Did you know that Truthout is a nonprofit and independently funded by readers like you? If you value what we do, please support our work with a donation.

Future historians will marvel at the austerity madness that gripped policy elites in the spring of 2010.

In a flurry of blind panic and irrational exuberance, organizations from the European Central Bank to the Organization for Economic Cooperation and Development suddenly abandoned everything we had learned, at a bitter cost, about economics during recessions and decided that fiscal austerity was the way to go while the world was in the depths of a slump — indeed, many claimed that spending cuts would actually be expansionary.

Not only was there an illogical push for austerity, but there also emerged a widespread demand for central banks to raise interest rates in the face of falling inflation and high unemployment.

This madness was exemplified by the O.E.C.D.’s economic outlook report in May, which supported these ideas. But the O.E.C.D. has suddenly changed its tune. “In the short term, the weakness can be dealt with [through] the prolongation of some of the monetary accommodation in some countries,” the O.E.C.D.’s secretary general, Angel Gurria, told Reuters on Sept. 17.

This is as close as such organizations ever get to admitting that they were wrong.

And speaking of the rewards of austerity, I think it’s worth checking to see whether there have been any.

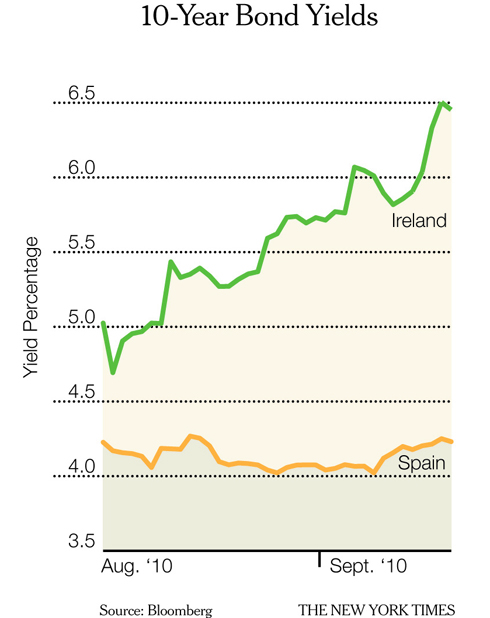

Regular readers may remember that I’ve written here about bond yields in Ireland and Spain.

Both had big housing bubbles and busts, but their post-bust politics have been very different, with Ireland quickly adopting austerity, and Spain much slower and grudging. And for a while many financial journalists asserted that the markets were rewarding Ireland’s virtuousness. But it was never true: Ireland’s economy didn’t perform better than malingering Spain’s.

And now, look at the bond data on this page— the market had a tough time this month after Barclay’s Capital released a dour economic outlook for Ireland, which had some commentators speculating about the country’s needing an I.M.F. bailout — speculation it has refuted.

In the last month, Ireland’s risk premium has exploded.

And Spain’s? Not so much.

Of course, Ireland’s banks were arguably second only to Iceland’s in their irresponsibility, and the Irish government’s blanket guarantee of bank liabilities has exposed it to huge losses.

But bear in mind that when Ireland seemed, briefly, to have regained the trust of the markets, this was touted as proof that austerity would be rewarded.

Do you like this? Click here to get Truthout stories sent to your inbox every day – free.

So the Irish are back to waiting for their reward for suffering.

What a strange trip it has been, though, sadly, it is not yet over.

——————————

Backstory: The Damages of Speculation

A gloomy report from Barclay’s Capital released in the middle of September sent Ireland’s bond market reeling, prompting the European Central Bank to pump millions of euros into the severely damaged market.

The report had sparked speculation that Ireland’s economic troubles might require a bailout from the International Monetary Fund, which spooked investors, who are already leery of Irish banks. Ten-year bond yields in Ireland quickly hit a record high on Sept. 17. This was indeed troubling news, since the yield increases as demand decreases and, thus, risk increases.

While the I.M.F. was quick to say that it did not expect Ireland to need a bailout, the damage had been done. Financial-services firms Barclays and Credit Suisse have said that the Irish government is doing all it can to address Ireland’s stalled economy — even if the government’s options are limited. And given recent economic forecasts for the global economy, these options are unlikely to improve anytime soon: Revising an earlier opinion, the Organization for Economic Cooperation and Development said in early September that world’s seven largest economies will likely grow by only 1.5 percent this year, not the 1.75 percent predicted earlier this year. With these economies underperforming, the peripheral European economies may suffer even more.

There has been one exception, however: Spain. The Spanish bond market has stabilized following a spate of bank reforms. On Sept. 16, Spain sold 4 billion euros’ worth of government bonds, and yields have dropped sharply since May — a clear signal that investor confidence there is strong.

Nevertheless, restoring market confidence remains a goal for the Irish. On Sept. 20, Ireland’s central bank governor, Patrick Honohan, indicated that Prime Minister Brian Cowen’s government needs to cut the coming budget more if Ireland wants to gain international confidence in its economy, according to the Financial Times.

Truthout has licensed this content. It may not be reproduced by any other source and is not covered by our Creative Commons license.

Paul Krugman joined The New York Times in 1999 as a columnist on the Op-Ed page and continues as a professor of economics and international affairs at Princeton University. He was awarded the Nobel in economic science in 2008.

Mr Krugman is the author or editor of 20 books and more than 200 papers in professional journals and edited volumes, including “The Return of Depression Economics” (2008) and “The Conscience of a Liberal” (2007).

Copyright 2010 The New York Times Company.

Fundraiser Deadline: Missed

Truthout is one of only a few platforms for justice-oriented, grassroots journalism. Today, as political censorship from the right intensifies, we have no choice but to ask for your help.

We missed our fundraising deadline, but there’s still time to help us meet our basic operating expenses before the end of the month. If you can support Truthout with a one-time or monthly donation, you will make a significant impact on our work. Anything you can do makes a difference — we appreciate your support.