Truthout is an indispensable resource for activists, movement leaders and workers everywhere. Please make this work possible with a quick donation.

We just had another electoral earthquake in the eurozone: Candidates backed by the anti-austerity party Podemos have won local elections in Madrid and Barcelona. And I hope that the IFKATs – or the “institutions formerly known as the troika” – are paying attention.

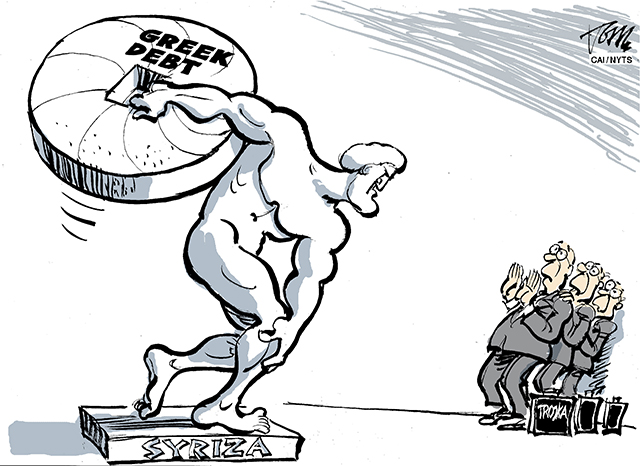

The essence of Greece’s situation today is that the parameters of a short-term deal are clear and unavoidable: Greece can’t run a primary budget deficit, because nobody will lend the country money. And it won’t (and basically can’t) run a large primary surplus, simply because no more blood can be squeezed from that stone. So one would think that an agreement for Greece to run a modest primary surplus over the next few years would be easy to reach. That is what will happen, so why not make it official?

But now the International Monetary Fund is playing bad cop, declaring that it cannot release funds until Greece’s Syriza party toes the line on pensions and labor market reform. The latter involves dubious economics – the I.M.F.’s own research doesn’t support enthusiasm for structural reforms, especially of the labor market. The former probably recognizes a real problem – it’s unlikely that Greece will be able to deliver what it has promised its pensioners – but why should this be an issue over and above the general question of the primary surplus?

What I would urge everyone to do is ask what happens if Greece is, in fact, pushed out of the eurozone. (Yes, it’s called “Grexit” – an ugly word, but we’re stuck with it.)

It would surely be ugly in Greece, at least at first. Right now the core euro countries believe that the rest of the eurozone can handle Greece’s exit, which might be true. Bear in mind, however, that the supposed firewall of support from the European Central Bank has never actually been tested. If markets lose faith and the time for E.C.B. purchases of Spanish or Italian bonds arises, will they really happen?

But the bigger question is what transpires a year or two after Grexit, when the real risk to the euro isn’t that Greece fails, but that it succeeds. Suppose that a greatly devalued new drachma brings a flood of British beer drinkers to the Ionian Sea, and Greece starts to recover. This would greatly encourage challengers to austerity and internal devaluation elsewhere.

Just the other day the Very Serious Europeans were hailing Spain as a great success story, a vindication of the whole austerity program. But, evidently, the Spanish people don’t agree. And if the anti-establishment forces have a recovering Greece to point to, the discrediting of the establishment will accelerate.

An important fundraising appeal: Fell Short of Our Goal

Truthout is one of only a few platforms for justice-oriented, grassroots journalism. Today, as political censorship from the right intensifies, we have no choice but to ask for your help.

We just finished a fundraiser to cover our basic operating expenses for June, but we fell short of our goal. If you can support Truthout with a one-time or monthly donation, you will make a significant impact on our work. Anything you can do makes a difference — we appreciate your support.