, when guns and torture were widely used as means to enforce fiscal discipline and a “free-market” utopia on an otherwise unaccommodating nation. The IMF approach has failed everywhere it has been tried, in the process making a mockery of economic science and shredding democratic ideals and values.

From Latin America to Africa in the 1970s and 1980s, and from the former Soviet Union in the 1990s to Europe’s periphery today, the unfolding of the neoliberal experiment has produced a social dystopia, leading to lower economic growth rates, rolling back social progress and increasing inequalities. As was to be expected, the bailout deal of May 2010 turned out to be an EU/IMF fiasco and a Greek tragedy. Greece’s deficit shrank, but so did everything else – and in much greater proportions: employment, tax revenues, investment, consumer demand, and social and human services. The public debt increased substantially, and so did every index of economic misery and social malaise, including the spread of anti-immigrant extremism and waves of suicides related to economic hardship. But Greece’s financial partners had no interest in the social and economic consequences of the fiscal consolidation hoax they had perpetrated. All that mattered was attaining fiscal balance – that is, ensuring that the banks would keep on receiving payments for the Greek sovereign bonds they held.

The austerity-based fiscal adjustment program began to show catastrophic effects within a few months. Small-size businesses were shutting down at record levels, and unemployment had begun its upward spiral. In May 2010, the unemployment rate stood at 12 percent; by May 2011, it had jumped to 16.6 percent. The austerity measures were also having a major effect on tax revenues. In spite of repeated tax hikes – including across-the-board sales tax increases, a reduction in nontaxable income, and an emergency property tax on all homeowners – state revenues declined, with the pension and social insurance funds taking especially huge drops. According to the Greek Statistical Authority, state revenues for 2011 were lower than in 2009, “the year,” as some commentators acutely observed, “of the absolute fiscal derailing.” [4]

The May 2010 bailout agreement was to have been a one-time deal. Yet, even before the ink had dried, everyone (except the EU officials) could see that it was not going to be enough to help Greece overcome its crisis – and certainly not enough to stop the spread of contagion. Accordingly, Greek bond yields kept soaring to ever greater heights, freezing Greece out of the private financial markets for an indefinite period of time, and the bond vigilantes went on a safari for more fiscally wild “PIIGS.”

Nearing the end of the first two years of the bailout, euro zone finance ministers ended up approving a new rescue package deal for Greece worth 130 billion euros. Without the new bailout funds, the country would have defaulted. Interestingly enough, stocks fell when the announcement was made, as markets were quick to realize that, once again, the deal wasn’t going to solve the Greek crisis. By that time, Greece had already made the transition from crisis to catastrophe. Austerity was crushing the Greek economy and causing a slowdown in every peripheral euro zone economy that was implementing deep austerity measures in the midst of a major recession. But dogma is dogma and, as such, it has to be reinforced regardless of any empirical reality. Thus, the second bailout package included even more budget cuts across the board, the reduction of public employment by 150,000 by the end of 2015, and a massive privatization project – essentially an all-out neoliberal attack on public goods and all publicly owned enterprises in Greece. “A Nation for Sale” is how many Greek citizens have come to regard the terms and conditions included in the second bailout agreement. On sale, among other highly valuable state assets, are the ports of Piraeus and Thessaloniki; the Greek telecom OTE; the national lottery; prime real estate; and the postal bank. All at fire sale prices. [5]

Greece’s financial backers expected the privatization projects to raise 50 billion euros by 2015, revealing how wildly out of touch they were with Greek economic reality – although a more likely scenario is that the urgent push for privatization was simply a Machiavellian plan to transfer public wealth into private hands. After all, it is beyond contention that the Greek debt crisis has been utilized as an opportunity to dismantle the social state, to sell off profitable public enterprises and state assets at bargain prices, to deprive labor of its most basic rights, and to substantially reduce wages and pensions – all with the support of a significant segment of the Greek industrial/financial class and with the assistance of the domestic political elite, which, since the onset of the crisis, has relied heavily on dictatorial action to meet the demands of the country’s foreign creditors and to institutionalize a much-sought-after neoliberal economic order.

For the first two years of the first bailout agreement, EU leaders and the Greek government alike also made a mockery of any suggestion that Greece’s unsustainable public debt should be restructured, a move that should have been undertaken almost immediately after the crisis broke out. In May 2012, a debt restructuring deal was reached with most of the private investors, who, after Germany and the EU used some strong arm tactics, agreed to swap their government bonds for new securities worth less than half the previous securities. Greek government bonds held by the ECB were excluded from the “haircut.” As it turned out, this was yet one more move on the part of EU leaders to buy time, since the restructuring deal still left Greece’s debt at unsustainable levels (at around 132 percent), while placing new Greek bond issues under British law (hence the Greek Parliament cannot pass legislation refusing payment).

The terms of the second “bailout” out package accelerated the free fall of the economy and intensified the social decomposition that was underway, and, hence, Greece’s conversion from a fairly developed nation into a poor and dependent periphery. Greek GDP contracted by 6.4 percent in 2012, and dropped by another 5.6 percent in the first quarter of 2013. During the second quarter of 2013, the decline of the GDP was not as sharp at -3.8 percent, mainly because of an improvement in trade and tourism. Greek GDP is projected to post a decline of 4.8 percent for 2013.

In the meantime, the upward trend in unemployment continued, climbing from 24.2 percent in 2012 to 27.6 percent in 2013, the largest unemployment rate in all of the euro zone and at levels comparable to those that Greece had in 1961.

Thanks to the austerity measures, wages were slashed by close to 25 percent in the course of the past three years (purchasing power actually dropped by 37 percent), forcing in turn a reduction in domestic demand of 31 percent.

As for the public debt-ratio-to-GDP – which according to IMF forecasts would start declining by 2013 over its 2010 levels – not only did not shrink, but climbed to 170 percent (at 330 billion euros) by the end of 2013, leaving the nation permanently trapped in a state of peonage.

Primary Surplus: To What End?

The alleged Greek “success story” behind the austerity experiment in Greece rests exclusively on the elimination of the current account deficit and the recording of a small primary surplus, which, as of this writing, has yet to be verified. The attainment of a primary surplus is a key objective of the “troika” since it will allegedly help speed up Greece’s return to the international private credit markets (recall that according to the forecasts of the architects of the first “bailout” agreement, Greece was to return to credit markets by late 2011 or early 2012). However, the real reason for the “troika’s” obsession with a primary surplus is purely political: It serves as “evidence” that the austerity medicine works.

Greece’s current account began to decline by early 2012, and, by the end of that year, it had contracted by an amazing 72.9 percent in comparison to 2011. In actual figures, this meant a contraction of over 15 billion euros. The bulk of the contraction came from major declines in the trade deficit (7.6 billion euros) and in the income account deficit (6.4 billion euros).

While not necessarily a bad thing, ceteris paribus, the massive reduction in the current account of Greece in 2012 is intrinsically related to the deteriorating economic condition of the working people in the country, who have seen their wages slashed dramatically and their purchasing power sent back to mid-1990s levels. The alleged realization of a primary surplus for 2013 has been accomplished through the further deterioration of economic and social conditions.

Indeed, this is the main problem and the actual nature of the economic tragedy in Greece today. Instead of pursuing pro-growth, pro-employment policies, which would stimulate economic activity and put people back to work, the EU and IMF architects of Greece’s “bailout” plans opted from the beginning to impose draconian, neo-Hooverian policies on a crumbling economy. Indeed, facing a financing gap for 2015 and 2016, Greece will end up with yet another bailout agreement sometime by late 2014. Therefore, what purpose does a primary surplus serve in the midst of a crashing economy other than that of an ideological weapon to justify the insane policies of austerity?

The celebration over the primary surplus is nothing short of a desperate attempt on the part of the Greek government to cover up the catastrophic failure of the austerity experiment and hence of the bailout agreements with the European Union and the IMF. The Greek economy is not recovering by any stretch of the imagination, but remains under the firm grip of a major depression, though it is possibly slowing down after six painful years, with 2013 continuing in the rhythms set by the depression in 2011 and 2012, thereby proving how lethal the policies of austerity have been for Greece. Exports, for example, which apparently were to receive a major boost through the policy of internal devaluation, are struggling to make any inroads: in fact, in September of 2013, total exports amounted to 2.39 billion euros, while in September of 2012, they amounted to 2.44 billion euros, thus registering a decline of 2.2 percent.

The industrial production index in Greece, as recently reported by the Greek Statistical Authority, posted a decline of 6.1 percent between October 2012 and October 2013, while construction (one of the most dynamic sectors of the economy in the pre-crisis period) dropped by 36.6 percent between September 2012 and September 2013.

In the meantime, because of the severe budget cuts, the Greek public health care system has virtually collapsed, along with the nation’s public education system, thereby leaving no doubt that a failed state has emerged in contemporary Greece.

Finally, another great irony of the Greek “success story” is that the debt of the public sector has spread into the banking and private sector as well. Having received the sum of 50 billion euros in recapitalization from the government in order to keep them breathing, Greek banks are still unable or unwilling to provide much needed credit to businesses and consumers, claiming that they face a huge percentage of non-performing bad loans, which according to most estimates exceed 20 percent of all loans combined, and the figure is expected to rise in 2014-15. Greek banks will most likely need additional capital, and rather soon, thus increasing even further the public debt and, with the further deterioration of the overall economic climate, making it even harder for banks to help spur growth.

In sum, the future of Greek banks does not look any rosier than that of the overall Greek economy, and the likelihood that they will eventually pass into foreign hands is a rather strong possibility, although nationalizing them should be on top of the agenda of any Greek government dedicated to getting the economy out of the depression and avoiding the country’s conversion into a peripheral colony of the EU.

Future Prospects for Greece

Within the next 1-2 years, Greece may see the sharp and continuous decline of its GDP come to a halt. It would be a sign that the economy has reached rock bottom – not a sign of economic recovery, or that the path to growth has finally opened up. Any growth prospects for Greece remain dim without the implementation of a growth-oriented strategy. Some economists have proposed a new Marshall Plan for Greece, which under current conditions would be the only rational strategy to pursue for the sake of Greece and the future of the euro zone – but the current political leadership in Europe is unlikely to adopt such measures – unless it is politically forced to do so. However, the political situation in Europe is anything but promising, and developments inside a single nation alone will hardly carry enough force to compel a change of course inside the rest of Europe.

Yet, an objective observer would have a difficult time seeing how a nation like Greece can be sustained and remain a member of the euro zone if the policies of the last three-and-a half years continue. The stupendous rise in unemployment in Greece, for example, is the result of crude neoliberal policies, and the problem of lack of employment will not disappear with the refinement of these catastrophic policies, but rather with their abandonment. Even with a return to growth, the current levels of unemployment in Greece will never return to pre-crisis levels without the implementation of serious government-sector employment policies.

Indeed, the structural adjustment program underway in Greece will not lead to a growing and sustainable economy, and the empirical evidence is nowhere to be found that such programs have ever produced viable economies and decent societies. In Greece, in fact, they have already produced an economic and social disaster of historically gigantic proportions. One out of three Greeks is already near the poverty line, and in a recent poll, almost half of the population expressed the desire to leave the country. Greece is already on its way to resembling a Latin America country of the 1960s, and its condition as such cannot be reversed while the country is forced to go on carrying unsustainable government debt loads. Today’s European leaders are showing no sign of being willing to take the necessary steps to help Greece reduce its debt burden. In all likelihood, they won’t do so until the looting of the nation’s wealth has been completed.

Now, that would be a true neoliberal “success story”!

Footnotes:

1. Costas Vergopoulos, The Looting of Wealth (in Greek). Athens. A. A. Livanis, 2005, p. 75.

3. For a more detailed treatment of the political economy of Greece leading up to the nation’s financial crisis of 2010, but also including the impact of the bailout agreement that followed, see C. J. Polychroniou, “An Unblinking Glaze at a National Catastrophe and the Potential Dissolution of the euro zone: Greece’s Debt Crisis in Context,” Research Brief. Political Economy Research Institute, University of Massachusetts at Amherst, September 2011.

4. Yiannis Malkoutzis and Nick Moyzakis. Greece, Spain, Portugal Stare Into Abyss. Kathimerini (English edition). July 21, 2012.

5. See C. J. Polychroniou, “The Tragedy of Greece: A Case Against Neoliberal Economics, the Domestic Political Elite and the EU/IMF Duo.” Public Policy No. 1, 2013, Annandale-on-Hudson, NY: Levy Economics Institute of Bard College; and C. J. Polychroniou, “Failure By Any Other Name: The International Bailouts of Greece.” Public Policy No. 6, 2013. Annandale-on-Hudson, NY: Levy Economics Institute of Bard College.

Press freedom is under attack

As Trump cracks down on political speech, independent media is increasingly necessary.

Truthout produces reporting you won’t see in the mainstream: journalism from the frontlines of global conflict, interviews with grassroots movement leaders, high-quality legal analysis and more.

Our work is possible thanks to reader support. Help Truthout catalyze change and social justice — make a tax-deductible monthly or one-time donation today.