Honest, paywall-free news is rare. Please support our boldly independent journalism with a donation of any size.

It is strangely comforting to see that the United States is not alone as it struggles in its morass of failed fiscal policy.

P. O’Neill, a regular contributor to the online magazine A Fistful of Euros, has published some good observations on the mess that followed Ireland’s 2009 plunge into harsh austerity. He writes that the debt crisis has led to Irish banks, “owning businesses they never expected to, so that they are now operating hotels that they have taken over and selling repossessed farm equipment.

“But there is a strange flip side to this situation,” he writes. “There is exactly one sector of the economy that the government has declared off limits from the process of debt distress, restructuring and external management – the banking sector.”

The author suspects the worst is not over: “Recognizing the scale of the restructuring that needs to be done, you’d think there would be a rush to get it done as quickly as possible and reduce some of the debt overhang. Not necessarily.”

So what are the rewards for Ireland’s fiscal toughness? There don’t seem to be any.

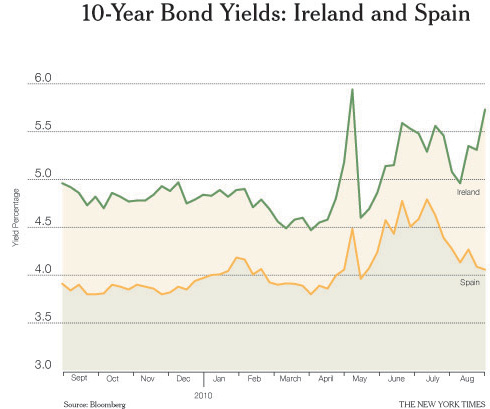

A couple of months ago I posed a different question: Does fiscal austerity actually reassure the markets? After Ireland quickly and bravely embraced savage austerity, quite a few press reports declared that it had regained the confidence of the markets, but the actual numbers showed otherwise. I compared Ireland with Spain, which has been relatively slow and reluctant to embrace austerity, but has been treated no worse by investors.

Before the financial crisis hit, Ireland’s and Spain’s revenues were buoyed by immense real estate bubbles. When the bubbles burst, both governments found themselves on the hook for massive losses.

Keeping in mind that bond yields always move in the opposite direction of prices – if there is market demand for a bond, the yield will generally decrease; if demand is low, the yield increases – look at the 10-year bond yield numbers for Ireland on the graphic on this page. Since austerians have been claiming that bond market approval is a sign of fiscal policy success, it is worth pointing out that dutiful Ireland looks as if it’s entering a runaway debt spiral, while malingering Spain is looking considerably better. It is true that Ireland’s bubble was even bigger than Spain’s, so you could say that’s the issue.

But the simple fact is that the contrast between nations is striking.

——————————

BACKSTORY: Austerity’s Drawbacks

While both Ireland and Spain enacted strict fiscal austerity programs to curb bloated budget deficits during their recent sovereign debt crises, Ireland’s economy appears to have fared substantially worse.

In August, Lloyd’s Banking Group even called a halt to its business-lending activity in Ireland, citing the nation’s lack of growth prospects as the reason for the decision.

This move came after Lloyd’s suffered a $3.43 billion loss in Ireland during the first half of this year. However, this is just a fraction of the total loan losses that credit-rating agency Standard & Poor’s projects for the country’s banking sector – a sobering $30.5 billion. On the basis of this projection, S.&P. downgraded the nation’s credit rating a notch.

In contrast, Spain’s economy has fared a bit better under austerity. On Aug. 18, the country announced plans to restore 500 million euros in funding that had been cut from infrastructure investment budgets – a stimulus measure that signals the Spanish government’s desire to balance fiscal discipline with economic growth. Officials say they plan to do so without raising taxes; they were able to restore the funding because debt servicing costs proved to be lower than expected.

On the other hand, the government announced on Aug. 31 that unemployment had risen to 20.3 percent in July, the highest rate reported in a euro zone country since the single currency was introduced in 1999, according to the Financial Times. Ireland’s unemployment rate during that period was 13.6 percent.

Also, the latest estimates from S.&P.’s predict that Ireland’s debt will reach 113 percent of gross domestic product this year – one of the highest proportions in the euro zone, with Spain’s at 65 percent. But the agency did offer some positive news for Ireland’s long-term outlook: the firm estimates the deficit will be just 5 percent of G.D.P. by 2014.

Copyright 2010 The New York Times.

Truthout has licensed this content. It may not be reproduced by any other source and is not covered by our Creative Commons license.

Paul Krugman joined The New York Times in 1999 as a columnist on the Op-Ed page and continues as a professor of economics and international affairs at Princeton University. He was awarded the Nobel in economic science in 2008.

Mr. Krugman is the author or editor of 20 books and more than 200 papers in professional journals and edited volumes, including “The Return of Depression Economics” (2008) and “The Conscience of a Liberal” (2007).

Important Message: Please Read

For 25 years, Truthout has survived by publishing impactful investigative journalism and analysis; distributing full editions 365 days a year; and building a community of readers who support us with small, hard-earned donations.

Eighty percent of our $3 million yearly budget comes from small donors alone. Of those, 8,000 readers support us with monthly donations. Back in 2018, when Facebook decided to suppress the circulation of posts made by organizations, thereby cutting readers off from seeing many articles shared by the news organizations they had intentionally decided to follow, Truthout’s total traffic declined by 40 percent, as nearly all of our traffic from that platform disappeared.

Now, Google has recently rolled out its AI search bar, providing AI summaries instead of directing readers to our site. Google Search is our single largest source of traffic; it’s the route by which nearly one third of our readers find us. Much like in 2018, a shocking 40 percent of our Google traffic has disappeared overnight.

It will not be easy for Truthout to shoulder this blow. Nor will it be easy for our peers and collaborators — news sites that depend on traffic and aren’t bankrolled by large corporations.

If you can support Truthout with a donation today, you can help us resist the AI onslaught. Please give today.