Did you know that Truthout is a nonprofit and independently funded by readers like you? If you value what we do, please support our work with a donation.

The Great Society is a place where every child can find knowledge to enrich his mind and to enlarge his talents. It is a place where the city of man serves not only the needs of the body and the demands of commerce but the desire for beauty and the hunger for community. It is a place where men are more concerned with the quality of their goals than the quantity of their goods.”

– Lyndon Baines Johnson

There are two important reasons for having a strong social safety net, one based in sound economic policy and the other in our common humanity. So it’s no surprise that the countries that have strong social safety nets tend to have resilient economies and a higher quality of life.

Ultimately, social safety nets are about managing risk and unforeseen contingencies. On the one hand, there are the risks that we want people to take, such as starting a new business. On the other hand, there are unforeseen events that are so severe – like becoming paralyzed in an accident – that no one person (unless incredibly wealthy) could handle the expenses associated with them. In both cases, by setting up a social safety net that distributes the costs of responding to them across the wide spectrum of society, we minimize both the societal cost and the individual suffering.

I’ve started seven businesses in my life, five of them successful enough that my wife, Louise, and I could sell them off, take about a year of retirement (better to retire when you’re young was our philosophy), and have enough left over to start the next company. In most cases, when we started the business we had no health insurance, even though in every case we had children.

But we were young and healthy and so were our children (one was a home birth whom I “delivered,” although Louise would rightly point out that she did most of the work), and so we did take what, in retrospect, seem like pretty dumb risks: for the initial year or two of setting up a business, we would have no health insurance for ourselves or our employees. We simply couldn’t afford it, and so we went without it until the business started earning enough money to pay for it.

Of course, this being the era from the late 1960s to the 1990s, health insurance was heavily regulated by most states, usually offered by nonprofit companies, and relatively inexpensive, so our “stupid” periods weren’t usually particularly long or dangerous. But that is no longer the case. Employer-sponsored health insurance costs have skyrocketed in the past decade, far above inflation or workers’ wages.

According to a Kaiser Family Foundation report, “between 1999 and 2009, health insurance premiums rose 131 percent, a much faster rate of increase than general inflation (28 percent) or workers’ earnings (38 percent).” The report also had this shocking statistic about the amount spent by employers on group health insurance policies: “The amount grew over twenty-fold from $25 billion in 1960 to $545 billion in 2008.”1

When premiums skyrocket, the usual response from the insurance companies is that they are simply passing along the increase in health-care costs to the consumers. And the corporate media never ask whether the profits of these insurance companies are also suffering. In reality they are making out like bandits, as a 2009 report from Health Care for America Now shows:2 Profits at 10 of the country’s largest publicly traded health insurance companies in 2007 rose 428 percent from 2000 to 2007, from $2.4 billion to $12.9 billion, according to U.S. Securities and Exchange Commission filings. In 2007 alone the chief executive officers at these companies collected combined total compensation of $118.6 million – an average of $11.9 million each. That is 468 times more than the…average American worker made that year.

What we have in America today is a trend of higher profits for insurance companies, higher premiums for employers and employees, and an increasing number of small-business owners and entrepreneurs worrying about the health-care costs of doing business.

But in every other developed country (and many that are considered below that threshold, like Costa Rica), entrepreneurs don’t have to take such risks. And the result is that the United States is being hammered in the area of innovation by countries that have stronger social safety nets. The Economist magazine recently published a study sponsored by Cisco Systems titled “A New Ranking of the World’s Most Innovative Countries.”3

During the period the study was conducted, every country in the top 20, including number 19, Slovenia, had a national health care system that covered every citizen regardless of employment – except the United States. Japan, Switzerland, and Finland beat us out, and right on our heels were Sweden, Germany, Taiwan, and the Netherlands. The study noted, “The high rank for three small wealthy European states reflects the fact that their economic, social and political conditions favour innovation….The slippage of the U.S. confirms the gradual erosion in recent years of that country’s traditional position as the world’s technological leader— a trend we expect to continue.”

The country that brought the world Thomas Edison and George Westinghouse and Andrew Carnegie has now slid in innovation, in part because of our lack of a strong social safety net.

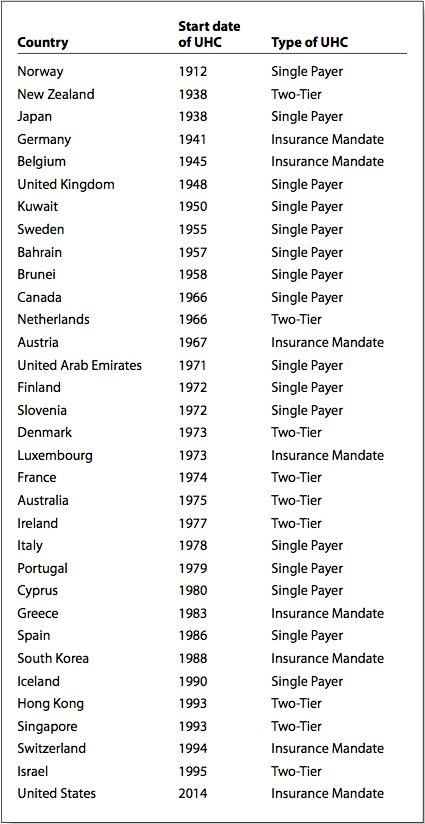

Praveen Ghanta, a Louisiana resident and a graduate of the Massachusetts Institute of Technology who runs the True Cost blog, notes that of the 33 acknowledged “developed” nations in the world, 32 of them have universal health care for all their citizens. The single exception is the United States. The other 32 countries have some version of universal health care: a single-payer system in which the government pays all bills; a two-tier system, where government provides basic coverage for everyone and nonprofit companies compete to offer high-end services to consumers; or an “insurance mandate” system, where the government requires everyone to have health insurance and insurers are barred from rejecting sick individuals (see sidebar).

Countries with Universal Health Care

The table on the facing page was developed in August 2009 by True Cost, a blog written by Praveen Ghanta. It shows that 32 of the 33 developed nations (those that ranked at 0.9 or higher on a 0-to-1 scale on the United Nations Human Development Index) have universal health care (UHC), with the United States being the lone exception. Note that universal health care does not imply government-only or even government-run health care, as many countries implementing a universal health-care plan continue to have both public and private insurance and medical providers.

Types of Universal Health Care

Single payer The government provides insurance for all residents (or citizens) and pays all health-care expenses except co-pays and co-insurance. Providers may be public, private, or a combination of both.

Two-tier The government provides or mandates catastrophic or minimum insurance coverage for all residents (or citizens) while allowing the purchase of additional voluntary insurance or fee-for-service care when desired. In Singapore all residents receive a catastrophic policy from the government coupled with a health savings account that they use to pay for routine care. In other countries, such as Ireland and Israel, the government provides a core policy, which the majority of the population supplements with private insurance.

Insurance mandate The government mandates that all citi- zens purchase insurance, whether from private, public, or non- profit insurers. In some cases, the insurer list is quite restrictive, while in others a healthy private market for insurance is simply regulated and standardized by the government. In this kind of system, insurers are barred from rejecting sick individuals, and individuals are required to purchase insurance to prevent typical health-care market failures from arising.

Source: Praveen Ghanta, www.truecostblog.com. Reprinted with permission.

As journalist and author T. R. Reid pointed out in his seminal 2008 documentary, Sick around the World, and in his subsequent book on the topic, The Healing of America: A Global Quest for Better, Cheaper, and Fairer Health Care, the United States is the only industrialized nation in the world that allows for-profit corporations to offer basic, primary-care health insurance. While many countries allow for-profit players in the insurance market, they’re specialized; the insurance will get you a single room or suite in a private hospital or covers things like elective cosmetic surgery – basically health insurance add-ons for the rich. But every other nation except the United States considers health care a right instead of a privilege, so they let only nonprofit companies provide insurance for it, or the nations’ governments provide it themselves.4

Thus the same inescapable conclusion: America should offer universal health care because it is sound economic policy, because it leads to better innovation in the business sector, and – most importantly – because it ought to be a basic human right in a modern, industrialized democracy.

The Obama Compromise

It took a full year for President Obama and the Democrats to push, pull, and shove through Congress a relatively modest set of changes in the way that health insurance is administered in the United States. The bill that Obama eventually signed on March 22, 2010—titled the Patient Protection and Affordable Care Act—had been sufficiently watered down so that it posed no threat to the profits of the insurance companies and the pharmaceutical companies. The changes were so benign from the point of view of the health insurance industry that its stock prices actually went up the day after the legislation was passed. Ditto for the drug giants.

President Obama was so fixed on getting “bipartisan” approval (he did get one Republican senator – Olympia Snowe of Maine – to vote for the bill in committee), that long before any bill came to a vote he embarked on a strategy to buy his own insurance, so to speak, for passage of the bill by addressing the concerns of the health insurance and pharmaceutical companies so that they would not lobby against it on Capitol Hill.

To buy their silence, if not their support, he made a series of major concessions: there would be no “public option” to compete with them to lower premiums (thus protecting insurance company profits and CEO salaries), there would be limits on importing drugs from abroad (thus protecting drug company profits and CEO salaries), and Medicare would be allowed to negotiate drug prices with Big Pharma only on a very limited basis over an extended period of time (more drug company profits). What’s more, the insurance mandate would send 30 million new Americans to the industry as customers. No surprise, then, that stock prices rose upon passage of the bill.

Reforming health insurance in the United States was probably a bigger job than reforming health care would have been. The reason is because the process required building entirely new structures of regulation and management. Such new laws and institutions required a supermajority of 60 of the Senate’s 100 senators to overcome a continuous filibuster, something the Republicans began using quite freely since Obama’s election.

Ironically, it’s much easier to expand an existing program. If legislation is considered in the Senate that only adjusts the amounts of revenue coming in or going out, it can be done through a process called “reconciliation,” which requires only a simple majority – 50 votes – to pass, with the vice president to break a tie.

For example, George W. Bush and the Republicans used reconciliation – majority rule – to push through his huge cuts in taxes on the richest Americans three different times in the first decade of this century. They were not creating a new program but simply adjusting the revenue figures. Ronald Reagan had done the same. If legislation has to do only with revenue or scale adjustments to existing programs, 50 votes in the Senate are enough.

Therein lies the greatest – and the simplest – opportunity to truly reform health care.

We already have Medicare, which is a fairly comprehensive basic health insurance/health-care program that covers nearly all Americans over 65 years of age. It is, in essence, a single-payer health-care program. Obama and the Democrats could easily push to expand the Medicare program to allow Americans of all ages to participate in it, and all they’d need is a simple majority, not a supermajority.

And here’s the most amazing part: this would be totally consistent with what President Lyndon B. Johnson and the folks in his administration and Congress had in mind when they created Medicare in July 1965.

The Birth of Medicare

Robert M. Ball was the commissioner of Social Security through the administrations of three presidents – John F. Kennedy, Lyndon B. Johnson, and Richard M. Nixon. He’d worked his way up in the Social Security Administration to become its head guy, spending 30 years of his life there; and then, after he retired, he was tapped by Ronald Reagan to be on the commission that, in 1983, overhauled Social Security to keep it solvent through the Baby Boomer retirement phase.

Medicare was established as an add-on to Social Security, not as a standalone program, so Ball was intimately involved in its creation as commissioner of Social Security throughout the Johnson years. He sat in on the meetings with members of the House and the Senate, he was involved in the writing of the Medicare legislation, and he was the man charged with helping implement it after LBJ signed it into law on July 30, 1965. He even ceremonially presented the first Medicare cards to Harry and Bess Truman.

Given his catbird seat during this entire process, Ball felt it important to put his recollections into the historical record, which he did in a 1995 article for Health Affairs journal titled “Perspectives on Medicare.” “Because I was deeply involved in the development, enactment, and implementation of the [Medicare] program,” he wrote, “my recollections may be of use in rounding out the historical record.” His article was appropriately subtitled “What Medicare’s Architects Had in Mind.”5

Perhaps the most important thing the drafters had in mind, Ball wrote, was that Medicare was the first step in a more far-reaching solution to America’s healthcare problem:

For persons who are trying to understand what we were up to, the first broad point to keep in mind is that all of us who developed Medicare and fought for it—including Nelson Cruikshank and Lisbeth Schorr of the AFL-CIO and Wilbur Cohen, Alvin David, Bill Fullerton, Art Hess, Ida Merriam, Irv Wolkstein, myself, and others at the Social Security Administration—had been advocates for universal national health insurance. We saw insurance for the elderly as a fallback position, which we advocated solely because it seemed to have the best chance politically. Although the public record contains some explicit denials, we expected Medicare to be a first step toward universal national health insurance, perhaps with “Kiddicare” as another step.

In his article Ball talks about how national health insurance had actually once been advocated by the American Medical Association (AMA), whose leaders “were favorably impressed by the systems that had been established in Germany (1883) and Britain (1911), and several other countries around that time.” This was 1916, he notes, and “ironically, much of the American labor movement in 1916 was opposed” to national health insurance, as “Samuel Gompers, president of the American Federation of Labor (AFL), preferred collective bargaining to political solutions and feared that if workers began leaning on government, they might begin to look generally in that direction, rather than to unions, for help.”

A decade later, Ball notes, the AMA and AFL positions had reversed and stayed that way up to and through the development of Medicare. The AMA was so vehemently opposed to government-offered health insurance that it even hired Hollywood actor and tobacco industry spokesman Ronald Reagan to produce an LP record titled Ronald Reagan Speaks Out against Socialized Medicine, which would be played at coffee klatches held by doctors’ wives nationwide to generate letters to Congress against the Medicare plan.

“The AMA’s opposition approached hysteria,” Ball wrote, noting that during the Truman administration the advocacy of the president for a national single-payer system so frightened the AMA that “members were assessed dues for the first time to create a $3.5 million war chest—very big money for the times—with which the association conducted an unparalleled campaign of vituperation against the advocates of national health insurance.” This was, he notes, “a warm-up for the later campaign against Medicare.”

So how did Medicare get passed?

Ball lays it out quite simply: old people were not profitable for the health insurance companies, so they were happy to get them off their rolls and onto the government’s. “[The elderly] used, on average, more than twice as many hospital days as younger persons used but had, on average, only about half as much income. Private insurers, who set premiums to cover current costs, had to charge the elderly much more, and the elderly could not afford the charges.”

This set the stage for Medicare, and the health insurance companies were at first enthusiastic about it. But in the final days of the development of the Medicare program, word got out that the people putting it together, including President Johnson, saw it as a system that could easily be modified to cover all Americans by the simple process of lowering the eligibility age, presumably incrementally over a decade or two. This pushed the insurance companies over the edge, prompting on their part a “fervent desire to keep government from penetrating further into the insurance business.” Ball adds, “Although most business groups opposed Medicare, the insurance industry was the AMA’s main ally [in that opposition].”

But because people knew and trusted Social Security, and this was just a health-benefit add-on to that existing program, it was easy to sell in Congress and to the American people. It was one of the most important legislative accomplishments of the Johnson administration.

It’s been more than 45 years since Medicare was legislated into existence, and it was established with the idea that one day it would be slightly tweaked to become the national single-payer health insurance program for the United States of America.

Medicare for All

So here we are, with a long-standing and successful Medicare program that everyone understands. Medicare has four parts: Part A covers hospital stays, Part B pays for medical services, Part C pays for private insurance coverage, and Part D covers prescription drugs.

It’s time now to create “Medicare Part E,” which covers “everybody.” Just let any citizen in the United States buy into Medicare.

It would be so easy. There is no need to reinvent the wheel with the so-called “public option,” which would mean setting up a whole new program from the ground up. Medicare already exists. It works. Some people will like it; others won’t, just like the Post Office versus FedEx analogy that President Obama has used so often.

Just pass a simple bill—it could probably be just a few lines, like when Medicare was expanded to include disabled people— that says that any American citizen can buy into the program at a rate to be set by the Centers for Medicare and Medicaid Services (CMS) and the Department of Health and Human Services that reflects the actual cost for us to buy into it.

Thus, Medicare Part E would be revenue neutral!

And as we saw earlier, if you are not creating a new program, with its own set of rules and regulations and management system, but only making changes to an existing program, you can get it through Congress with a simple majority and never face the threat of a filibuster or having to water things down to get enough votes for a supermajority.

To make it available to people with a low income, Congress could raise the rates slightly for all currently noneligible people to cover the cost of subsidizing families that live below 200 percent of the federal poverty level. Revenue neutral again.

This would blow up all the rumors about “death panels” and “pulling the plug on Grandma” and everything else: everybody knows what Medicare is. And nobody would be forced to enroll in Medicare. Those who scorn it and think of it as “socialized medicine” can give their hard-earned pay to United Healthcare so that it can pay its CEO $744 million in stock options. Those who like Medicare can buy into Part E. Simplicity itself.

Of course, we’d like a few fixes, like letting Medicare negotiate with pharmaceutical companies to get volume discounts on drug prices, and filling some of the other holes Republicans and AARP and lobbyists for Big Insurance have drilled into Medicare that now pretty much require people to buy “supplemental” for-profit insurance, but that can wait for the second round. Let’s get this done first.

And if this fails – if Congress can’t get out from under its corporate overlords – there is another solution embedded in the Obama legislation that passed in March 2010. Senator Ron Wyden of Oregon put into the health-care bill an amendment – which passed and is now law – titled “Empowering States to Be Innovative” that lets any state apply to the secretary of Health, Education, and Welfare (HEW) for a waiver from the national health insurance mandate program. The secretary has 180 days to deny the waiver with cause (Wyden can’t imagine what the cause may be other than perhaps there being a Republican in the White House appointing the HEW secretary). After that the state can start its own single-payer health-care system—with or without an insurance mandate, with or without a public option – so long as the state system meets or exceeds the coverage requirements of the federal legislation.

So far California’s legislature has twice passed a law to set up a statewide single-payer health insurance system, and Vermont did just weeks before this writing, in April 2010. In California’s case, Republican Governor Schwarzenegger twice vetoed the legislation, and the Vermont bill has not yet been reviewed by that state’s Republican governor for a signature or veto. But eventually some state will successfully pull this off.

This is how Canada moved into the modern health-care era, starting the same year that the United States was helping Germany and Japan write constitutions that declared health care to be a right rather than a privilege (although the Truman administration couldn’t get similar legislation through Congress when they submitted a single-payer plan in 1947).

In 1946 the province of Saskatchewan passed the Saskatchewan Hospitalization Act, which was a single-payer system for all citizens of the province covering all medical expenses that required hospitalization. Four years later the province of Alberta followed suit with a somewhat expanded program, creating a single-payer system called Medical Services (Alberta) Incorporated. In 1957 the Canadian federal government got into the act, and by 1961 all 10 provinces of Canada had joined in.

In the United States, Hawaii and Massachusetts have experimented with universal health care, although both had to do it during a time when federal laws made it difficult to impossible to start a true single-payer system, so in both cases the systems rely on the for-profit companies to administer the programs. Although the 2010 law didn’t do away with the for-profit health insurance companies’ antitrust exemption, it did, according to Senator Wyden, make it explicitly possible for any state to start its own single-payer system that, for the first time, excludes the for-profit leeches…er…companies.

Now we can all get active and mobilize to get our own states to set up single-payer systems that are far more inclusive and progressive than the watered-down federal legislation that became law in 2010.

Rebuild the Social Safety Net

If we address the health-care conundrum in America with a single-payer system that is fair and equitable, we will be patching a big hole in our social safety net. The importance of such a change is clear when we compare its impact on innovation and entrepreneurialism across the country with that of other nations that have already done this.

The Reagan experiment of suspending enforcement of the Sherman Antitrust Act wiped out small businesses across the land; college has become prohibitively expensive; health-care costs are out of sight; and our bankruptcy laws were rewritten by the banksters during the Bush Jr. administration to make it harder for entrepreneurs to declare bankruptcy and start over (as Henry Ford, P. T. Barnum, Milton Hershey, and J. H. Heinz all famously did and then bounced back to create successful companies).

The result is what Barry C. Lynn refers to as “the new monopoly capitalism” in America, a process that has turned this country from an entrepreneur’s dream into a neo-feudal state where almost all businesses are owned or controlled by a small handful of huge corporations, workers tremble at the specter of unemployment, and the middle class is being wiped out.

It’s ironic that the Tea Party populists, most of whom believe that they are furthering the American ideal of “rugged individualism,” are supporting mega-corporate-friendly policies like Reaganomics and Clintonomics and are making it very difficult for individuals to be anything other than drones in a giant corporate-run economic machine. And, on the flipside, those countries that call themselves “democratic socialist” in their organization – Finland, Germany, Japan, the Netherlands, Sweden – actually provide a deep and fertile soil into which entrepreneurs may plant new businesses.

Bankruptcy laws that protect innovators and risk-takers are good for entrepreneurialism: all those countries except the United States make it relatively easy to start over.

Not having to put yourself and your family’s health at risk to start a business is good for entrepreneurialism: all but the USA offer national health care that is not tied to your employer in such a way that you lose health insurance when you quit your job or your first attempt at a new business doesn’t succeed.

A strong social safety net is the most powerful way we can encourage innovation and entrepreneurialism. While ideologues will rant about the “dangers” of “big government,” the reality is that when government provides this sort of backstop, individuals like me—and a whole new generation of entrepreneurs—will step forward to innovate, build, and succeed.

Notes:

1. “Wages and Benefits: A Long-term View,” Kaiser Family Foundation, November 2009, https://www.kff.org/insurance/snapshot/chcm0 12808oth.cfm.

2. “Premiums Soaring in Consolidated Health Insurance Market: Lack of Competition Hurts Rural States, Small Businesses,” Health Care for America Now! May 2009, https://hcfan.3cdn.net/1b741c44183247 e6ac_20m6i6nzc.pdf.

3. Economist Intelligence Unit, “A New Ranking of the World’s Most Innovative Countries,” Economist, April 2009, https://graphics.eiu .com/PDF/Cisco_Innovation_Complete.pdf.

4. T. R. Reid, The Healing of America: A Global Quest for Better, Cheaper, and Fairer Health Care (New York: Penguin Press, 2009).

Notes 211 5. Robert M. Ball, “Perspectives on Medicare,” Health Affairs 14, no. 4

(1995), https://content.healthaffairs.org/cgi/reprint/14/4/62.pdf.

5. Robert M. Ball, “Perspectives on Medicare,” Health Affairs 14, no. 4

(1995), https://content.healthaffairs.org/cgi/reprint/14/4/62.pdf.

Thom Hartmann is a New York Times bestselling Project Censored Award winning author and host of a nationally syndicated progressive radio talk show. You can learn more about Thom Hartmann at his website and find out what stations broadcast his program. He is also now has a daily television program at RT Network. You can also listen to Thom over the Internet.

Copyright Thom Hartmann and Mythical Research, Inc. Truthout has obtained exclusive rights to reprint this content. It may not be reproduced, and is not covered by our Creative Commons license.

Want a copy of the book? Receive “Rebooting the American Dream: 11 Ways to Rebuild Our Country” as a thank-you gift with a donation of $35 or more to Truthout.

An urgent appeal for your support: 10 Days to raise $50,000

Truthout relies on individual donations to publish independent journalism, free from political and corporate influence. In fact, we’re almost entirely funded by readers like you.

Unfortunately, donations are down. At a moment when independent journalism is urgently needed, we are struggling to meet our operational costs due to increasing political censorship.

Truthout may end this month in the red without additional help, so we’ve launched a fundraiser. We have 10 days to hit our $50,000 goal. Please make a tax-deductible one-time or monthly donation if you can.