Over the past few weeks, House and Senate Democratic leaders have been working to craft a compromise between their two health care bills that were passed over the last few months. Today, President Obama has released what Dan Pfeiffer, Communications Director at the White House, is calling the administration’s “best shot” at bridging the differences between the House and Senate.

The proposal comes in advance of the planned February 25 health care summit, where Republicans and Democrats will meet and talk about the health care proposals on the table. The White House thought it would be most productive to “come to the table with one proposal,” as Pfeiffer put it.

Over the last few months, we’ve been fighting to finish health reform right under the rubric of two main goals. By making health care affordable we mean making sure insurance is affordable for individuals, making sure insurance is affordable at work, and making sure middle-class health plans aren’t taxed. By holding insurance companies accountable we mean giving regulators a national exchange so insurance plans in the exchange are subject to the same stringent rules and creating a public health insurance option to hold private insurance companies accountable.

So, what does the President’s plan do?

(Note: The plan starts from the Senate bill as a foundation so any changes listed in the overview of the President’s plan [pdf] are changes to the Senate bill.)

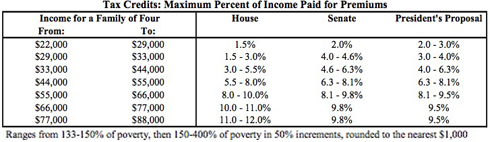

Affordability for Individuals

The President’s plan merges the tax credit schedules of the House and Senate bills for the subsidies an individual or small business would get if they buy health care on the exchange.

As noted previously, the House bill provided much more generous tax credits to lower income people so they could truly afford health care while the Senate bill was more generous for the middle class. The President’s bill has merged these two in a way that makes health care more affordable to both low and middle income people.

Here’s what the subsidies look like in the President’s bill compared to the House and Senate bills:

Affordability at Work

The House bill included a crucial “pay or play” provision that would have required employers to provide good health care at affordable prices to their employees and help small business afford it. If a business didn’t provide health care, it would have had to pay a fee to the government to offset the cost to government of providing health care for uncovered workers.

The Senate, by contrast, does not require all businesses to contribute their fair share. Instead, they’d only pay $750 per worker per year if they left them uncovered and the worker qualified for a subsidy in the exchange.

The President’s plan, though not a full “pay or play” system, moves towards reconciling the House and Senate bills. If a business does not offer coverage, it must pay $2,000 per worker to help cover the cost of insuring its employees. The White House estimates that this amount is one-third less than the average amount businesses would pay under the House proposal.

Taxing Middle Class Plans

The excise tax in the Senate bill would tax many middle class health care plans, making coverage worse and more expensive. The House finances their health care bill by taxing those that can most afford it—households making more than $1 million per year.

The President’s plan does not do away with the excise tax entirely, but it makes some significant changes. The threshold at which the tax kicks in was moved from $23,000 as the cost of a health care plan in the Senate bill to $27,500 for families and from $8,500 to $10,200 for individuals. This would likely exempt millions of middle-class people from the tax.

In addition, dental and vision benefits won’t be part of the cost calculation, in effect raising the threshold higher.

The thresholds will be pegged to inflation plus 1 percent and will automatically go upwards if “health costs rise unexpectedly quickly between now and 2018″ when the tax is set to phase in.

Finally, there will be adjustments in the threshold for businesses that have higher costs due to the gender or age makeup of their employees.

Health Insurance Exchange Design

The President’s plan maintains the state-based exchange design in the Senate bill instead of a more robust, national one [8]. The President proposes giving the Department of Health and Human Services and state regulators the authority and funding to question and block rate increases like we’ve seen recently from Anthem/WellPoint in California.

Igor Volsky at Think Progress has a rundown of what the new policy would do:

The final Senate health care bill already bars insurers with excessive rate hikes from participating in the insurance exchanges but this new provision would go a step further, federalizing the states’ traditional and somewhat uneven role in monitoring insurance rate increases. At least 25 states [12] have some “form of a prior approve process for premium increases,” but state governments often lack the resources or political will to keep insurers in check. Obama’s provision is both politically and substantively significant. It protects consumers from unreasonable rate increases but also prohibits insurers from dramatically increasing rates during the elections of 2010 and 2012 or the period between the passage of comprehensive reform and implementation.

Democrats were worried that insurers would exploit the interim period to boost profits ahead of the new insurance regulations. The federal government’s new rate review powers could blunt at least some of the anticipated increases. Here is how rate review would work:

- Insurance companies would have to justify unreasonable premium increases.

- The Secretary could deny or modify health insurance rate increases that are found to be unjustified.

- The Secretary would determine whether states have the capability to conduct rate reviews.

- Establishes a Health Insurance Rate Authority to advise the Secretary. It will have seven members, including consumer representatives, an insurance industry representative, a physician and other experts like health economists and actuaries

Since conservatives will surely claim that rate review is some kind of government takeover of private industry or a burdensome new federal requirement for insurers, it’s important to note that states that have instituted [the rate review process] house profitable insurance companies and maintain competitive and vibrant markets. Families USA has more on that here.

Public Option

There is no public health insurance option in the President’s bill.

Other Changes

In addition, the President’s plan would:

- fully close the donut hole for prescription drugs under Medicare by 2020

- put more money into community health centers

- some changes in the individual mandate, plus allowing people to opt out of purchasing insurance entirely if they’re below the tax filing threshold of $18,700 per year for families

- gets rid of “pay for delay” which allows branded pharmaceutical companies to keep generics off the market by paying the generic maker to stay out

- $10 billion in more tax on big PhRMA

- fully funds the Medicaid expansion for states until 2017, funds it at 95% until 2019, and funds it at 90% going forward after that

- gets rid of the special deals like Senator Nelson’s cornhusker kickback

- is fully paid for and reduces the deficit over 10 and 20 year periods

Join us in defending the truth before it’s too late

The future of independent journalism is uncertain, and the consequences of losing it are too grave to ignore. To ensure Truthout remains safe, strong, and free, we need to raise $47,000 in the next 8 days. Every dollar raised goes directly toward the costs of producing news you can trust.

Please give what you can — because by supporting us with a tax-deductible donation, you’re not just preserving a source of news, you’re helping to safeguard what’s left of our democracy.