Truthout is a vital news source and a living history of political struggle. If you think our work is valuable, support us with a donation of any size.

Washington – Wondering who to thank for the bizarre rules that allow Congress to approve spending, then later slam the door on new borrowing to pay the bills? Thank the Founding Fathers.

Article 1 of the U.S. Constitution grants Congress the exclusive powers to legislate and the power of the purse. In fact, Section 8 of the first article deals specifically with paying debts.

But the Constitution’s Article 2 empowers the president to carry out the laws passed by Congress and run the government at the levels authorized and appropriated by Congress.

In that simple civics lesson is the root of the problem. Congress passes legislation to spend, but it’s the president who must ensure those bills get paid. Those two objectives don’t neatly line up. President Barack Obama complains that past presidents haven’t been subjected to the types of conditions being asked of him in exchange for lifting the debt ceiling, but it just isn’t true. To the contrary, there’s plenty of precedent.

“In the past, Congress has responded to make sure that the Treasury can still keep borrowing, but debt and budgets have always been contentious,” said D. Andrew Austin, an analyst in government finance for the nonpartisan Congressional Research Service and the author of a brief but thorough history of the debt limit.

His research shows that fights over installing a new cap on the nation’s debt are hardly a new phenomenon.

“While the debt limit has never caused the federal government to default on its obligations, it has at times caused great inconvenience and has added uncertainty to Treasury operations,” Austin wrote.

The Constitution created the backdrop for fights between Congress and the president over spending and taxes, but the actual statutory limit on just how much debt the federal government can incur began almost 100 years ago, with the Second Liberty Bond Act of 1917.

Before then, Congress had from time to time given the Treasury Department authority to issue bonds to raise money for special projects. And Congress had authorized borrowing for specific reasons such as for building the Panama Canal.

The issuance of long-term Liberty Bonds changed the game. They were authorized so that the federal government could better hold down its borrowing costs as it funded America’s entry into World War I. In 1919, the debt ceiling was about $43 billion, but at the close of the fiscal year debt actually stood at about $25.5 billion, with Congress reluctant to borrow all that was authorized.

Several decades of congressionally mandated debt limits followed, and it gave Treasury officials more autonomy to issue debt. Austin’s report notes that at the start of World War II, the U.S. debt ceiling of $45 billion was just 10 percent higher than the $40.4 billion in actual debt. Actual borrowing matched up more neatly with authorized amounts. Until the cost of World War II exploded, that is. By 1945, the debt ceiling was set at $300 billion.

The debt ceiling actually fell, to $270 billion, after the war and stayed there until about 1954. The Korean War was paid for through higher taxes, not more debt. And between 1954 and 1962, the debt limit fell twice and increased seven times. It didn’t return to the World War II high-water mark again until March 1962.

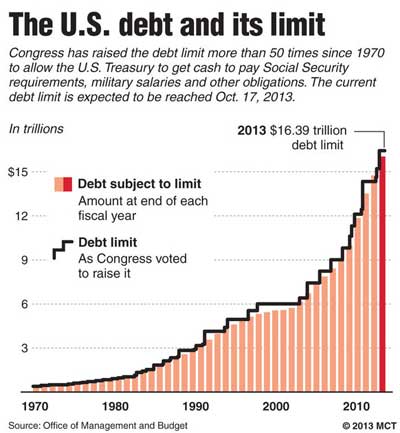

From that point forward, there were 69 changes to the debt limit through the end of the 2007-2008 fiscal year, including the largest single-chunk increase, $984 billion in May 2003, as America borrowed to pay for wars in Afghanistan and Iraq while also cutting taxes.

From that point forward, there were 69 changes to the debt limit through the end of the 2007-2008 fiscal year, including the largest single-chunk increase, $984 billion in May 2003, as America borrowed to pay for wars in Afghanistan and Iraq while also cutting taxes.

During the 1980s and early 1990s, there was brief respite from the politicization of the U.S. debt ceiling. Lawmakers had grown tired of passing spending increases and then voting against raising the debt ceiling for their profligate spending. It made them appear hypocritical in front of the voters, and that second vote to allow more borrowing never played well back home.

In 1979, up-and-coming Missouri Democrat Dick Gephardt, who later became House majority leader, won a parliamentary ruling that allowed any final vote on a budget to automatically raise the debt ceiling.

The so-called Gephardt Rule was welcomed by both major political parties because it eliminated the need to take that separate and politically costly vote to raise the debt ceiling. Over time, it lost its luster because senators amended the budget passed by the House, meaning it had to come back to the House for another vote, which had the same effect as voting to raise the debt ceiling.

The Gephardt Rule, however, ended when Republicans took back the House of Representatives in the 104th Congress and in 1995 Georgia Republican Newt Gingrich became House speaker. He saw an opportunity to use the debt ceiling for political leverage

“It was looked at by conservatives as another opportunity to take a whack at the fiscal situation . . . since the Senate was historically amending the debt limit,” said William Hoagland, a former Republican staff director for the Senate Budget Committee.

Since the demise of the Gephardt Rule, whichever political party controlled the Congress has generally used the debt ceiling as a political tool, returning to the 1970s practice of increasing spending but also voting against raising the debt ceiling.

In one example, Sen. Barack Obama took to the Senate floor on March 16, 2006, in opposition to raising the debt ceiling while George W. Bush was president.

“Increasing America’s debt weakens us,” Obama argued then.

That month, China held $635.4 billion in U.S. government debt. By this July, that number had doubled to nearly $1.28 trillion.

Some experts actually see value in the frequent fights over raising the debt ceiling, because they force the two major parties to bridge divides.

“In fact, debt limit increase bills have served not only as vehicles for bipartisan fiscal reform measures, but catalysts for subsequent negotiations about debt reduction,” wrote Anita Krishnakumar in the 2005 edition of the Harvard Journal of Legislation.

“Upon careful evaluation, it is clear that the statute retains enduring value.”

Press freedom is under attack

As Trump cracks down on political speech, independent media is increasingly necessary.

Truthout produces reporting you won’t see in the mainstream: journalism from the frontlines of global conflict, interviews with grassroots movement leaders, high-quality legal analysis and more.

Our work is possible thanks to reader support. Help Truthout catalyze change and social justice — make a tax-deductible monthly or one-time donation today.