Did you know that Truthout is a nonprofit and independently funded by readers like you? If you value what we do, please support our work with a donation.

Debate continues to rage between the inflationists who say the money supply is increasing, dangerously devaluing the currency, and the deflationists who say we need more money in the economy to stimulate productivity. The debate is not just an academic one, since the Fed's monetary policy turns on it, and so does Congressional budget policy.

Inflation fears have been fueled ever since 2009, when the Fed began its policy of “quantitative easing” (effectively “money printing”). The inflationists point to commodity prices that have shot up. The deflationists, in turn, point to the housing market, which has collapsed and taken prices down with it. Prices of consumer products other than food and fuel are also down. Wages have remained stagnant, so higher food and gas prices mean people have less money to spend on consumer goods. The bubble in commodities, say the deflationists, has been triggered by the fear of inflation. Commodities are considered a safe haven, attracting a flood of “hot money” – investment money racing from one hot investment to another.

To resolve this debate, we need the actual money supply figures. Unfortunately, the Fed quit reporting M3, the largest measure of the money supply, in 2006.

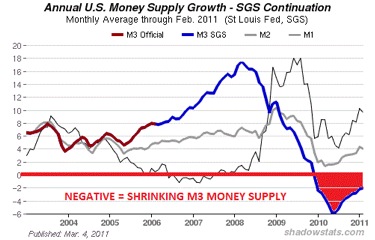

Fortunately, figures are still available for the individual components of M3. Here is a graph that is worth a thousand words. It comes from ShadowStats.com (home of Shadow Government Statistics, or SGS) and is reconstructed from the available data on those components. The red line is the M3 money supply reported by the Fed until 2006. The blue line is M3 after 2006.

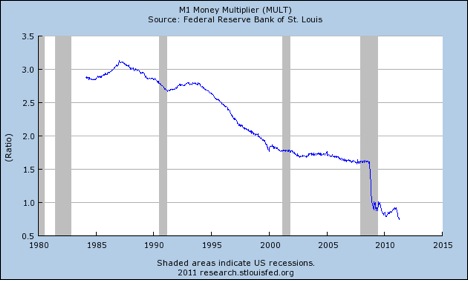

The chart shows that the overall US money supply is shrinking, despite the Fed's determination to inflate it with quantitative easing. Like Japan, which has been doing quantitative easing (QE) for a decade, the US is still fighting deflation. Here is another telling chart – the M1 Money Multiplier from the Federal Reserve Bank of St. Louis:

Barry Ritholtz comments, “All that heavy breathing about the flood of liquidity that was going to pour into the system. Hyper-inflation! Except not so much, apparently.” Ritholtz quotes David Rosenberg: “Fully 100% of both QEs by the Fed merely was new money printing that ended up sitting idly on commercial bank balance sheets. Money velocity and money multiplier are stagnant at best.” If QE1 and QE2 are sitting in bank reserve accounts, they're not driving up the price of gold, silver, oil, and food, and they're not being multiplied into loans, which are still contracting.

The part of M3 that collapsed in 2008 was the “shadow banking system,” including money market funds and repos. This is the non-bank system in which large institutional investors that have substantially more to deposit than $250,000 – the Federal Deposit Insurance Corporation (FDIC) insurance limit – park their money overnight. Economist Gary Gorton explains:

[T]he financial crisis … [was] due to a banking panic in which institutional investors and firms refused to renew sale and repurchase agreements (repo) – short-term, collateralized, agreements that the Fed rightly used to count as money. Collateral for repo was, to a large extent, securitized bonds. Firms were forced to sell assets as a result of the banking panic, reducing bond prices and creating losses. There is nothing mysterious or irrational about the panic. There were genuine fears about the locations of subprime risk concentrations among counterparties. This banking system (the “shadow” or “parallel” banking system) – repo based on securitization – is a genuine banking system, as large as the traditional, regulated banking system. It is of critical importance to the economy because it is the funding basis for the traditional banking system. Without it, traditional banks will not lend, and credit, which is essential for job creation, will not be created.[Emphasis added.]

Before the banking crisis, the shadow banking system composed about half the money supply, and it still hasn't been restored. Without the shadow banking system to fund bank loans, banks will not lend, and without credit, there is insufficient money to fund businesses, buy products, or pay salaries or taxes. Neither raising taxes nor slashing services will fix the problem. It needs to be addressed at its source, which means getting more credit (or debt) flowing in the local economy. When private debt falls off, public debt must increase to fill the void. Public debt is not the same as household debt, which debtors must pay off or face bankruptcy. The US federal debt has not been paid off since 1835. Indeed, it has grown continuously since then, and the economy has grown and flourished along with it.

As explained in an earlier article, the public debt is the people's money. The government pays for goods and services by writing a check on the national bank account. Whether this payment is called a “bond” or a “dollar,” it is simply a debit against the credit of the nation. As Thomas Edison said in the 1920's:

If our nation can issue a dollar bond, it can issue a dollar bill. The element that makes the bond good, makes the bill good, also. The difference between the bond and the bill is the bond lets money brokers collect twice the amount of the bond and an additional 20%, whereas the currency pays nobody but those who contribute directly in some useful way…. It is absurd to say our country can issue $30 million in bonds and not $30 million in currency. Both are promises to pay, but one promise fattens the usurers and the other helps the people.

That is true, but Congress no longer seems to have the option of issuing dollars, a privilege it has delegated to the Federal Reserve. Congress can, however, issue debt, which, as Edison says, amounts to the same thing. A bond can be cashed in quickly at face value. A bond is money, just as a dollar is.

An accumulating public debt owed to the International Monetary Fund (IMF) or to foreign banks is to be avoided, but compounding interest charges can be eliminated by financing state and federal deficits through state- and federally owned banks. Since the government would own the bank, the debt would effectively be interest-free. More important, it would be free of the demands of private creditors, including austerity measures and privatization of public assets.

Far from inflation being the problem, the money supply has shrunk and we are in a deflationary bind. The money supply needs to be pumped back up to generate jobs and productivity and, in the system we have today, that is done by issuing bonds, or debt.

An important fundraising appeal: 5 Days to raise $35,000

Thank you for reading Truthout today. We have a brief message before you go.

Unfortunately, donations are down for Truthout at a time when media faces immense pressure. Yet, grassroots media is vital in the fight against Trump’s authoritarian reign. Our mandate to tell the truth, share strategies for resistance, and speak against fascism grows more urgent each day. We must appeal for your support.

If you can support Truthout with a one-time or monthly donation, you will make a significant impact on our work. Please donate during our fundraiser.