Honest, paywall-free news is rare. Please support our boldly independent journalism with a donation of any size.

I promised recently that I would share some nagging concerns about a paper on redistribution and growth by Jonathan D. Ostry, Andrew Berg and Charalambos G. Tsangarides, researchers at the International Monetary Fund. They conclude that there is no negative effect of redistributionist policies, at least within the range we normally see, and quite possibly a positive effect from the reduction in inequality.

I think I can usefully phrase my concerns in terms of my favorite comparison on these matters, which is between the United States and France.

Why this pair? Because we’re talking about two advanced countries that clearly have similar levels of technological competence but have made very different social policy choices. In particular, France not only does much more redistribution, but has expanded its redistribution over time, limiting the rise in overall inequality, while the United States has not.

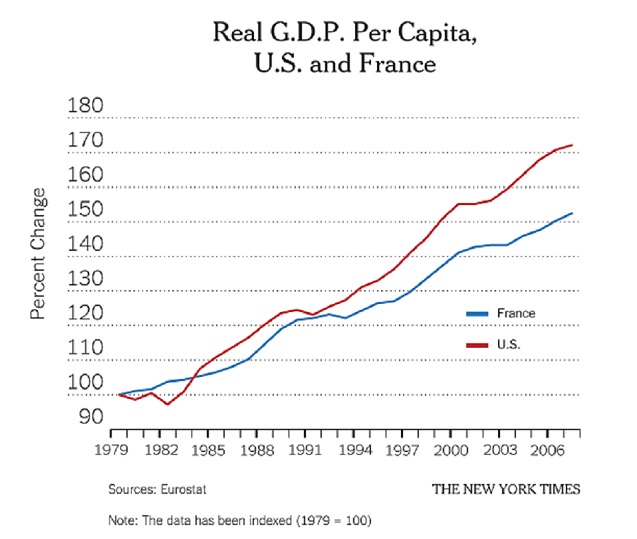

So how have the countries’ destinies compared during the New Gilded Age? Growth actually has been somewhat slower in France, although it’s hardly the catastrophe that the incessant bad press about the country might lead you to expect (see the chart on real gross domestic product per capita on this page.)

Even more strikingly, however, the level, as opposed to the growth rate, of French G.D.P. per capita is substantially lower than that of the United States.

This is my main concern about Ostry et al. Suppose a person thinks that strong redistributionist policies reduce the level of output – but that it’s a one-time shift, not a permanent depression of growth. Then he could accept their result of a lack of impact on growth while still believing in serious output effects.

Now, the I.M.F. researchers arguably have answered this objection by also including the current level of G.D.P. per capita in their regressions, which indicate that a country with lower G.D.P. per capita than the United States should be growing faster than the United States, other things being equal. So any level-depressing effect of redistribution should show up as a failure of this faster growth to materialize. But I’m uneasy about whether this is good enough.

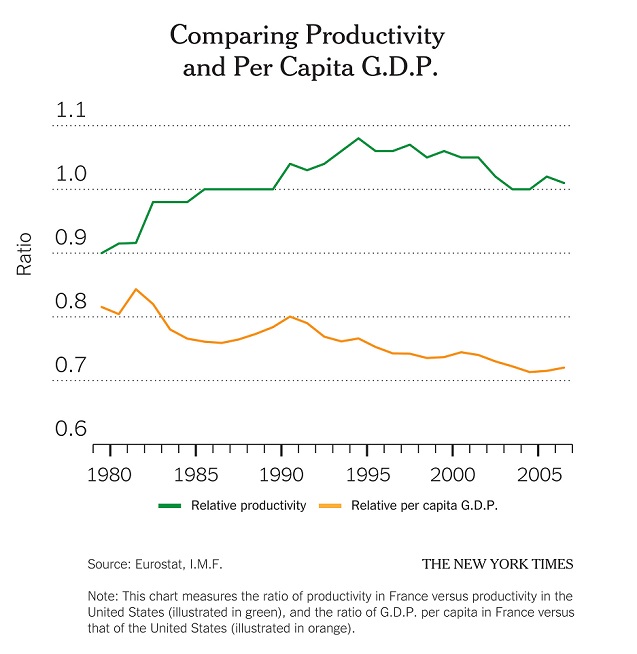

Interestingly, French underperformance is a matter of low labor input rather than low productivity (see the second chart).

Once you delve into this low labor input, it starts to look like the result of some very specific policies rather than redistribution in general: a pension system that encourages early retirement, regulations that give French people shorter hours and much more vacation time than we get.

Overall, I am still mostly persuaded by the I.M.F. paper, but I think we need to acknowledge that it’s not quite as slam-dunky as liberals might like.

Important Message: Please Read

For 25 years, Truthout has survived by publishing impactful investigative journalism and analysis; distributing full editions 365 days a year; and building a community of readers who support us with small, hard-earned donations.

Eighty percent of our $3 million yearly budget comes from small donors alone. Of those, 8,000 readers support us with monthly donations. Back in 2018, when Facebook decided to suppress the circulation of posts made by organizations, thereby cutting readers off from seeing many articles shared by the news organizations they had intentionally decided to follow, Truthout’s total traffic declined by 40 percent, as nearly all of our traffic from that platform disappeared.

As Google plans to roll out its new AI search bar, providing shoddy AI summaries instead of directing readers to our site, the consequences promise to be even more explosive. Google Search is our single largest source of traffic; it’s the route by which 27 percent of our readers find us. If even half of that 27 percent disappears, it will have a devastating impact on our journalism.

The entire journalism ecosystem will shoulder this blow, particularly independent publishers and news sites that depend on traffic and aren’t bankrolled by large corporations. If you can support Truthout with a donation today, you can help us resist the inevitability of Big Tech’s AI takeover. Please give today.