Truthout is a vital news source and a living history of political struggle. If you think our work is valuable, support us with a donation of any size.

After the news broke in May of last year that government-sponsored lending agency Freddie Mac had agreed to back $786 million in loans to the Kushner Companies, political opponents asked whether the family real estate firm formerly led by the president’s son-in-law and top adviser, Jared Kushner, had received special treatment.

“We are especially concerned about this transaction because of Kushner Companies’ history of seeking to engage in deals that raise conflicts of interest issues with Mr. Kushner,” Sens. Elizabeth Warren, D-Mass., and Tom Carper, D-Del., wrote to Freddie Mac’s CEO in June 2019.

The loans helped Kushner Companies scoop up thousands of apartments in Maryland and Virginia, the business’s biggest purchase in a decade. The deal, first reported by Bloomberg, also ranked among Freddie Mac’s largest ever. At the time, the details of its terms weren’t disclosed. Freddie Mac officials didn’t comment publicly then. Kushner’s lawyer said Jared was no longer involved in decision-making at the company. (He does continue to receive millions from the family business, according to his financial disclosures, including from some properties with Freddie Mac-backed loans.)

Freddie Mac packaged the 16 loans into bonds in August 2019 and sold them to investors. But Kushner Companies hadn’t finished its buying spree. Within the next two months, records show, Freddie Mac backed another two loans to the Kushners for an additional $63.5 million, allowing the company to add two more apartment complexes to its portfolio.

A new analysis by ProPublica shows Kushner Companies received unusually favorable loan terms for the 18 mortgages it obtained with Freddie Mac’s backing. The loans allowed the Kushner family company to make lower monthly payments and borrow more money than was typical for similar loans, 2019 Freddie Mac data shows. The terms increase the risk to the agency and to investors who buy bonds with the Kushner mortgages in them.

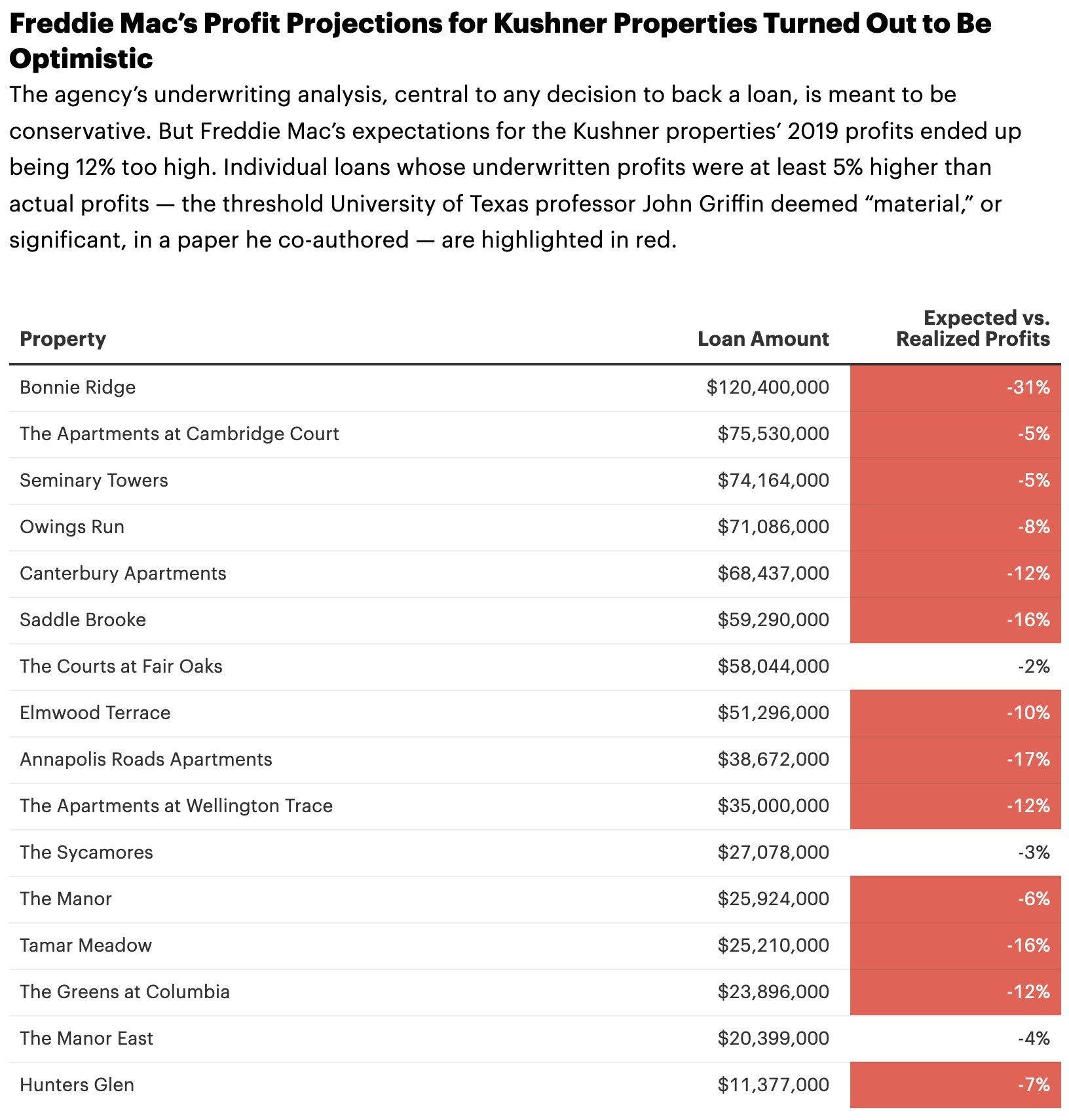

Moreover, Freddie Mac’s estimates of the Kushner properties’ profitability — a core element of any decision to back a loan — have already proven to be overly optimistic. All 16 properties in the firm’s biggest loan package delivered smaller profits in 2019 than Freddie Mac expected, despite the then-booming economy. The loan for the largest property lagged Freddie Mac’s profit prediction by 31% last year.

U.S. taxpayers could be responsible for paying back much of the nearly $850 million in Freddie Mac financing if Kushner Companies defaults and its properties drop significantly in value. Freddie Mac said that’s unlikely. But during the last real estate crash, taxpayers had to bail out the agency and its larger sibling, Fannie Mae, to the tune of $190 billion as the agencies plunged into the government equivalent of bankruptcy. (The agencies ultimately repaid the money and more.)

The involvement of Jared’s sister Nicole Kushner Meyer adds to questions about whether the family sought to exploit its political influence. Meyer, who shares her brother’s slight build, porcelain features and dark chestnut hair, lobbied Freddie Mac in person on behalf of Kushner Companies in February last year, a timeline of the deal obtained by ProPublica shows. She has previously drawn criticism for invoking her brother’s name while doing Kushner Companies’ business.

In a statement, Freddie Mac said it does “not consider the political affiliations of borrowers or their family members.” It called ProPublica’s analysis “random, arbitrary and incomplete” and asserted that the Kushner loans “fit squarely within our publicly-available credit and underwriting standards. The terms and performance of every one of these loans is transparent and available on our website, and all the loans are current and have been consistently paid.”

A spokesperson for Kushner Companies did not respond to calls and emails seeking comment. Emails to the White House seeking Jared Kushner’s comment were not returned.

There’s no evidence the Trump administration played a role in any of the decisions, and Freddie Mac operates independently. But Freddie Mac embarked on approving the loans at the moment that its government overseer, the Federal Housing Finance Agency, or FHFA, was changing from leadership by an Obama administration appointee to one from the Trump administration, Mark Calabria, Vice President Mike Pence’s former chief economist. Calabria, who was confirmed in April 2019, has called for an end to the “conservatorship,” the close financial control that his agency has exerted over Freddie Mac and Fannie Mae since the 2008 crisis.

The potential for improper influence exists even if the Trump administration didn’t advocate for the Kushners, said Kathleen Clark, a law professor at Washington University specializing in government and legal ethics. She compared the situation to press reports that businesses and associates connected to Jared Kushner and his family were approved to receive millions from the Paycheck Protection Program. Officials could have acted because they were seeking to curry favor with the Kushners or feared retribution if they didn’t, according to Clark. And if Kushner Companies had wanted to avoid any appearance of undue influence, she added, it should have sent only nonfamily executives to meet with Freddie Mac. “I’d leave it to the professionals,” Clark said. “I’d keep family members away from it.”

The Freddie Mac data shows that Kushner Companies secured advantageous terms on multiple points. All 18 loans, for example, allow Kushner Companies to pay only interest for the full 10-year term, thus deferring all principal payments to a balloon payment at the end. That lowers the monthly payments but increases the possibility that the balance won’t be paid back in full.

“That’s as risky as you get,” said Ryan Ledwith, a professor at New York University’s Schack Institute of Real Estate, of 10-year interest-only loans. “It’s a long period of time, and you’re not getting any amortization to reduce your risk over time. You’re betting the market is going to get better all by itself 10 years from now.”

Interest-only mortgages, which notoriously helped fuel the 2008 economic crisis, represent a small percentage of Freddie Mac loans. Only 6% of the 3,600 loans funded by the agency last year were interest-only for a decade or more, according to a database of its core mortgage transactions.

Kushner Companies also loaded more debt on the properties than is usual for similar loans, with the loan value for the 16-loan deal climbing to 69% of the properties’ worth. That compares with an average 59%, according to data for loans with similar terms and property types that Freddie Mac sold to investors in 2019, and is just below the 70% debt-to-value ceiling Freddie Mac sets for loans in its category. “What we generally have seen from Freddie and Fannie,” said Andrew Little, a principal with real estate investment bank John B. Levy & Company, “is they will do 10 years of interest-only on lower-leveraged deals.”

Loans right at the ceiling are “not very common,” Little said, adding that “you don’t see deals this size that commonly.”

Meanwhile Freddie Mac and its lending partner overestimated the profits for the buildings in the Kushners’ 16-loan package by 12% during the underwriting process, according to the agency’s data. Such analysis is supposed to provide a conservative, accurate picture of revenue and expenses, which should be relatively predictable in the case of an apartment building.

But the level of income anticipated failed to materialize in 2019, financial reports show. The most dramatic overstatement came with the largest loan in the deal, $120 million for Bonnie Ridge Apartments, a 960-apartment complex in a suburban part of Baltimore. In that case, realized profits last year were 31% below what Freddie Mac had expected.

“That’s definitely a significant amount,” said John Griffin, a University of Texas professor who specializes in forensic finance and has studied mortgage underwriting. He co-authored a recent paper highlighting as worrisome loans in which projected profits exceeded actual profits by 5%. “It’s a problem when underwritten income is inflated or overstated,” he said. “That is a key metric that determines the safety of the loan.”

Griffin’s paper found that 28% of all loans examined had projected profits that were 5% or more greater than what the properties actually earned in their first year. Some instances of underperformance could be caused by bad luck, the paper acknowledged, but “such situations should be relatively rare.” Yet in the case of Freddie Mac’s estimates in the Kushner deal, 13 of the original 16 loans met or exceeded the 5% threshold — many by a considerable amount.

Freddie Mac said it followed normal underwriting guidelines in assessing the Kushner buildings, including securing an independent appraisal and looking at historical property performance. It said investors who examined the riskiest portion of the debt also expressed no concerns.

If the underwriting had been on target, and reflected lower expectations, the loans would still have been within Freddie Mac’s credit parameters, data shows. But the resulting analysis would have suggested the Kushner Companies has a smaller cushion to sustain its loan payments. It could also have affected the interest rate the company pays. Thinner margins accompanied by relatively high rates of debt provide less wiggle room if the properties, or the economy, run into trouble. As Kushner Companies has seen before, that wiggle room can disappear quickly.

Freddie Mac’s main business has historically been buying bundles of home loans from the lenders that originated them, then selling them to investors as securities. The arrangement takes the debt off banks’ balance sheets, freeing them to make more loans. Freddie Mac and Fannie Mae are privately owned, but they have been financially backstopped by the federal government and are required to meet goals for lending on affordable housing.

Single-home loans are still Freddie Mac’s primary business, but since the 2008 economic crisis, the agency has greatly expanded its financing of apartment complexes.

Apartment complexes have been the specialty of the Kushner family, whose real estate holdings have spanned the mid-Atlantic and Midwest in recent years, with thousands of units scattered across suburbia. The company sold off 17,500 apartments in 2007, after the family’s patriarch, Jared’s father, Charles Kushner, returned from prison for convictions on illegal campaign contributions, tax evasion and witness tampering.

After Jared became CEO in 2008, the company turned its ambitions to high-profile commercial properties in New York City, a foray that turned sour. In 2018, the company gave up control of its marquee $1.8 billion building and headquarters, 666 Fifth Avenue, after being unable to keep up with its loans. Another piece of prime Kushner Companies Manhattan real estate, retail space in the old New York Times building near Times Square, was headed for a potential default in 2019, and foreclosure. (The New York Times reported in August that the foreclosure action was put off at the last minute, so negotiations with a lender could continue.)

Kushner Companies eventually resumed its residential focus and began bulking up its apartment portfolio. In the eight years before Trump entered the White House, the company and its partners secured a total of $581 million in Freddie Mac financing, according to data from the firm Real Capital Analytics first published by Bloomberg. By the end of 2018, Kushner Companies had amassed 21,000 apartment units.

Some of those loans didn’t fare well. They included a series of supplemental loans, or second mortgages, taken out on properties in Maryland that Kushner Companies owned in partnership with others (the size of the Kushner share was not clear). Landlords often use such second loans as a way to extract large amounts of cash from their holdings.

A lender had originated 10 such loans to Kushner Companies and its partners in 2015, and Freddie Mac planned to sell them to investors, or securitize them, once the properties demonstrated income consistently high enough to cover the debt payments. For four of the properties, however, profits dipped in 2016, and two more were in little better shape. Freddie Mac still hadn’t securitized the six loans, for $40 million, by inauguration day in 2017.

Mortgage industry experts say poor profits at underlying properties can lead Freddie Mac to delay selling off the loans as bonds, fearing they will be rejected by investors. By the time Freddie Mac offloaded the last of Kushner’s second mortgages in April 2017, they had racked up above-average lag times between their origination and securitization, compared with other loans in their debt packages, data shows. (Freddie Mac said the wait time was normal.)

Within 10 months of the sale of the loans to investors, one of the complexes landed on the servicer’s watchlist for mortgages at a heightened risk for default. Another soon followed, and another the year after that. All 10 complexes, which were built in the early 1970s or earlier, exhibited upkeep issues alarming enough to earn a flag in Freddie Mac data for “deferred maintenance” problems. (A Freddie Mac spokesman said the issues identified were almost all related to exterior asphalt and concrete, with one instance of an exterior drainage system in need of repair.)

At one property, a representative of Kushner Companies and its partners blamed residents of the nearby neighborhoods, who are primarily Black and low-income, for its declining profits and a rash of evictions: “The main driver is the client base in the area,” the servicer reported the borrower as saying, Freddie Mac records show.

Kushner Companies had other problems, too. In 2017, ProPublica reporter Alec MacGillis documented the company’s practice of charging aggressive, and what some tenants’ lawyers called illegal, fees to occupants of some of those complexes. Tenants also claimed Kushner Companies’ property management arm, Westminster Properties, at times neglected basic repairs and allowed the property condition to deteriorate, including raw sewage flowing out of one kitchen sink.

The complaints spurred a lawsuit filed in October 2019 by the attorney general of Maryland, Brian Frosh. Frosh accused the management company and its partners of charging “illegitimate fees” and having “rented apartments and townhomes to consumers that are distressed, shoddily maintained, and have conditions that can adversely impact consumers’ health and well being.” (Westminster has defended its conduct in legal filings for the suit, which remains active.)

Kushner Companies first approached Freddie Mac in August 2018 through Berkadia Commercial Mortgage, then abandoned its application without explanation in mid-October of that year. Berkadia did not return messages seeking comment.

In February 2019, Berkadia approached Freddie Mac again and informed the agency that Kushner Companies wanted to move forward. It’s not clear what explains the renewed interest. But two things had changed in the interim. The rates on 10-year Treasury bonds had dropped, a circumstance that typically fuels borrowing and the securitized lending that Freddie provides. And the Obama appointee in charge of the FHFA was gone, leaving an interim Trump appointee in place.

Six days after rekindling its interest, Nicole Kushner Meyer and two Kushner Companies executives, President Laurent Morali and Chief Operating Officer Peter Febo, met with Freddie Mac officials, along with representatives of Berkadia and an advisory firm, documents show. The records don’t say which Freddie Mac officials attended. The meeting covered the “business plan for assets, track record and general overview of the Kushner Companies.” Meyer followed up, documents say, sending multiple emails to a senior Freddie Mac official, who was not identified.

Meyer has been serving as a principal at Kushner Companies since 2015, according to her LinkedIn profile. She caused a stir in 2017, when she invoked her brother on a trip to China to pitch potential investors for a Kushner Companies development in Jersey City, New Jersey. The company was seeking investors to participate in a government program known as EB-5, which grants visas to foreigners who make high-dollar investments intended to create jobs in struggling areas.

Freddie Mac said Meyer did not mention Kushner by name during the meeting. The agency also said no one connected to the White House asked that the deal be done.

But the political sensitivity was obvious to Freddie Mac, whose officials emailed each other in the weeks after the meeting, expressing a desire to minimize press coverage of the deal, according to a person with knowledge of the situation. They also took the unusual step of notifying FHFA, their regulator, of the transaction, the timeline shows. Freddie Mac and FHFA both declined to say why Freddie made the notification except to say that it was necessary as part of the agency’s conservatorship. (One source suggested deals above a certain dollar amount require such notification.)

In March, Kushner Companies was able to move fast to lock in a favorable interest rate, documents show. It submitted a financing application, which is needed to request a lock on a component of its interest rate. Freddie Mac’s website says that single loans are eligible for such a procedure, but that groups of loans must obtain additional approval. The day after Kushner Companies submitted its application, documents show, Freddie locked the rate for all 16 mortgages.

Through a spokesman, Freddie Mac said that such locks are an important part of its business model, and that timing is at the borrower’s discretion.

Kushner Companies’ full-term interest-only loan proved exceptional in another way: Freddie Mac had granted Lone Star Funds, a private equity firm managing $85 billion in global investments, interest-only terms for only the first three years of its seven-year mortgages when it had acquired the same apartment complexes in 2015. As a result, Lone Star had been able to borrow more money. But it soon faced a sharp hike in its monthly payments, when it added principal to interest.

(Freddie Mac said full-term, interest-only loans are more common when the pool of mortgages examined is restricted to larger, conventional loans. Nonpublic data shows they made up roughly 20% of such loans over the last three years, the agency said.)

Freddie Mac completed its due diligence for the Kushner Companies deal and on May 22 of last year, Kushner Companies and its partner, Torchlight Investors, took ownership of the 16 properties, with $785,803,000 in loans pledged. Torchlight did not respond to questions.

The properties were largely in the Washington, D.C., and Baltimore suburbs. Their average construction date was 1980, almost a decade older than the other properties Freddie approved for similar loans in 2019.

From a profit standpoint, the 16 properties were a mixed bag. Appraisers pegged their value as having increased 2% overall in the previous four years. Four of the properties lost value, according to the analysis.

The Kushners also benefited from another provision that increased the deal’s risk. Groups of loans are often cross-collateralized, meaning that if one defaults, the lender can seek to seize others to recoup their losses. The strategy provides an extra hedge against risk for the lender. The Lone Star properties were cross-collateralized under their previous loan. But not those for Kushner Companies. (A Freddie Mac spokesman said cross-collateralization is not required and each of the company’s loans met credit parameters without it.)

Another curious phenomenon emerged in the disclosures for the new loans: The reported profits for seven of the Kushner buildings in 2017 were higher than those listed for the same buildings and same year in prior loan documents. For some properties, the difference was slight. But for others, it was more substantial. At one Kushner complex, for example, the Apartments at Cambridge Court in suburban Baltimore, the 2017 net operating income was nearly 6% higher in the new loan filing than it had been for the same year in an old disclosure.

In May, ProPublica reported a pattern of similar discrepancies in bonds that hold mortgages across the commercial real estate industry. And the paper by Griffin, the University of Texas finance professor, and his colleague Alex Priest also found a pattern of such profit alterations, suggesting multiple institutions are manipulating historical financials to downplay risk and bolster more aggressive lending.

Financial data on how the 18 Kushner properties are faring in this year’s economic slump is not yet available.

An urgent appeal for your support: We Have Until Midnight to raise $13,000

Truthout relies on individual donations to publish independent journalism, free from political and corporate influence. In fact, we’re almost entirely funded by readers like you.

Unfortunately, donations are down. At a moment when independent journalism is urgently needed, we are struggling to meet our operational costs due to increasing political censorship.

Truthout may end this month in the red without additional help, so we launched a fundraiser. We have until midnight tonight to hit our $13,000 goal. Please make a tax-deductible one-time or monthly donation if you can.