Support justice-driven, accurate and transparent news — make a quick donation to Truthout today!

Federal Reserve Chairman Jerome Powell and Treasury Secretary Steven Mnuchin have become the public faces of the $3 trillion federal coronavirus bailout. Behind the scenes, however, the Treasury’s responsibilities have fallen largely to the 42-year-old deputy secretary, Justin Muzinich.

A major beneficiary of that bailout so far: Muzinich & Co., the asset manager founded by his father where Justin served as president before joining the administration. He reported owning a stake worth at least $60 million when he entered government in 2017.

Today, Muzinich retains financial ties to the firm through an opaque transaction in which he transferred his shares in the privately held company to his father. Ethics experts say the arrangement is troubling because his father received the shares for no money up front, and it appears possible that Muzinich can simply get his stake back after leaving government.

When lockdowns decimated the economy in March, the Treasury and the Fed launched an unprecedented effort to buy up corporate debt to avert a freeze in lending at the exact moment businesses needed to borrow to keep running. That effort has succeeded, at least temporarily, with credit continuing to flow to companies over the last several weeks. This policy also allowed those who were heavily invested in corporate loans to recoup huge losses.

Muzinich & Co. has long specialized in precisely this market, managing approximately $38 billion of clients’ money, including in riskier instruments known as junk, or high-yield, bonds. Since the Fed and the Treasury’s actions in late March, the bond market has roared back. Muzinich & Co. has reversed billions in losses, according to a review of its holdings, with 28 of the 29 funds tracked by the investor research service Morningstar Direct rising in that period. The firm doesn’t publicly detail all of its holdings, so a precise figure can’t be calculated.

The Treasury is understaffed, and Muzinich was overseeing two-thirds of the department before the crisis hit. He spent his first year as the Trump administration’s point man on its only major legislative achievement, the landmark $1.9 trillion tax cut that mainly benefited the wealthy and corporations.

As the markets panicked about the economic impact of the coronavirus, Muzinich’s responsibilities expanded. The Treasury worked with the Fed on the emergency lending programs, and the agency has ultimate power to sign off. Muzinich was personally involved in crafting the programs, including the effort to bail out the junk bond market, The Wall Street Journal reported in April. He communicates with Fed officials daily by phone, email or text, the paper said.

That effort has many skeptics. The Fed has never bought corporate debt in its more than 100 years of existence, much less that of the indebted and fragile companies that raise money through the sale of junk bonds. Private equity firms, hedge funds and specialty investment firms like Muzinich & Co. dominate the market for junk-rated debt. In effect, the Fed has swooped in to protect the most sophisticated investors from losses on some of their riskiest bets.

Muzinich & Co. Profited From the Government’s Actions

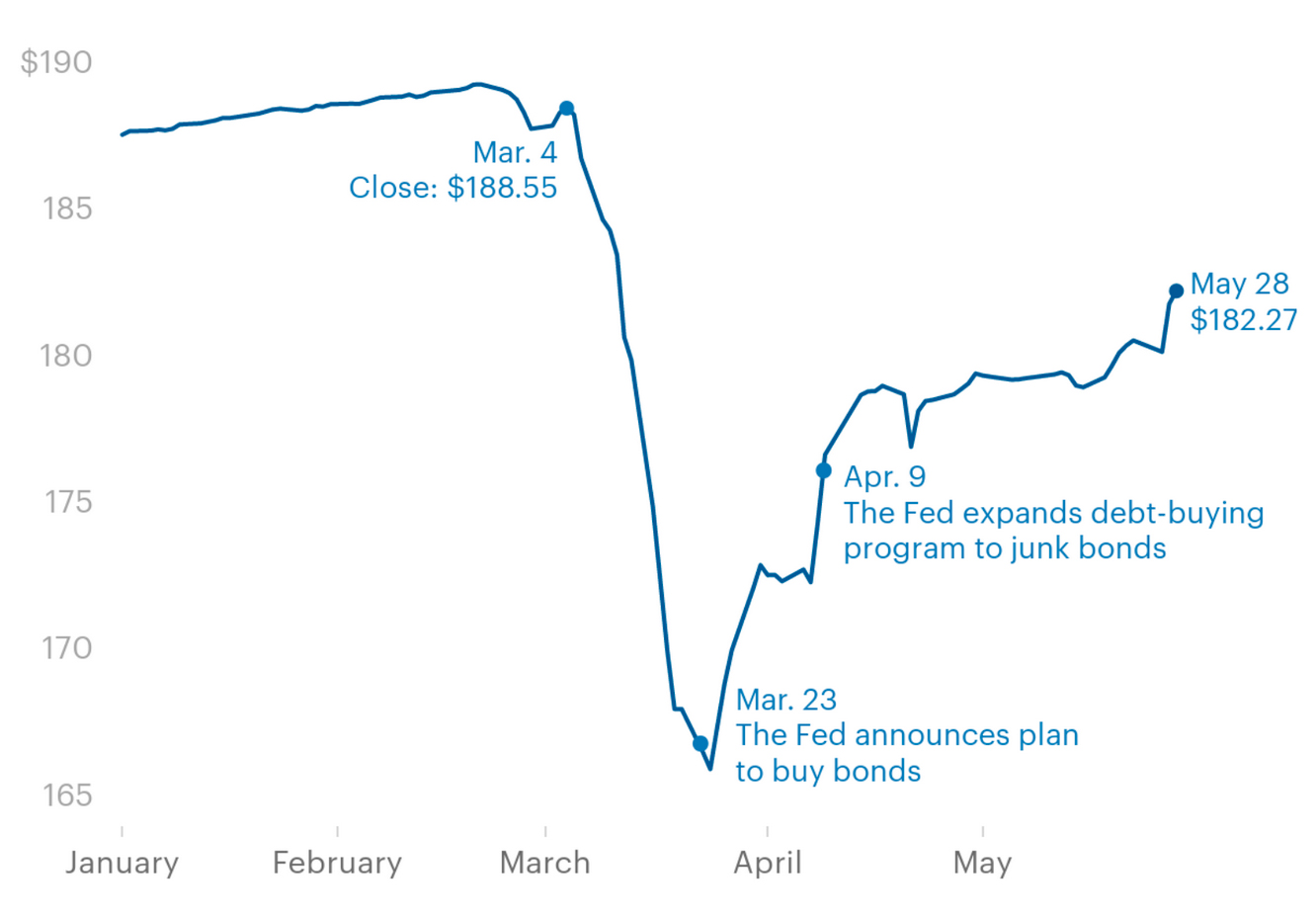

Muzinich & Co.’s largest fund, with over $10 billion in assets, jumped in value when the Treasury and the Federal Reserve announced plans to buy bonds.

Justin Muzinich’s ongoing ties to the family firm present a thicket of potential conflicts of interest, ethics lawyers said. Instead of immediately divesting his stake in the firm when he joined the Trump administration in early 2017, Muzinich retained it until the end of that year. But even then, he did not sell his stake and use the proceeds to buy broad-based securities such as index funds, as is common practice. Instead, he transferred his piece of the company to his father, who owns Muzinich & Co. In exchange, he received what amounts to an IOU — a written agreement in which his father agreed to pay him for the shares, with interest, but with no principal due for nine years.

“This is something akin to a fake divestiture,” said Kathleen Clark, a law professor and ethics specialist at Washington University in St. Louis. “It sure looks like he is simply parking this asset with a relative, and he will likely get it back after he leaves the government.”

A Treasury spokeswoman declined to say whether Muzinich has pledged not to take back the stake in the family firm once his public service ends. Muzinich “takes his ethics obligations very seriously” and “any suggestion to the contrary is completely baseless,” she said.

She added the arrangement with his family firm was approved by the Office of Government Ethics and agency ethics lawyers, who recently reexamined the setup given Muzinich’s role in the economic crisis response. They concluded that there is no currently envisaged scenario in which Muzinich would make decisions as a government official that would affect his father’s ability to repay the money he owes under the IOU.

“Treasury’s career Designated Agency Ethics Official has determined that there is no such conflict of interest, as there are no current or reasonably anticipated matters in which Deputy Secretary Muzinich would participate that would affect the note obligor’s ability or willingness to satisfy its financial obligations under the note,” she said in a statement. (The note obligor is Muzinich’s father.)

Muzinich & Co. did not respond to multiple requests for comment.

Muzinich’s relationship with the family firm also creates potential conflicts related to Muzinich & Co.’s clients. The firm makes money by charging investment management fees to several dozen wealthy individuals, insurance companies, pension funds, as well as what filings describe as a “quasi foreign government corporation.” The client list is not public and it’s unclear whether Muzinich would know about clients that came on board since he left. But any large investor has much to gain, or lose, from decisions being made by the Treasury about the bailout policies.

“The clients of this firm, I imagine, must be thrilled that Muzinich has this vitally important, powerful position with a huge amount of discretion and authority,” Clark said.

The Treasury spokeswoman declined to answer a question about the firm’s clients.

Even as Justin Muzinich has presided over bailout policies criticized by some observers, Muzinich & Co. executives have praised the government’s actions in recent briefings for investors. One described the interventions “as providing somewhat of a floor underneath the high yield market.”

Another Muzinich executive, David Bowen, who manages one of the firm’s high-yield bond portfolios, said during a May 20 webinar, “The Fed has been about as supportive, helpful, accommodative — whatever word you want to use — as anyone could imagine.”

Untangling the Financial Relationship

When Treasury Secretary Steven Mnuchin hired Justin Muzinich as counselor in early 2017, in many ways he was selecting a younger version of himself.

Like Mnuchin, Muzinich grew up in New York City, the son of a wealthy finance executive. Also like his boss, Muzinich spent years collecting a series of elite credentials: He attended Groton and holds degrees from Harvard College, the London School of Economics, Yale Law School and Harvard Business School. He worked at Morgan Stanley and spent a few months at a hedge fund associated with billionaire Steven A. Cohen, followed by a few years at EMS Capital, which invests the money of the wealthy Safra family.

Colleagues praise Muzinich as hardworking and serious, and Democrats have expressed relief that he isn’t as inflammatory as many other Trump appointees. Powell, the Fed chair, called Muzinich “creative and extremely capable” in a statement to The Wall Street Journal in April.

In 2010, he joined the family firm and became its president. His father, George, founded the company in 1988, specializing in handling portfolios of American high-yield bonds for European pension funds. The company expanded to offer funds to other institutional investors and wealthy individuals, but it stuck to its focus on corporate credit — particularly the riskier type that pays higher interest rates. Headquartered in New York and London, the firm has eight offices across Europe and one in Singapore.

“Talking about credit all the time might sound boring, I’m sure it does,” Justin Muzinich said in a 2014 interview, “but that is what makes you good.”

As he rose in the family business, Muzinich also launched himself into GOP policy circles, advising the presidential campaigns of Mitt Romney in 2012 and Jeb Bush in 2016. He owns a $20 million ultramodern beachfront house in the Hamptons and a $4.5 million Park Avenue apartment and commutes from New York City to work in Washington.

When Muzinich entered the Trump administration, he reported owning stock and stock options in the family firm collectively worth at least $60 million. The true value could be much higher, but disclosure rules don’t require officials to give a specific figure for any asset worth more than $50 million.

The Treasury’s ethics officers are frequently called on to rule on complex questions, given that the department tends to attract people from careers on Wall Street who have large, complicated financial holdings — from ex-Goldman Sachs Chairman Hank Paulson to banker and Hollywood financier Mnuchin.

Stakes in individual companies can create conflicts of interest. So incoming Treasury officials typically sell those stocks and invest in broad-based options like mutual funds. Ownership in private investment funds can be particularly thorny because ethics rules treat each of the fund’s investments in specific companies as sources of potential conflicts. Sarah Bloom Raskin, who preceded Muzinich as deputy secretary in the Obama administration, reported holding only a collection of index and mutual funds that either track the whole stock market or a large basket of companies.

But government ethics officials did not require Muzinich to sell his stake in the family firm through his first year in office as counselor to Mnuchin.

According to ethics filings, Muzinich said that he did not divest it until December 2017, the month the tax law was signed. (Several months later, in April 2018, Trump nominated him to be deputy secretary.)

Muzinich did not receive cash for most of his stake in the family firm. Instead, his more recent financial disclosures show that the stake, held in a family trust, was replaced with an opaque asset described as a “receivable from family,” valued at over $50 million.

Muzinich’s disclosure filings don’t reveal much about this asset at all. They don’t say who the family member is or explain the arrangement. They don’t say how the terms were negotiated, or even if the valuation of the deal was vetted by an independent third party.

It turns out that Muzinich transferred his stake to his father. But his father didn’t have to pay him right away. According to a Senate Finance Committee memo obtained by ProPublica, Justin received two promissory notes from his father in return for the shares. The notes pay Justin between $1 million and $5 million in interest over a year, at a rate of 2.11%. Moreover, his father does not have to pay any principal on the loan for nine years.

Neither the financial disclosure forms nor the Senate memo say how long the agreement is supposed to last. Neither addresses the possibility of his getting the shares back after he leaves the government. The Treasury says the transaction is “not reversible” but did not elaborate.

In other words, Justin still has an ongoing long-term stake in the financial well-being of Muzinich & Co., since his father now owes him more than $50 million. If the company were to plummet in value or even go under, it could cost Justin. Actions the Treasury and the Fed take can either enhance the chances he gets his money back or lower them.

The Treasury defended the IOU transaction as an appropriate remedy for any conflicts of interest. The agency provided a statement from Elizabeth Horton, an ethics attorney who left the agency in 2019 and who worked with Muzinich on the divestiture from his family business. Horton said that when Muzinich first joined the agency, “the Treasury ethics office correctly advised him that he did not need to divest his holdings in his family business because of the generalized nature of his work on tax reform legislation.” She said that when his duties changed, “I advised Mr. Muzinich that an exchange for a fixed value note was an appropriate way to divest.”

Horton said that advice was “consistent with practice in previous administrations” — though the Treasury declined to cite similar cases. “Muzinich worked very closely with the ethics office and was extremely attentive to his ethics obligations,” Horton said.

ProPublica reached out to four ethics officials, including two former Treasury ethics lawyers. None could recall a similar divestment transaction. Three of the four disagreed that it resolved Muzinich’s conflicts, while one said that turning it into an asset with a value that doesn’t fluctuate with future developments should shield him from any allegations of impropriety.

The deal does not look like an arms-length transaction, said Virginia Canter, who served as a career ethics attorney at Treasury during the George W. Bush administration and is now at the watchdog group Citizens for Responsibility and Ethics in Washington.

“The terms of the loan suggest something less than a bona fide transaction,” she said. “Once he leaves office, nothing in the arrangement appears to preclude Muzinich from forgiving the debt owed to him by his father so they can amicably agree on returning to Muzinich the interest in the Muzinich family business.”

As ranking member of the Finance Committee, Sen. Ron Wyden opposed Muzinich’s nomination as deputy secretary because of his role in crafting the tax bill. Although he would have preferred a cash sale of the Muzinich & Co. stock, Wyden said in a statement that in July 2018 Muzinich had agreed to “strengthen his recusal commitments to include matters where his family’s company is a party.”

That satisfied Wyden at the time, but it is a very narrow restriction. A vast range of issues before the Treasury could affect Muzinich & Co. regardless of whether the firm was directly a party to any of them.

How Justin Muzinich treated the transaction for tax purposes could reveal whether it was a true and final sale or not.

Ordinarily, a sale of an asset such as equity in a company would trigger a capital gains tax bill. In Muzinich’s case, that could run into the tens of millions of dollars, even though his father paid him no cash upfront. But there is an exception if the asset in question is merely transferred with a commitment to have it returned, said Steve Rosenthal, a tax law expert at the Urban-Brookings Tax Policy Center.

“If you are merely parking or pledging securities, and you are going to get them back, that’s not viewed as a taxable transaction,” he said.

It is not clear how he reported the transaction to the IRS, and whether he was left with a huge tax bill. The Treasury declined to comment on the tax issues.

Tax Reform — for Friends and Family

Through his first year in the administration, even as Muzinich continued to own his stake in the family firm, he met with a wide range of business executives to hash out major tax provisions that would affect them, according to his 2017 calendars that ProPublica obtained after suing the Treasury last year under the Freedom of Information Act. Others were obtained by the watchdog group American Oversight. The Treasury redacted large sections of the calendars, saying that they required consultation with the White House before they could be released.

One of the most important principles in the federal government ethics rules covers whether an official is dealing with a “particular matter” that would affect a discrete group of people with specific interests or a “general matter” that affects a larger and more diverse group.

The Treasury spokeswoman said the tax reform bill was to affect a very large and diverse group, so ethics rules did not prevent Muzinich from working on it. He was allowed to keep his equity in the company while working on the tax bill because his “duties did not include particular matters that required divestiture of certain assets.”

But many industries had specific interests in the tax bill that they lobbied on — industries that may include clients of Muzinich & Co. Insurance companies, for example, featured prominently. Muzinich met with trade groups representing insurers as well as Liberty Mutual, The Hartford, Zurich and Blue Cross Blue Shield. In the final tax bill, property and casualty insurers fared particularly well by dodging new limitations on deductions that applied to other companies.

Insurance companies invest their premiums in order to increase their profits. In its regulatory filings, Muzinich & Co. reports that 17 of its 89 clients are insurance companies, which have given the firm more than $1.4 billion to invest. Muzinich & Co. did not provide a list of its clients.

Some of the companies Muzinich & Co. has stakes in also have been lobbying the Treasury on their own behalf. For example, Muzinich & Co. helps its clients invest in business development companies, a type of investment fund that enjoys lower taxes in exchange for providing capital to medium-sized companies. The firm itself owns stock in BDCs, many of them run by private equity companies such as Ares Capital Corporation, which has paid millions of dollars to lobby for looser rules governing the BDC industry.

Even beyond any overlap with the family firm’s interests, Muzinich’s calendars, which cover the period from February to September of 2017, reflect the administration’s priorities in negotiating the tax deal. Muzinich spent long days in meetings with private equity titans, energy company CEOs and heavy-hitting interest groups like the Business Roundtable and the anti-tax group Americans for Prosperity. His calendar shows no meetings with labor unions or progressive groups.

Muzinich did meet often with the Treasury’s in-house tax experts but frequently didn’t follow their recommendations. Richard Prisinzano, who served in the agency’s tax analysis office until August 2017, recalled trying to tell Mnuchin and Muzinich that drastically lowering corporate tax rates would likely prompt businesses to transform into C corporations, which often pay lower rates under the new law.

He argued that such a change would further reduce tax revenues. Muzinich disagreed, Prisinzano said, protesting that businesses wouldn’t change their corporate form just to lower their taxes. “He really pushed back,” Prisinzano recalled. “He said to me, ‘The secretary is a numbers person, and the numbers don’t make sense to him.’”

“‘I’m a numbers person, and they make perfect sense to me,’” Prisinzano said he responded. “That was not an answer that they liked.”

In the following two years, many large businesses did indeed convert into C corporations, including private equity giants Ares, Blackstone and KKR. The government hasn’t produced an estimate of how big a hit taxpayers took from these conversions.

During his confirmation hearing as deputy secretary in July 2018, Democratic senators pressed Muzinich on whether he agreed with the White House that the tax bill would “pay for itself,” despite the dire projections of independent forecasters such as the nonpartisan Congressional Budget Office. “Yes,” Muzinich responded.

It has not come close, as corporate tax collections plunged and left the national debt at historic levels on the eve of the pandemic.

Muzinich Takes on the COVID-19 Crisis

As the economic response to the novel coronavirus consumed Washington in March, Mnuchin turned again to Muzinich to negotiate with Congress over the shape of a bailout intended to sustain companies as they weathered the worst part of the crisis.

Ultimately, Trump administration officials and lawmakers settled on a package worth more than $2 trillion, divided into aid regimens for different sectors of the economy. While setting general parameters, the Coronavirus Aid, Relief and Economic Security Act gives the Treasury wide latitude over how the money is to be distributed. It calls for $50 billion in grants and loans for the airline industry, for example, with few rules on who should get what. (In another potential intersection with Muzinich’s Treasury work, Muzinich & Co. started a new business line to loan money to airlines to buy planes in February.)

Perhaps the greatest power the Treasury now has is the authority to sign off on Fed loan programs funded with CARES Act money. The Fed has said it will leverage that money to lend up to several trillion dollars.

Among their biggest decisions: Which firms to include in the $600 billion Main Street Lending Program, which will lend directly to mid-sized businesses, and how to structure two programs that will purchase up to $750 billion in corporate bonds.

The Main Street program, which has yet to launch, changed substantially after it was first announced to sweep in bigger companies and those with heavier debt loads. Offering a glimpse into how the Treasury directly shaped the Fed programs, Energy Secretary Dan Brouillette told Bloomberg the change was made in part to make sure beleaguered oil companies had access to the program’s favorable terms. Muzinich & Co.’s U.S.-based funds include dozens of energy companies.

Mnuchin also deputized Muzinich to fix problems that arose during the first round of funding for the Paycheck Protection Program, which offers forgivable loans to small businesses. The government hasn’t said who got money through the program, but Muzinich & Co.’s portfolio includes many companies that are small enough to be eligible.

The Fed’s bond purchasing programs will go even further to help companies with poorly rated credit.

On March 23, the Fed and the Treasury announced a sweeping stimulus program that would involve buying hundreds of billions of dollars of investment-grade bonds. Selling bonds is a way for large companies like Boeing or PepsiCo to raise money for new investments, to fund day-to-day operations or to pay back older loans. Companies that are strong and profitable are expected to be able to pay back the borrowed money. Their bonds are deemed “investment grade” and come with lower interest rates. The news of the Fed program on its own heralded a dramatic recovery in the bond market, which in three weeks recovered nearly all of the 13.6% it had lost since the plunge began on March 6, according to one index.

Then, on April 9, the Fed announced, with the Treasury’s approval, that it would expand its efforts to buy some junk bonds. These carry higher interest rates because the borrowing companies are viewed as riskier and may already be heavily in debt. One index tracking that market segment surged nearly 8% on the news, the most in a decade. This risker category of bonds has expanded dramatically in recent years as companies took on higher debt burdens to do things like acquire competitors and buy back stock. These are the bonds in which Muzinich & Co. has long specialized.

At the end of 2019, Muzinich & Co. reported it had $2.8 billion of assets under management in its U.S. high-yield bond strategy. A Muzinich fund that focuses specifically on those bonds took significant losses in March, as companies like oilfield services provider Targa Resources and Caesars Entertainment saw the price of their bonds fall 30% and 35% respectively.

The government’s announcement buoyed Muzinich & Co.’s high-yield holdings along with everyone else’s. The portfolio manager for the firm’s U.S. high-yield offering also praised CARES Act’s tax provisions that would “help high yield companies.”

In a separate development in May, the Fed expanded another Treasury-backed lending program in a way that could help Muzinich & Co.’s portfolio. The central bank said May 12 it would support “syndicated loans,” another form of corporate debt often in which riskier firms borrow money from multiple lenders. Muzinich & Co. had more than $3 billion in assets under management in U.S. and European syndicated loans at the end of last year.

The good news for Muzinich & Co. keeps coming. As the firm’s head of investment strategy, Erick Muller, told investors in a May 13 webcast about the junk bond market: “The recovery is pretty spectacular.”

Doris Burke and Hannah Fresques contributed reporting.

Press freedom is under attack

As Trump cracks down on political speech, independent media is increasingly necessary.

Truthout produces reporting you won’t see in the mainstream: journalism from the frontlines of global conflict, interviews with grassroots movement leaders, high-quality legal analysis and more.

Our work is possible thanks to reader support. Help Truthout catalyze change and social justice — make a tax-deductible monthly or one-time donation today.