Truthout is an indispensable resource for activists, movement leaders and workers everywhere. Please make this work possible with a quick donation.

Washington— After modest increases last year, the cost of job-based health insurance for families and individuals has jumped sharply this year, even though insurers are paying less in benefits as cash-strapped American workers opt for less medical care.

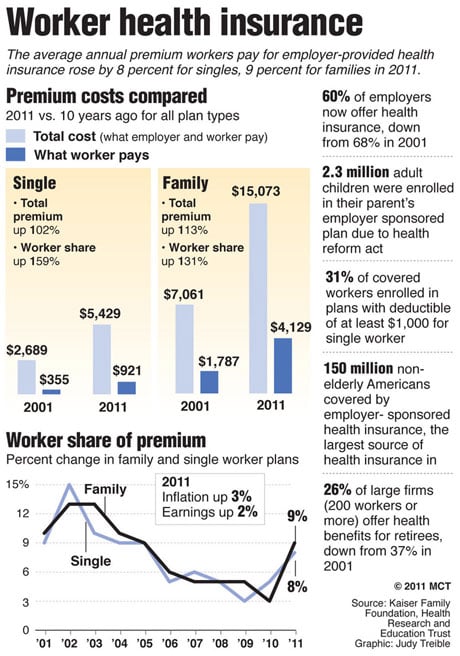

For the estimated 150 million workers with employer-sponsored coverage, the average cost of family health insurance jumped 9 percent this year to $15,073, while the price of individual coverage rose 8 percent to $5,429.

Both increases are the largest since 2005.

Click here to view larger.

Click here to view larger.Each far outpaced a national 2 percent hike in wages and a 3.2 percent rise in inflation, according to an annual survey of nearly 2,100 businesses that the Kaiser Family Foundation and the Health Research & Educational Trust released Tuesday.

Premiums for family and individual coverage had increased only 3 percent and 5 percent, respectively, in last year's survey.

“We don't know if this is a one-time jump and premiums will go back down again next year or whether we're entering a period of higher increases. We really don't know, and we won't know until next year,” said Drew Altman, the president and CEO of the Kaiser Family Foundation.

What is clear, however, is that family coverage premiums have climbed 113 percent since 2001, compared with a 34 percent rise in workers' wages and a 27 percent increase in inflation over the same period.

Employers still absorb the bulk of insurance costs. They pay an average of 72 percent, nearly $11,000, toward the cost of family coverage. Workers pay about 28 percent, an average of $4,129. For single coverage, workers pay about 18 percent, or $921, in premiums, while employers pay the rest, about $4,508.

The rising costs are why more employers and workers are opting for cheaper, high-deductible health plans that require patients to pay $1,000 or $2,000 in medical costs before their coverage kicks in. The survey found that 31 percent of covered workers are in high-deductible plans, up from 10 percent in 2006.

Karen Ignagni, the president of America's Health Insurance Plans, said the increasing cost of medical care was the main culprit behind the rate increases. Rising medical costs also helped pave the way for the landmark 2010 Affordable Care Act, which overhauled the nation's health care sygfstem.

But Altman said that this year's higher premiums, which were set last year, also might reflect insurers' expectation of a stronger economic recovery this year, with more patients presumably seeking more services.

Other insurers may have set rates higher this year thinking that the Affordable Care Act would increase their costs. But analysis by Kaiser and the federal government found that provisions in the new law enacted last year probably accounted for only 1 to 2 percentage points of this year's premium increases.

“In the end, both assumptions were wrong — but insurance companies still charged high premiums and earned impressive profits,” said a blog post Tuesday by Nancy-Ann DeParle, assistant to the president and the White House deputy chief of staff.

Indeed, profits continue to pour in for insurers, who are spending less for services as covered workers postpone doctor visits and other elective medical procedures during the economic downturn. That trend was reflected in a quarterly measurement of employer health care costs by the Bureau of Labor Statistics, which came in at its lowest level in more than 10 years for the first half of 2011, according to DeParle.

Barclays Capital also reported that 13 of the 14 top health insurers beat their projected earnings for the first quarter, with profits averaging more than 46 percent higher than expected.

Ignagni, however, cited a report by Standard & Poor's that found health care costs covered by commercial insurance increased nearly 8 percent in the year that ended in July 2011. A May report by the independent consulting firm Milliman Inc. also found that the cost of care for a family of four covered in a preferred provider organization had increased 7.3 percent over 2010.

Ignagni said the premium increases simply reflected these trends. “It's the cost that's driving the numbers,” she said.

In addition, Ignagni said, as more young, healthy workers have trouble finding employment and increasing numbers of these workers decline health coverage even when they do find jobs, the risk pool of covered employees grows “older and less healthy,” which makes workers more expensive to cover.

While the main provisions of the Affordable Care Act don't kick in until 2014, two measures that took effect in September 2010 could have affected the cost of coverage this year. The first allows adult children up to age 26 to be covered on their parents' policies. An estimated 2.3 million young adults receive coverage through their parents' policies because of the new law, the survey found.

“This is a concrete, tangible product of the ACA, and a very popular benefit according to our polls,” Altman said.

The second provision requires that new plans cover certain preventive medical services with no patient cost-sharing. Some 47 million Americans were helped by this measure, with 23 percent of covered workers in plans that lowered their co-payments for preventive services and 31 percent in plans that added preventive services at no extra cost to members.

Effective this month, the new health law requires insurers that are seeking rate increases of 10 percent or more on new policies to disclose the moves publicly and have them reviewed by state or federal officials to determine whether they're unreasonable.

© 2011 McClatchy-Tribune Information Services

Truthout has licensed this content. It may not be reproduced by any other source and is not covered by our Creative Commons license.

Important Message: Please Read

For 25 years, Truthout has survived by publishing impactful investigative journalism and analysis; distributing full editions 365 days a year; and building a community of readers who support us with small, hard-earned donations.

Eighty percent of our $3 million yearly budget comes from small donors alone. Of those, 8,000 readers support us with monthly donations. Back in 2018, when Facebook decided to suppress the circulation of posts made by organizations, thereby cutting readers off from seeing many articles shared by the news organizations they had intentionally decided to follow, Truthout’s total traffic declined by 40 percent, as nearly all of our traffic from that platform disappeared.

Now, Google has recently rolled out its AI search bar, providing AI summaries instead of directing readers to our site. Google Search is our single largest source of traffic; it’s the route by which nearly one third of our readers find us. Much like in 2018, a shocking 40 percent of our Google traffic has disappeared overnight.

It will not be easy for Truthout to shoulder this blow. Nor will it be easy for our peers and collaborators — news sites that depend on traffic and aren’t bankrolled by large corporations.

If you can support Truthout with a donation today, you can help us resist the AI onslaught. Please give today.