Senate Majority Leader Sen. Mitch McConnell and other Republicans speak to the press after the Senate passed tax reform legislation on Capitol Hill December 19, 2017, in Washington, DC. Brendan Smialowski / AFP / Getty Images

The House Republican “2.0” tax plan contains new provisions that are supposedly aimed at promoting savings, the most troubling of which is a proposal to introduce “Universal Savings Accounts” (USAs). A USA is a new type of tax-preferred account that’s similar to a Roth Individual Retirement Account (Roth IRA) but would have no income limits for participation and would let an individual withdraw funds before retirement. As we’ve written, the USA is fundamentally flawed: it would do little to boost private savings, it would drain federal revenues, and it overwhelmingly benefits the nation’s wealthiest households.

The USA proposal would come along with the centerpiece of the House 2.0 plan, which is its permanent extension of the 2017 tax law’s individual provisions that are slated to expire after 2025. As we’veexplained, that extension would be fiscally irresponsible and would favor the wealthiest Americans.

As for USAs, they would:

Do little to boost savings.Rep. David Brat — who authored a previous USA proposal — haspromotedthe accounts as a “more streamlined and flexible saving account option that will truly encourage savings.” In reality, they won’t increase savings much at all. That’s because, according to high-qualityresearchby Harvard economist Raj Chetty and his co-authors, this type of tax-based savings incentive mostly subsidizes saving that households would have done anyway. Overall, every dollar of tax-cut benefit only increased savings by one cent, Chetty and his co-authors estimated.

The main effect of USAs, therefore, would likely be that some households would shift assets from taxable investment and savings vehicles — including regular savings accounts, the interest income from which is taxable — into USAs and receive a tax cut without increasing their savings.

Drain federal revenue.USAs would drain federal revenues because — as with Roth IRAs — investment earnings would escape taxation. The cost could be substantial as households shift increasing amounts of savings from taxable accounts intoUSAs. The Joint Committee on Taxation estimates that the USA provision will cost $8.6 billion over ten years. Yet, as we’veexplained, that’s likely an understatement of its true long-run cost since the benefit of not paying tax on investment earnings is backloaded into later decades as more assets shift into USAs and those assets grow in value.

The cost may also be understated if some people shift new contributions from an existing tax-preferred account, such as a 401(k) or traditional IRA, to a USA account, since that would change thetimingof their tax benefits; the existing accounts provide their tax benefits up frontrather than at a future time of withdrawal. That would make the costs smaller in the first ten years than in subsequent decades without reducing their actual, long-run cost.

Mostly help the wealthy and do little for households in the middle and at the bottom.The wealthy are best positioned to take advantage of USAs’ main tax benefit — reducing tax liability by shifting savings from taxable accounts to tax-preferred USAs — because they have substantial assets in taxable accounts that they could shift into USAs. Households in the top 1 percent of wealth have, on average, $9.4 million in assets that they could shift into USAs, while the average household in the middle 60 percent has just $16,000 that it could shift. Given USAs’ $2,500 per-adult contribution limit, a married couple with $16,000 in USA-eligible savings would need roughly four years to shift its existing eligible assets, after which these households could get an additional tax break only by boosting their savings rate. In the end, wealthy households would get a hefty tax cut that grows over time, while a wide swath of households at the bottom or in the middle would get far less.

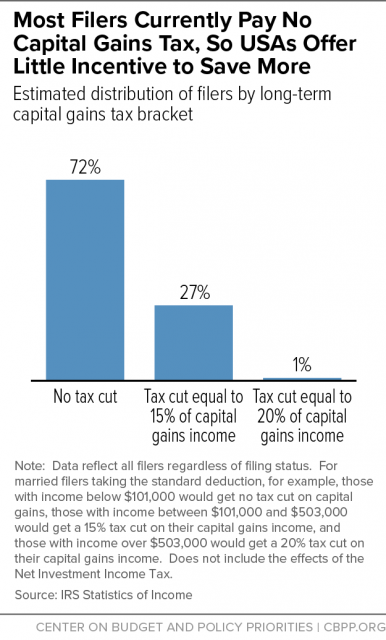

USA benefits are tilted to the top in another important way: the tax savings would be proportional to a household’s tax rate on investments. Take, for instance, capital gains — the gains from the sale of stocks or other assets. The top tax rate on long-term capital gains is 20 percent, but the rate is 0 for a married couple making up to about $100,000. Thus, that married couple would receive no additional tax benefit from holding such assets in a USA as opposed to a taxable account; either way, the couple would pay no tax on the gains. More than 70 percent of filers would fall into this group (see chart). By contrast, a married couple making $1 million a year would get a significant tax advantage by shifting its assets into a USA: rather than pay a 20 percent tax on any capital gain, it would payno tax at all.

Thank you for reading Truthout. Before you leave, we must appeal for your support.

Truthout is unlike most news publications; we’re nonprofit, independent, and free of corporate funding. Because of this, we can publish the boldly honest journalism you see from us – stories about and by grassroots activists, reports from the frontlines of social movements, and unapologetic critiques of the systemic forces that shape all of our lives.

Monied interests prevent other publications from confronting the worst injustices in our world. But Truthout remains a haven for transformative journalism in pursuit of justice.

We simply cannot do this without support from our readers. At this time, we’re appealing to add 50 monthly donors in the next 2 days. If you can, please make a tax-deductible one-time or monthly gift today.