Honest, paywall-free news is rare. Please support our boldly independent journalism with a donation of any size.

It has become increasingly common to suggest that on top of the European debacle and the sluggish recovery in the United States, China might be on the verge of a collapse, and with it the last bastion of economic growth in the world economy would also be gone. Not only the center is stagnant, but also the periphery of the global economy is very fragile. But the probability of a Chinese slowdown is greatly exaggerated.

Paul Krugman, who has been correct about the need for fiscal expansion in the United States, and about the European Central Bank (ECB) mismanagement of the Greek crisis, for example, has suggested that China is in the middle of a housing bubble that can burst at any time (see also Jayati Ghosh and C. P. Chandrasekhar here for a similar, but broader view of the dangers in 2012). This view insinuates that growth in China is fundamentally dependent on domestic demand, but that the sources of the expansion are fragile. It, further, suggests that China now looks very similar to the US before the Lehman Brothers crisis in September 2008.

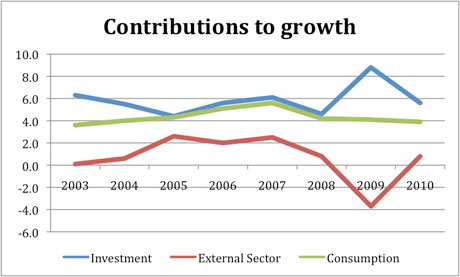

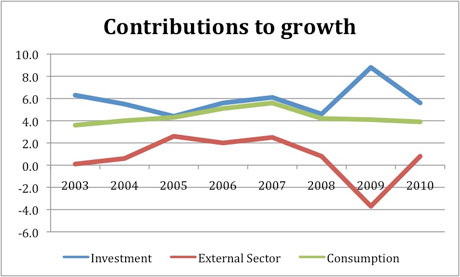

It would be good to check the data, before providing a full reply to the doomsday scenario. First when we look at the decomposition of the sources of growth in China, it becomes clear that since the beginning of the last boom in the periphery the external sector has not been the driving force in China, since imports, particularly of commodities, have grown very fast. Investment and consumption are, on the contrary, the main sources of Chinese growth. So on that one the pessimists’ are correct; growth in China is driven by domestic markets forces (by the way, that makes the complaint that China is not making enough to solve the so-called global imbalances a bit peculiar, to say the least).

Note also, in the graph above, that with the collapse of external demand during the 2007-09 crisis, investment, which corresponds to about 40% of GDP (in the US for comparison is closer to 15%), of which about half is public and good chunk goes to housing, increased to make up the difference.

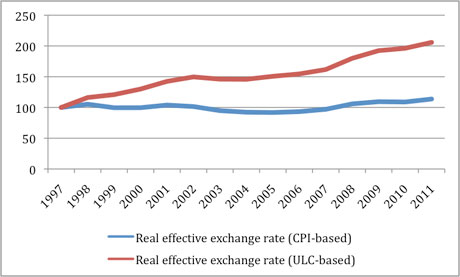

It is worth noticing that the rise of China as a great trade power, which brought about better economic opportunities for peripheral countries in Africa and Latin America, since its entry in the World Trade Organization (WTO) in December of 2001, has taken place hand in hand with a significant real appreciation of its currency. While the real exchange rate deflated by the Consumer Price Index barely moves (and fits the complaints that China has not done enough to appreciate its currency and solve the global imbalances), the one deflated by Unit Labor Costs (ULC) has appreciated about 100% since the Asian Crisis of 1997.

Further, as the 3rd graph (below) shows it seems that ULC changes have fundamentally followed the variations of real wages. In other words, the expansion of real wages, which has been one of the pillars of consumption growth, a central component of output growth as we saw in the first graph, has undermined the external competitiveness of China, as it should be expected.

Public investment and domestic consumption, the driving forces of the expansion, are built on a foundation of insignificant foreign borrowing (foreign obligations as a share of reserves are tiny, since international reserves stand at around US$ 3 trillion) and a sustained increase in workers remuneration (for a chart of real wage growth going back to the 1980s go here). In that sense, a fundamental difference of the Chinese boom with respect to other bubble based booms, is that the housing boom was not central to allow the expansion of consumption and there is no imaginable balance of payments problem ahead.

Further, China is going through a long transition from a rural society to an urban industrial one, which would imply that hundreds of millions of people moving to cities in the next couple of decades. Given the size and importance of public investment for the Chinese economy it would surprising if there is no public involvement in the expansion of public housing projects to say the least.

But lets assume that the pessimists are correct and that housing prices collapse in China. Critics suggest that local governments, which are heavily dependent on land sales, and banks, that issued record numbers of home mortgages, will be the first to be hurt by a collapse of the housing market. The government will be forced to rescue banks, and, again like in the US, this would take precedence over growth and employment creation. Yet, I find this scenario very unlikely.

Note that in China and the US the debt is all denominated in domestic currency and, as a result, it is a political decision to rescue banks and creditors, or promote growth and favor debtors. While the expansions in the US have been weak (not just this one, but for 30 years now; see here), and the economic policies have been pro-creditors (Wall Street if you prefer) and anti-labor, the long Chinese boom has not been so. Growth (and direct repression of dissent, one might note) has been the way to sort out social conflicts in China. Nothing indicates that would change in 2012.

Press freedom is under attack

As Trump cracks down on political speech, independent media is increasingly necessary.

Truthout produces reporting you won’t see in the mainstream: journalism from the frontlines of global conflict, interviews with grassroots movement leaders, high-quality legal analysis and more.

Our work is possible thanks to reader support. Help Truthout catalyze change and social justice — make a tax-deductible monthly or one-time donation today.