Support justice-driven, accurate and transparent news — make a quick donation to Truthout today!

![]()

In 2008, when George Glover decided to retire from his job as a program coordinator for the Rhode Island Department of Labor and Training after 33 years, he did so with the expectation of receiving a 3 percent cost-of-living increase in his state pension every year. A statistician by training, Glover had planned methodically for his retirement, making spreadsheets, doing the math. Between Social Security, his state pension, and the adjustments for the cost of living, he figured he would be able to pay all his bills and have a little left over.

“I’m what you might call meticulous,” he said. “I never make a decision without running the numbers first.”

Then, in 2011, the Rhode Island legislature, claiming that the state’s retirement system had become unsustainable, passed a sweeping law — euphemistically dubbed the Rhode Island Retirement Security Act — that made drastic modifications to the pension scheme.

Among other changes, the legislation raised the minimum retirement age, changed from a defined benefit plan to a mixture of a defined benefit plan and a defined contribution plan, and switched from giving retirees a 3 percent annual cost-of-living adjustment (COLA) to giving them one every five years at a rate that will depend on the fund’s investment returns. The revised system will remain in effect until the pension fund reaches an 80 percent funding ratio (as of 2011, the funding ratio of the Rhode Island State Employee Retirement System was only 57.4 percent).

For Glover, that means that he will not be receiving the COLA that he was counting on this January, and that he has no way of knowing how much the next one will be. If the subsequent COLAs are lower than the increase in the overall cost of living, his pension will be worth less and less every year. Though he still expects to be able to pay all of his monthly bills next year, Glover said that he will not be able to save any money for the bills that come due annually, such as his car insurance and his taxes. To make up for the difference, he said, he is considering finding a part-time job.

“I had my plan in place,” he said. “I did everything that I was told to do and made my plans based on everything I had been told. Then the state changed its mind and decided to pull out. I just don’t think that’s fair.”

After the legislation passed, Glover, along with hundreds of other retired state workers and current employees, filed lawsuits alleging that the bill was a violation of their contracts with the state. The Rhode Island constitution, like the federal Constitution, prohibits the state from passing any law “impairing obligation of contracts.”

The argument put forward by the Rhode Island officials who are named in the lawsuit — including Governor Lincoln D. Chafee and State Treasurer Gina Raimundo — is that the promises the state has made to its workers about their pensions do not constitute contracts, and are thus not legally enforceable.

The stakes in the case are very high. According to legal experts, if the courts uphold the state’s argument, it would represent a drastic and fundamental shift in the way that state pensions have been treated under the law for decades, with implications that could be large and lasting, not just in Rhode Island, but across the country.

“The entire public pension system is built on the understanding that pensions are legally protected promises,” said Richard Kaplan, a professor at the University of Illinois College of Law. “That idea has been foundational for at least the last half-century.”

That was certainly the understanding that Glover had when he took his job with the state in 1975, so he was surprised when he heard that the state was arguing that employees and retirees had no contractual rights to their pensions.

“The state made a promise to me,” he said, “and now it’s reneging on that promise. That isn’t how it’s supposed to work. When I grew up, a promise was a promise was a promise.”

Promises or “gratuities”?

Paul Secunda, an associate professor at Marquette University Law School, explained that until the early 20th century, courts had treated public pensions not as contracts or promises but as “gratuities,” more akin to gifts or tips than to salaries or wages.

“It was accepted that employees didn’t have any rights to their pensions and that the employers could change them at any time, almost on a whim,” he said. “People could work their whole lives and then, just before they were going to retire, the employer could pull the rug out from under them.”

Since the middle of the century, however, courts have generally acknowledged that states cannot promise pension benefits to their employees as an inducement to get them to work for the state and then renege on those promises. The large majority of states have protected pensions under the theory that the promise of a pension represents a form of contract, though there is some variation (see bottom box entitled “A variety of legal protections”).

“We moved from a place where pensions were thought of as being like tips to a place where it was understood that they were part of the compensation that employees had earned,” Stein said. “The legal understanding has been, ‘That is your money, and the state can’t take it away.’”

“A radical shift”

According to Secunda, the lawsuits that are moving through the courts in Rhode Island and other states gain added significance when seen within the context of the historical evolution away from a gratuity model.

“We’re at an inflection point,” Secunda said. “We’re poised between these two possibilities: will the court uphold the contract model and find that public pensions are entitled to legal protections, or will they move back toward the gratuity model, where the legislature can change benefits on a whim?”

The majority of pension lawsuits are still pending in state courts, but the decisions that have come down have gone both ways. In April, for example, a South Dakota judge ruled that cost-of-living adjustments the state had promised to retirees were not contractually protected, while in October, the Colorado Court of Appeals ruled that they were.

Michael Yelnosky, a professor of law at Roger Williams University in Bristol, Rhode Island, said that, “[i]n other rulings, courts have just chipped away at the contractual protection, and have generally upheld some limits on what the state can do,” he said. “But here the state is saying, ‘Just throw the contract stuff out the window and give us free reign.’”

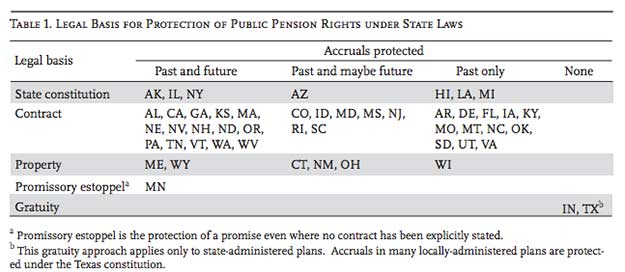

A variety of legal protections

Though every state except for Texas and Indiana extends some form legal protection to the pension rights of their employees, the legal basis for these protections varies from state to state.

The vast majority of states — 41 — apply a contract theory to their employees’ pension rights. All of these states have consitution provisions that — mirroring the contract clause of the federal Constitution — prohibit the passage of any law that impairs the obligation of contracts. In the constitutions of seven of these states, there is a clause explicitly preventing the state from reducing the pension benefits its employees have earned. In the remaining 34, statutes and judicial decisions have found that the promise made by the state to pay a specified amount to the employee in pension benefits constitutes a contract and is entitled to constitutional protection.

Six states have adopted a property-based model of protecting pensions, meaning that the promised benefits are legally considered to be the property of the employee who has earned them. Thus, according to the Fifth and Fourteenth amendments of the federal Constitution, promised benefits cannot be “taken for public use, without just compensation.”

The Second Judicial District Court of Minnesota recently applied a third model of legal protection to the state’s pension obligations. Under this model, known as “promissory estoppel,” the state must live up to the promises it has made — even if those promises did not form contracts — if the promises have been reasonably relied upon by another party and if breaking the promises would cause an injustice.

Finally, Texas and Indiana apply a “gratuity” model to state pension promises. Under this theory, benefits are considered more akin to gifts or tips than to salary or wages, and can be unilaterally modifed by the state at any time.

Additionally, there is variation from state to state as to the point at which these legal pension protections for state workers apply. Pension benefits are earned, or “accrued,” over time. In 21 states, the protections apply both to the benefits that have accrued and to future promised benefits. In 16 states, the protections apply to accrued benefits only. In 11 states, it is unclear whether the protections apply to past and future benefits or only to past benefits.

Source for table: Center for Retirement Research at Boston College

Though a decision in Rhode Island would not be binding on other state courts, Richard Kaplan of the University of Illinois explained that state judges tend to look at how other states have decided similar cases when making their own rulings. If other courts were to follow Rhode Island’s example, it would represent “a radical shift” in the legal landscape governing public pensions.

“It cuts against decades of precedent,” Kaplan said, “not to mention basic, commonsense notions of what pensions are and what’s fair.”

According to Secunda of Marquette University, a shift back towards a gratuity model would be “disastrous.”

“What the states are trying to do is change the rules in the middle of the game,” he said. “They’re saying, ‘We’ll play by a certain set of rules until the game is not in our favor anymore, and then we’ll change them.’ Try explaining that to a five-year-old and see if they think it should be allowed.”

Kaplan agreed. “What the states told these workers was that ‘if you do x, you’ll get y.’ You can be sure that the states didn’t say, ‘if you do x, and we feel like we can afford it, you’ll get y.’”

Joseph Slater, a professor of law at the University of Toledo and a labor historian, explained that, historically, states and local governments have used the promise of secure pensions to justify paying public employees less than they might earn in the private sector.

“If they knew that that promise didn’t really mean anything, people might have made different decisions about what job to do,” he said. “This is part of the reason why they decided to dedicate their lives to public service.”

So far, the Superior Court Associate Justice Sarah Taft-Carter, who is assigned to the Rhode Island pension cases, has seemed to agree with those arguments. In a 2011 ruling on another lawsuit concerning previous, less drastic changes that the state legislature had made to the pension system, she ruled that pensions do constitute “implicit contracts.”

In that decision, Justice Taft-Carter explicitly rejected the gratuity model. “The benefits provided…[to retirees] are not gratuities that may be taken away at the whim of the State,” she wrote, adding that reliance on “[m]edieval notions of the beneficence and graciousness of worldly monarchs have no relevance to modern notions of sovereignty.”

A negotiated settlement?

In Rhode Island, several public employee unions have offered to negotiate with the state, and Gov. Chafee has expressed interest in doing so.

State Treasurer Gina Raimundo, however, has so far refused to meet with the union leaders. Raimundo, the architect of the pension changes now in dispute, however, is apparently still looking for total victory.

“We have a strong case,” she told the Associated Press “I trust the courts. Let’s let it weave its way through.”

“What’s legal isn’t necessarily fair”

John Tarantino is a attorney representing the Governor, the Treasurer, and the Employees’ Retirement System of Rhode Island in the lawsuits. In a recent interview with Remapping Debate, Tarantino explained that the state’s argument in the current lawsuits hinges on convincing Justice Taft-Carter (or the State Supreme Court, if the state loses this case and appeals it) that the legislation that set benefit levels in the past was no different than any other law, meaning that the legislature can change those benefits at any time. According to that theory, the state lawmakers can legislatively modify the benefits that public employees have been promised as easily as they might change the speed limit.

“We believe that the decisions of one legislature should not be binding on the decisions of a future legislature,” he said.

When asked whether he believed it was reasonable for the workers, when they were hired, to expect and rely on the benefits that were outlined to them, however, Tarantino said, “Absolutely.”

And doesn’t that promise make the law different from other legislation that can be changed at any time?

“Listen, I take promises very seriously,” Tarantino said. “I’m a man of my word. But just because I make a promise to you, that doesn’t mean that we have a contract.”

But wouldn’t breaking that promise violate basic notions of equity and fairness?

“That stuff doesn’t matter,” Tarantino responded. “All I’m going to try to prove is that it’s legal. What’s legal isn’t necessarily fair.”

Another potential escape route for states?

When pension benefits and other promises are deemed to enjoy contractual protections, that does not mean that the state cannot break those promises under any circumstances. It is generally agreed that the terms of a contract may be changed if breaking the promise is found to be “reasonable and necessary” to achieve an “important public purpose.”

According to Richard Kaplan, a professor of law at the University of Illinois, proving that reneging on their pension obligations is necessary to achieve an important public purpose is a high bar to reach, because that argument implies that the state’s ability to raise taxes to keep its promises have been exhausted.

“That argument might make sense if the state is really in extremis, if we’re talking about going without teachers and firefighters,” Kaplan said. “But even in that case, the state would have to convince the court that raising taxes was somehow off the table.”

In Rhode Island, however, the state is currently making what several legal observers characterized as a far more extreme argument: that it is not under any contractual obligation to keep its promises to its employees about their pension at all.

“Rhode Island isn’t arguing that it had no choice but to make these cuts or else public welfare would be jeopardized,” said Stephen Pincus, an attorney with a Pittsburgh law firm who has represented state employees in pension lawsuits in other states. “The state is saying that employees have no contract rights to their pensions at all.”

“In that argument,” Pincus continued, “the circumstances aren’t important. The state is saying that they can change the terms of the agreement at any time,” regardless of whether doing so is reasonable and necessary for an important public purpose.

Do states really have no choice?

According to several legal experts, the argument that pensions enjoy no contractual protections can best be seen as a tactical decision on the part of the states to try to get around what they originally intended when they promised certain pension benefits to their employees.

“Nobody’s had any great philosophical revelation about contract theory,” said Kaplan said. “The state is just trying to find any argument that allows them to get out of their obligations and that will stick in court.

Stein agreed, and added that the context for the Rhode Island lawsuits and several others around the country was that past lawmakers persistently failed to make their necessary contributions to the pension system.

“Now, the bills are coming due, and they’re looking for a legal framework that allows them to go back on their promises,” he said. “They know that they need to get the court’s blessing on these huge, dramatic changes in pension rights.”

The alternative, Stein said, would be to “go to the citizens of the state as a whole and say, ‘We made these promises but we messed up and didn’t put enough money away, so we need to ask each of you to pay a little more in taxes so that we don’t break them.’”

“The reason we’re seeing these reforms in the first place is that officials haven’t had the courage to do that,” he added.

If the Rhode Island lawsuits are successful, Secunda said, it could make it easier for other courts to reduce protections, and even open the door to future pension cuts.

If Rhode Island is given legal authority to “renege on promises made to workers,” you “can be sure that other states are going to try to go down the same path,” Secunda said. “Right now, we’re waiting for the other shoe to drop.”

In the meantime, George Glover, the retired Rhode Island state worker, said that he was fully conscious of the implications of the lawsuits. “Our whole system of economics in America is based on trust and contracts,” he said. “I just think that to allow the state to get out of its promises like this runs against that entire idea.”

An Intimidation tactic?

States may also be able to use the threat of going back on their promises to extract preemptive concessions from public employee unions.

In Illinois, for example, Governor Pat Quinn and state lawmakers have proposed several versions of pension legislation, the latest of which would, among other changes, reduce cost-of-living adjustments, raise the retirement age, and increase employee contributions. The legislation surprised many observers because Illinois has long had some of the strongest pension protections in the country, including a specific clause saying that pension benefits “shall not be diminished or impaired.”

Though they have vowed to fight the legislation in court, a coalition of public employee unions in Illinois has also offered to negotiate for pension changes with the state.

An important fundraising appeal: 6 Days to raise $42,000

Truthout is one of only a few platforms for justice-oriented, grassroots journalism. Today, as political censorship from the right intensifies, we have no choice but to ask for your help.

We are fundraising right now to cover our basic operating expenses. If you can support Truthout with a one-time or monthly donation, you will make a significant impact on our work. Anything you can do makes a difference — we appreciate your support.