Truthout is an indispensable resource for activists, movement leaders and workers everywhere. Please make this work possible with a quick donation.

The economy added 263,000 jobs in November, again coming in ahead of expectations. Perhaps more importantly, wages continue to grow at a rapid pace, as the October average hourly wage was revised up by 6 cents. The annual rate of wage growth over the last three months was 5.1 percent, the same as the rate over the last year.

Wage Growth Is Still Rapid

The rapid pace of wage growth paints a very different picture than we were looking at in October, where the annualized rate was just 3.9 percent. Since we should expect some shift back to wage income, reversing the shift to profits in the pandemic, this would have been roughly consistent with the Fed’s 2 percent inflation target. (There were periods in 2018 and 2019 when wage growth approached 4 percent.) The revised data, coupled with the 0.6 percent growth reported for November, indicate wage growth has yet to slow.

Workers at the Bottom Still Doing Well

Lower paid workers have seen the most rapid wage growth through the pandemic recession and recovery. That continues to be the case. The average hourly wage for production and nonsupervisory workers in hotels and restaurants is up 7.4 percent over the last year.

Divergence Between Establishment and Household Survey Grows

While the unemployment rate remained at 3.7 percent, the employment rate fell by 0.1 percentage point, as the household survey showed a drop in employment of 138,000 in November. Since March the household survey has shown a gain in employment of just 12,000. Over this same period, the establishment survey has shown an increase of 2,692,000 jobs. While large divergences between the surveys are not uncommon, a gap of this size is unprecedented.

The establishment survey is almost certainly closer to the mark. Data on consumption spending and tax collections would be implausible if job growth was anywhere close to the numbers indicated in the household survey. Perhaps BLS will make an extraordinarily large adjustment when new population controls are put in place with the January jobs report.

Other Data in the Household Survey Show Mixed Picture

There were some positive signs in the household survey, apart from the drop in employment rates. The U-6 measure of labor market slack fell back to 6.7 percent, tying the all-time low it hit in September 2022. The employment rate for workers with disabilities rose from 22.0 to 22.3 percent, while their unemployment rate fell to 5.8 percent, both records. The unemployment rate for workers without high school degrees fell to 4.4 percent. This is a record low, although these data are erratic, so it could be driven by measurement error.

There were also some negative signs. The percentage of unemployment due to voluntary quits fell to 13.9 percent. This is down from a record high of 15.9 percent in September 2022. This number is erratic, but a fall of this size likely means workers are feeling less confident about their job prospects. There was also an increase in all the duration measures of unemployment, with the average duration rising by 0.6 weeks to 21.4 weeks and the median increasing by 0.3 weeks to 8.4 weeks. The share of long-term unemployed (more than 26 weeks) jumped by 1.1 percentage points to 20.6 percent.

Strong Job Growth Across Sectors

Most sectors showed strong job growth in November, in spite of the Fed’s efforts to slow the economy. Construction added 20,000 jobs, with even residential construction still showing modest gains, in spite of the sharp fall in housing starts. Employment in the sector is now 126,000 above pre-pandemic levels. Manufacturing added 14,000 jobs, putting employment 149,000 above pre-pandemic levels.

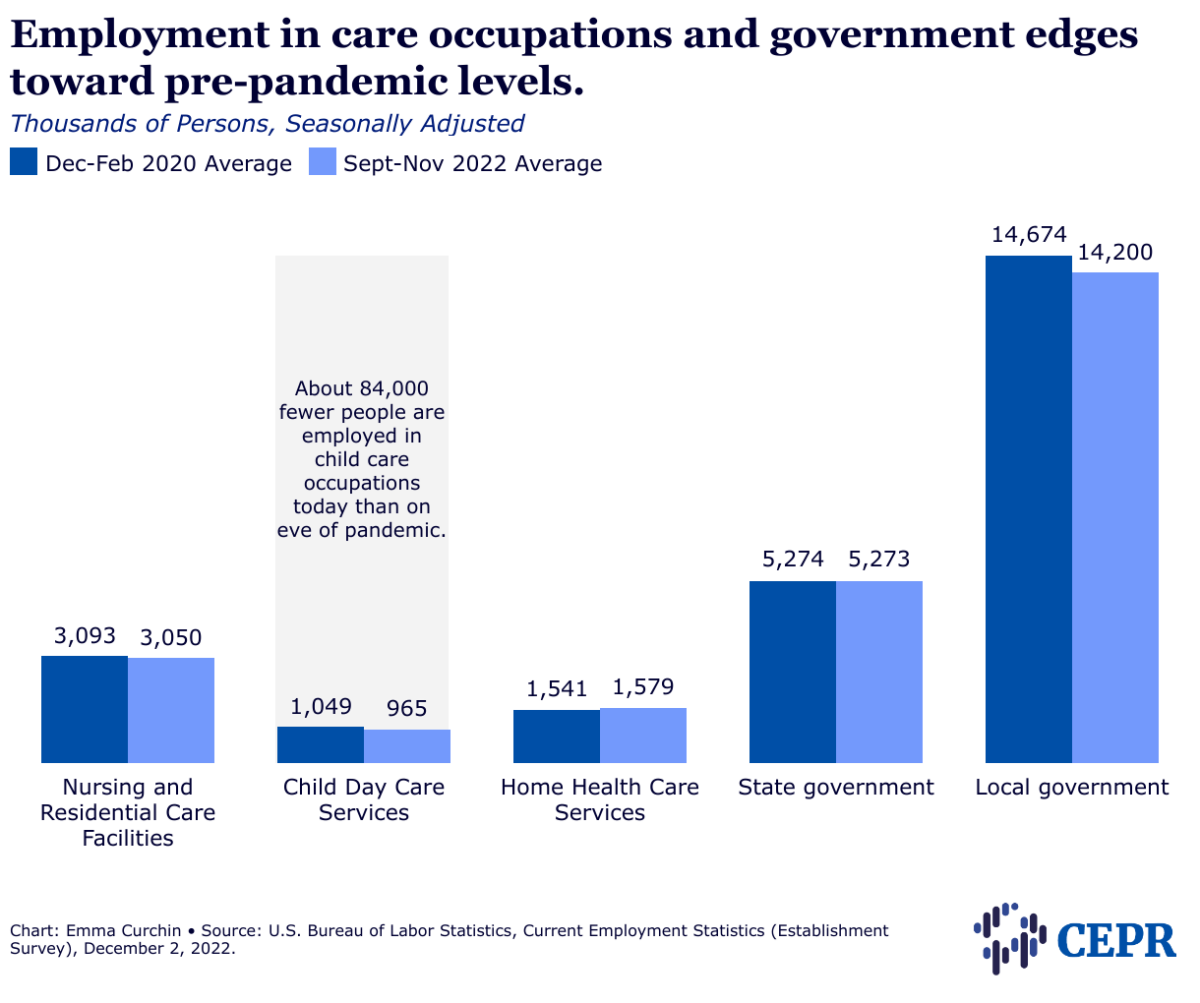

Air transportation added another 4,100 jobs in November, putting employment 58,500 above the pre-pandemic level. Nursing homes and child care facilities added 2,800 and 5,400 jobs, respectively. Employment in nursing homes is now down 215,300 from pre-pandemic levels, while employment in child care centers is down by 84,400.

State and local government added a total of 43,000 jobs in November. Employment in state governments is still down by 26,000 while employment by local government is down by 445,000. Restaurants again showed strong job growth, adding 62,100 workers, while hotels added 15,900.

Retail Continues to Shed Jobs

The retail sector lost 29,900 jobs, with a drop in employment of 32,200 jobs in general merchandise stores accounting for all of the decline. The sector has been losing jobs since February. Jobs in retail are now down 60,700 since the February peak, but still 169,600 above the pre-pandemic level.

The other notable job losses were in the categories of non-depository credit intermediation and activities related to credit intermediations, which lost 11,000 and 2,400 jobs, respectively. These are the sectors that would be most directly hit by the collapse of the mortgage refinancing boom, as well as home purchases. Employment in the two sectors is 38,300 and 15,100, respectively, below peaks hit earlier this year.

Average Workweek Falls by 0.1 Hour

One item going against the generally strong picture in the establishment survey was a drop of 0.1 hour in the length of the average workweek. This was not just an issue of rounding, the index of aggregate weekly hours fell by 0.2 percent, in spite of the strong job growth.

Earlier in the recovery, the length of the workweek had risen, as employers were likely having their existing workforce put in more hours, when they were unable to hire new workers. This no longer seems to be an issue, as the workweek had already fallen back to pre-pandemic levels. It is likely that the November drop in hours reflects some weakening in the demand for labor.

Labor Market Remains Strong in November

This report is a mix of good and bad news. The good news is that the economy is continuing to add jobs at a very rapid pace and that unemployment continues to be near 50-year lows, with some demographic groups seeing their lowest unemployment rate on record.

The bad news is that with the revisions to the October data, and strong wage growth in November, we are still seeing a pace of wage growth that is more rapid than would be consistent with the Fed’s 2 percent inflation target. This likely means that it will continue on its path of aggressive rate hikes for the near future.

Press freedom is under attack

As Trump cracks down on political speech, independent media is increasingly necessary.

Truthout produces reporting you won’t see in the mainstream: journalism from the frontlines of global conflict, interviews with grassroots movement leaders, high-quality legal analysis and more.

Our work is possible thanks to reader support. Help Truthout catalyze change and social justice — make a tax-deductible monthly or one-time donation today.