Honest, paywall-free news is rare. Please support our boldly independent journalism with a donation of any size.

Antonio Fatas, a professor at the Insead business school, in commenting on recent research on deleveraging (or the lack thereof) on his blog, emphasized one of my favorite points: No, debt does not mean that we’re stealing from future generations.

Globally – and for the most part even within countries – a rise in public debt isn’t an indication that we’re living beyond our means, because as Mr. Fatas put it, one person’s debt is another person’s asset. Or, as I have put it before, debt is money we owe to ourselves – an obviously true statement that, I have discovered, has the power to induce blinding rage in many people.

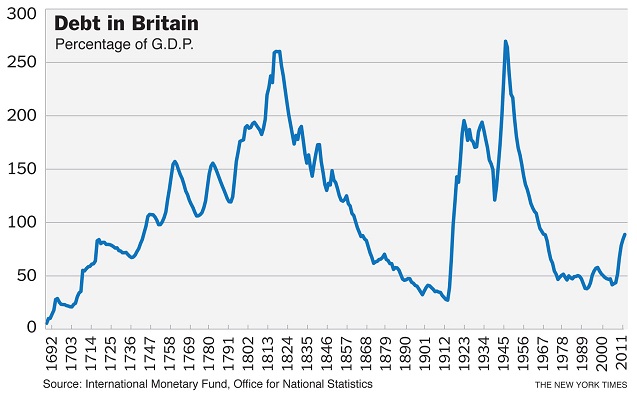

Think about the history shown in the chart here. Britain did not emerge impoverished from the Napoleonic Wars in the early 1800s. The government ended up with a lot of debt, but the counterpart of this debt was that the British propertied classes owned a lot of consols, or government bonds.

More than that, as Mr. Fatas pointed out on his blog, rising debt can be a good sign. Think of my little two-classes model of debt, where some people are less patient than others – perhaps (to step outside the model a bit) because they have better investment opportunities.

Moving from a very limited financial system that doesn’t allow much debt to a somewhat more open-minded system should, in that case, be good for growth and welfare.

The problem with private debt is that we have good reason to believe that, in very wide open financial systems, people get irrationally exuberant, lending and borrowing to an extent that they eventually realize is excessive – and that there are huge negative externalities when everyone tries to deleverage at the same time. This is a very big concern, but it’s not about generalized excess consumption.

And the problems with public debt are also mainly about possible instability, not that we’re “borrowing from our children.” The rhetoric of fiscal debates has been, for the most part, nonsense.

An important fundraising appeal: 6 Days to raise $41,000

Truthout is one of only a few platforms for justice-oriented, grassroots journalism. Today, as political censorship from the right intensifies, we have no choice but to ask for your help.

We are fundraising right now to cover our basic operating expenses. If you can support Truthout with a one-time or monthly donation, you will make a significant impact on our work. Anything you can do makes a difference — we appreciate your support.