Did you know that Truthout is a nonprofit and independently funded by readers like you? If you value what we do, please support our work with a donation.

One of the good ideas in a now-essential recent paper by Paul De Grauwe, a professor of economics at the University of Leuven in Belgium and a research fellow at the Center for European Policy Studies, was to do a head-to-head comparison of Spain and Britain to illustrate the problems the euro faces.

Here’s an update.

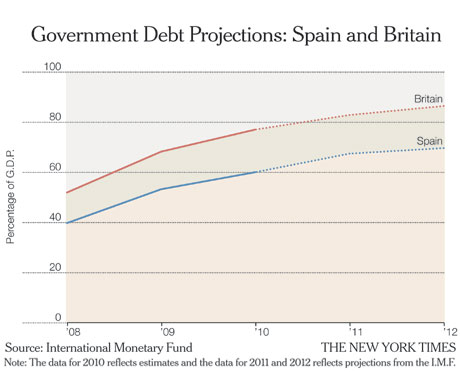

First, see the fiscal outlook for Spain and Britain, illustrated by the graphic on this page (using the most recent data and projections from the International Monetary Fund).

Spain started off with low debt, and despite the severity of its slump is expected to have, if anything, less increase in debt than Britain.

Yet markets are acting as if Spain is highly risky, while treating British bonds as a safe haven, like American or German bonds.

To some extent this may reflect the reality that British growth prospects are better because of the depreciated pound, and also the fact that Britain won’t have to deflate the way Spain will, thanks to Spain’s adopting the euro. But I believe that Mr. De Grauwe is right that the most important factor is that Britain, which can turn to the Bank of England for financing if necessary, doesn’t face the risk of a run by creditors the way Spain does.

What’s needed, clearly, is for Europe — and, ultimately, that probably means the European Central Bank — to provide for Spain and Italy the kind of backstop countries with their own currencies can provide for themselves. Without that, the whole euro system is at risk of unraveling, not over the course of years, but over the course of a few weeks.

Oh, and Britain should give thanks to Gordon Brown, the former chancellor and prime minister, who kept the nation out of the euro zone.

Stimulus Spending And Double Standards

Just a quick thought: in much of the discussion about economic policy these days, the presumption is that stimulus had its chance, it failed, and that’s that. Never mind those of us who say that we actually didn’t do nearly enough — and were saying that from the beginning, not as an after-the-fact rationalization. It’s one strike and you’re out.

Meanwhile, the pain caucus keeps telling us that austerity is the way to restore confidence, and confidence keeps not being restored. Ireland, for example, has imposed savage austerity, yet the interest rate on its 10-year bonds is still 6.7 percentage points higher than Germany’s, down from recent peaks but still far above its level when the austerity program began.

Yet somehow nobody in the pain caucus says “Hey, this was supposed to work but it didn’t, so our theory is all wrong.” Instead, they just insist that we double down, continuing the beatings until morale improves.

Just saying.

Truthout has licensed this content. It may not be reproduced by any other source and is not covered by our Creative Commons license.

Paul Krugman joined The New York Times in 1999 as a columnist on the Op-Ed page and continues as a professor of economics and international affairs at Princeton University. He was awarded the Nobel in economic science in 2008.

Mr Krugman is the author or editor of 20 books and more than 200 papers in professional journals and edited volumes, including “The Return of Depression Economics” (2008) and “The Conscience of a Liberal” (2007). Copyright 2011 The New York Times.

Fundraiser Deadline: Missed

Truthout is one of only a few platforms for justice-oriented, grassroots journalism. Today, as political censorship from the right intensifies, we have no choice but to ask for your help.

We missed our fundraising deadline, but there’s still time to help us meet our basic operating expenses before the end of the month. If you can support Truthout with a one-time or monthly donation, you will make a significant impact on our work. Anything you can do makes a difference — we appreciate your support.