Jessica Patterson tensed as she tore open the letter from Exeter Finance. “This notice is being sent to you concerning your default,” the company wrote.

She didn’t need to keep reading to know she was in trouble.

It was January 2018. Seven months earlier, she’d borrowed $14,786.07 to purchase a silver Kia Rio. The interest rate was sky high — 25.17% — and the $402 monthly payment was more than a quarter of her take-home pay. But she needed the car to keep her job and support her three young children. For months she had skimped on groceries, eaten at soup kitchens and even skipped Christmas gifts to pay the car loan. But most of the time it wasn’t enough, and now Exeter was threatening to seize the Kia.

Panicked, she dialed the number in the letter. Can we work something out, Patterson asked.

Exeter’s response came easily, she recalled. It offered to extend her loan.

The company would simply move the December and January payments to the end of her five-year payment schedule, the representative told her, adding two months to the loan’s term. “It was instant relief,” Patterson said.

The extension seemed to be a courtesy from Exeter in a time of need. In fact, the company’s disclosures at the time stated “Extension fee: $0.00.”

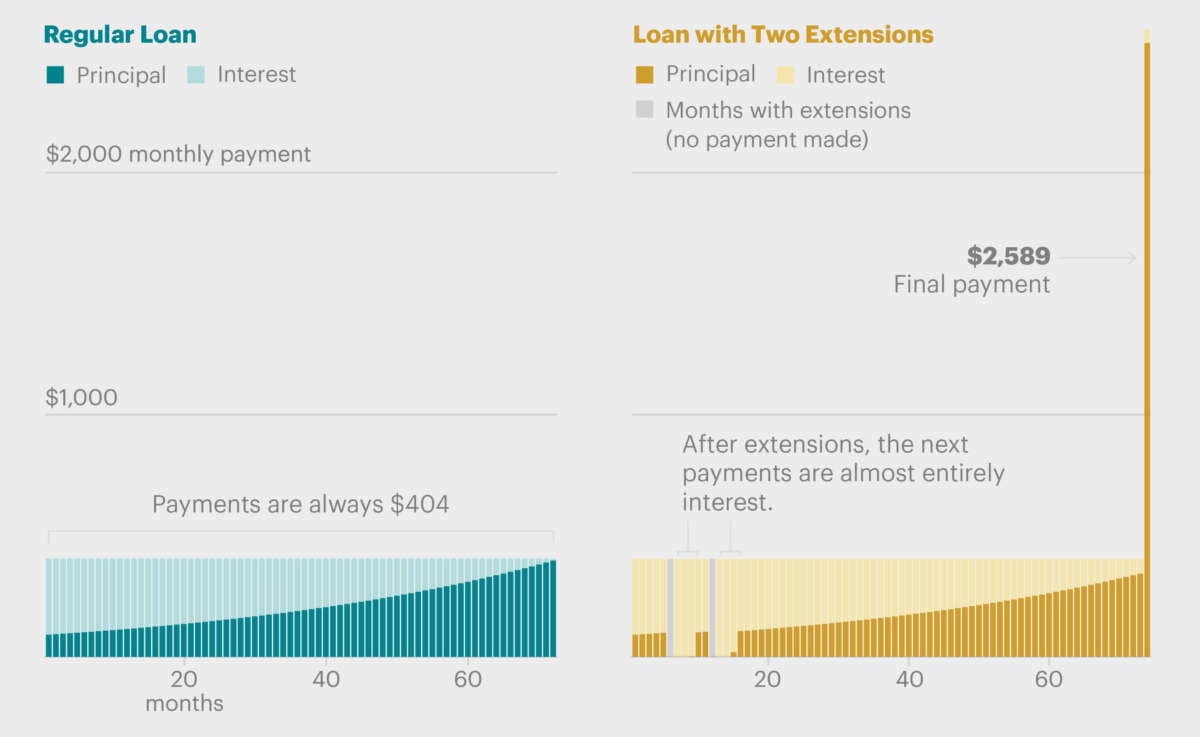

The pause in payments, however, was anything but free. What Patterson didn’t know, and what she said Exeter didn’t tell her, was that every penny of her next five payments would go to the interest that built up during the reprieve. That meant she didn’t pay down the original loan balance at all during that time.

While the extension allowed her to keep her car, it added about $2,000 in new interest charges, which the lender did not clearly disclose.

Patterson’s experience with Exeter was not unusual. A ProPublica investigation has found that it’s an integral part of how the company runs its business.

Exeter is one of the largest auto lenders in the nation, specializing in high-interest loans to people with histories of not paying bills or defaulting on debt, a practice known as subprime lending. The company, which has more than 500,000 active loans and a partnership agreement with CarMax, the country’s largest used car retailer, casts itself as a provider of second chances. “We’re here to help,” it says on its website. In reality, Exeter’s practices often do the opposite.

When the company allows a borrower to skip payments, it typically adds thousands of dollars in new interest charges to the customer’s debt. Dozens of customers told ProPublica that Exeter didn’t tell them about the added costs.

When it’s time to make their final payment, many are faced with a huge bill, which they often can’t afford to pay.

At that point, Exeter often repossesses a car and sends the bill to a debt collector, regulatory records show. In some cases, the company makes more money on loans that default than on ones in which borrowers pay on time, ProPublica found.

Critics, including some former employees, say the company’s practices are predatory. “I really hated extensions once I found out what they did to people,” said Tyhara Ross, who worked at Exeter for nearly nine years. “You think you’re getting something for nothing, and you’re not.”

Exeter’s top executives declined to be interviewed for this story, and the company did not answer detailed written questions. Instead, it issued a statement that said it’s “fully committed to transparency in its lending practices” and “has no reason to mislead customers.”

“Exeter’s mission is to enable Americans who otherwise may not be able to access financing the opportunity to own their own vehicle so they can go to work and take care of their families,” the company said. “We take that mission seriously as well as our commitment to our customers.”

It’s difficult to track just how many extensions Exeter gives out; the company is not required to report detailed numbers. But publicly available data shows they’re fundamental to Exeter’s business model. Lenders often describe extensions in the context of financial emergencies, like when a borrower loses their job, or national crises, like the COVID-19 pandemic. Exeter hands them out “like candy,” according to three former employees who worked in the company’s collections operation.

To examine Exeter’s practices and their effect on borrowers, ProPublica analyzed data on more than 10 million auto loans included in bonds issued in the past five years.

At first blush, Exeter’s portfolio looks dire: A majority of its loans — more than 200,000 — are at least three payments behind schedule — a degree of delinquency that is roughly twice that of any other subprime lender in the data. Many companies would be preparing to count those loans as losses, send them to a collection agency and repossess the cars.

But Exeter has turned what would otherwise be a financial crisis into a profit center. Each time the company grants an extension, it resets the clock and reclassifies the loan as being on schedule. ProPublica found that Exeter has done this as many as 12 times over the course of a 72-month loan, with borrowers continuing to make payments in hopes of catching up. Regulatory records show many customers paid the equivalent of the full loan or more, only to see their cars repossessed.

Federal law prohibits lenders from engaging in “unfair, deceptive or abusive acts,” and the chief enforcer of that law, the Consumer Financial Protection Bureau, took action against Santander Consumer USA, the nation’s largest subprime lender, in 2018 for practices similar to Exeter’s, such as offering loan extensions without clearly disclosing the financial impacts. CFPB forced Santander to pay nearly $12 million in restitution and penalties. But the agency hasn’t taken enforcement action against Exeter. Meanwhile, annual complaints to the CFPB about the company have grown threefold in the past five years, with nearly 900 in 2023.

Extensions that hide the consequences from borrowers “are taking a loan that is not working and ensuring that it’s just not going to work for a little longer,” said Pamela Foohey, a University of Georgia law professor who has written extensively about subprime lending.

Exeter said it made “voluntary revisions” in 2019 “to the way it communicates about extensions to ensure customers are fully informed on the costs,” notably in the scripts its agents use when talking to borrowers. It also said it created a dedicated team that year to handle extensions “with a focus on transparency to customers.”

“Customers are told clearly that interest will continue to accrue during an extension and are given the true cost of the interest accrual so that customers can make a decision on whether to choose an extension,” the company said.

But none of the customers that ProPublica spoke to said that was what they experienced. In fact, more than 20 borrowers told us they were not provided a dollar amount of what their extensions would cost before they agreed to them. “I just felt like that was so wrong,” said Natosha Smith, a former Exeter borrower living in Georgia.

She received eight extensions over the course of her loan. Each time, Smith said, an Exeter employee explained that it added additional months to the end of her loan term. Smith said she expected to pay a little extra interest, something akin to her $425 monthly payment. Instead, the cost was more than 10 times that.

“You guys have gotten double what this vehicle is worth, and you still want to take another $6,000 from me?” Smith said of Exeter. “I was appalled. I couldn’t believe it.”

When asked why it did not provide Smith and others with the exact cost of their extensions, Exeter amended its statement, saying, “Customers who request an extension are given the option before accepting the extension to immediately speak with an agent who can provide the cost of the interest that will accrue during the extension period. Some customers choose not to be transferred to an agent to receive the explanation.”

Neither Smith nor other borrowers could recall being given this option.

Loans With Extensions Result in Inflated Final Payments

Targeting Struggling Buyers

Exeter has always specialized in the subprime market. But in the late 2010s, the company went after customers with poor credit more aggressively than it had in the past. It accepted borrowers with even lower credit scores, lent them more money — as much as $50,000 per loan — and gave them longer to repay it. Some agreed to schedules stretching longer than six years, making the loans more costly.

“We’re not your father’s Exeter Finance,” the company proclaimed in a 2019 blog post aimed at wooing new business from dealerships.

It also increased its prices.

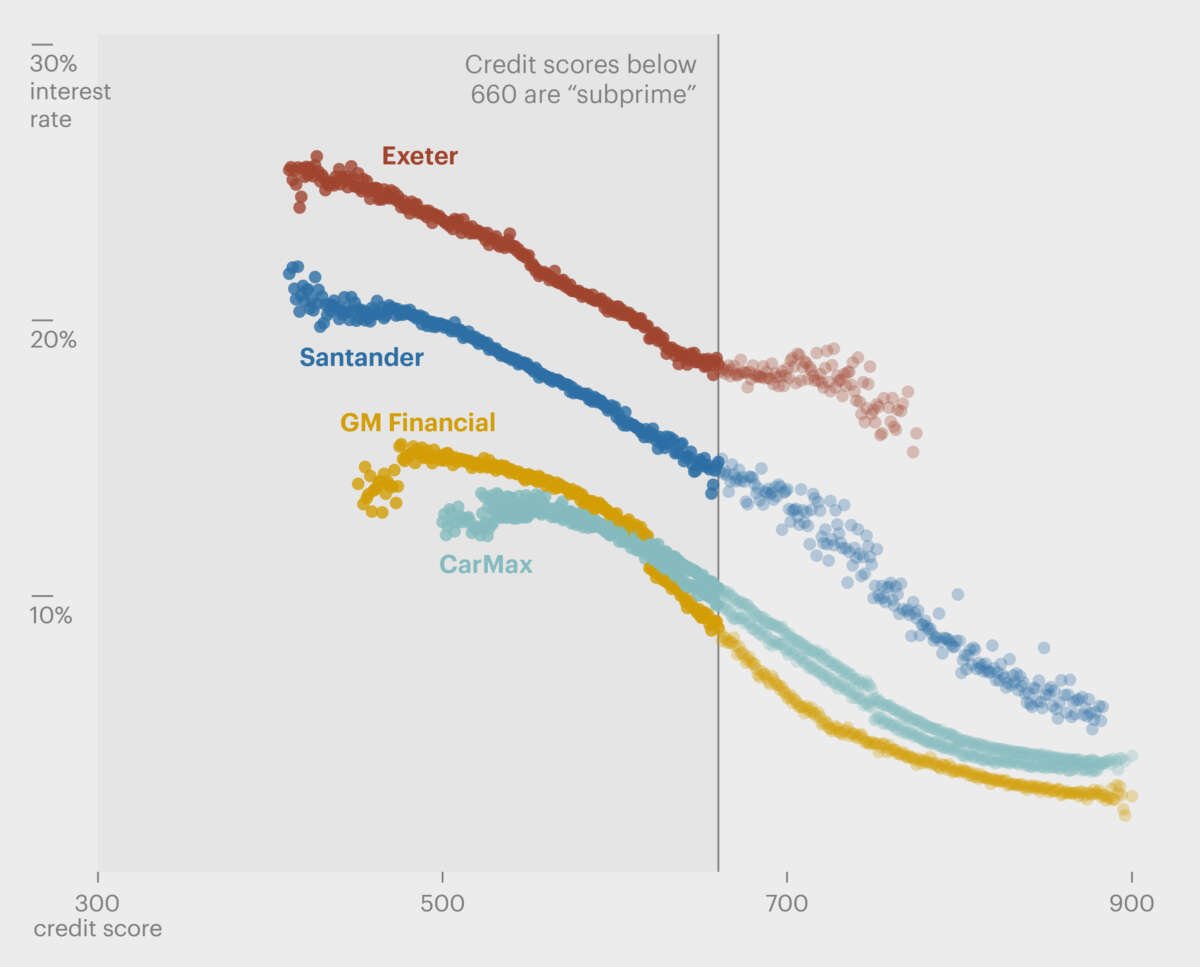

ProPublica’s analysis shows that Exeter charges the highest interest rates of any lender in the publicly available data. Since 2020, the average interest rate for an Exeter car loan jumped from 19% to nearly 22%, regulatory records show.

Exeter Charged Higher Interest Rates Than Other Subprime Lenders

Exeter’s loan volume exploded, bond data shows. And as borrowers got into trouble, the lender’s collections workers were rewarded with bonuses for getting loans out of delinquency, according to three former employees. Extensions were a common tool to accomplish that. Exeter denied the allegation, saying, “customer service agents are not incentivized or rewarded with compensation related to granting extensions.”

Either way, Exeter financial records show the number of loans with five or more extensions rocketed 80% between 2016 and 2018.

The company attributed part of a more recent uptick in extensions to the COVID-19 relief bill that Congress passed during the pandemic in 2020, saying the legislation “encouraged compassion from lenders.”

That “compassion,” however, led to confusion and anger among borrowers who began filing complaints with state attorneys general. ProPublica examined nearly 200 of them and found the most common problems involved how much of their payments went to interest and why they still owed so much.

The company has drawn the scrutiny of regulators in at least three states. In 2019, the attorneys general of Massachusetts and Delaware settled lawsuits against Exeter alleging it had violated consumer protection laws. The company said the settlements had nothing to do with extensions and contained no admission of illegality. The Georgia attorney general’s office confirmed it is now investigating Exeter, though it declined to provide more detail. Exeter declined to comment on the investigation.

The CFPB declined to answer questions about Exeter’s practices and its oversight of the company. Chris Kukla, a CFPB program manager supervising the auto finance industry, said that in general “it’s important for everybody to understand what’s going on in the transaction.”

“All the information should be shared,” he added.

For years, Exeter failed to provide specific information in its written notices. They did not explain that a borrower’s next payments would first be applied to the interest from extensions, which would delay repayment of the original loan balance, known as the principal. These omissions were identical to those that federal regulators had targeted in their case against Santander years earlier, according to three consumer finance experts who reviewed them.

The company said it updated those disclosures in late 2021 but declined to provide copies or details about the changes.

Notices sent to borrowers earlier this year, reviewed by ProPublica, said that an extension would increase the borrowers’ interest charges as well as the amount of their final payment. However, the notices did not include the actual dollar amount. If borrowers wanted to know more, the letter directed them to call a toll-free number.

One employee said that lack of disclosure was intentional.

“The object was for the agent to keep the customer in the car no matter what,” said Ross, the former Exeter employee who worked with borrowers struggling to make their payments. “That’s the end game. Because as long as that customer stays in that car, guess what? They are getting that interest. And the interest brings them more money.”

Lender of Last Resort

Jessica Patterson encountered Exeter like tens of thousands of consumers do each year: via CarMax, which uses Exeter to make loans when borrowers don’t qualify for CarMax’s in-house financing.

In the spring of 2017, Patterson sat at a circular table in her local CarMax just outside Kansas City, Kansas, with $200 in her pocket. Around her was an open sales room nearly as deep and wide as a football field.

A salesperson had shown her a Kia Rio with low mileage and zero frills. At $15,000, it was “the best that I could do for what I had,” Patterson recalled.

As a receptionist at a hearing aid sales center, she made $12 an hour, below the federal poverty line. She’d just moved her family out of a domestic violence shelter and into a basement apartment of their own. Their life felt fragile.

Like most subprime customers, her credit history was rife with unpaid bills. The debts were mostly from her ex-husband, she said.

The CarMax employee said she had good news, though: Exeter would lend Patterson the full amount needed to buy the Kia. Then the employee read the loan terms aloud. A six-year loan. A 25.17% interest rate. A monthly payment of $402.63. That would be a quarter of Patterson’s take-home pay, almost twice what consumer finance experts recommend.

She asked whether there were cheaper offers. None of the other companies were willing to give Patterson a loan, said the employee, who turned her computer monitor so Patterson could see. “Exeter was the only one there,” she said. According to rating agency reports, CarMax is the single largest source of Exeter’s business — responsible for some 50,000 loans per year.

Patterson agreed to the terms. To get to work and get her kids to school, she needed a car. Turning down the loan felt like giving up.

Exeter contacted her employer and landlord to confirm the details in her application. It knew how much money Patterson would get in her upcoming paychecks, how much would automatically go out and how little room for error she had.

For its part, CarMax said it is not involved with the loans Exeter and other lenders sell to its customers and declined to answer specific questions about its partnership with Exeter.

“Each of CarMax’s finance sources performs its own underwriting, servicing, and collection activity,” the dealership chain said in a written statement. “CarMax cannot speak to details about how our finance sources manage repossessions or extend financing.”

Truth in Lending?

The top of Patterson’s contract had a box detailing just how much she would pay over six years — a requirement of the federal Truth in Lending Act. It said she’d pay Exeter more than $14,000 in interest, almost as much as she would pay for the Kia itself.

While it would be tight, Patterson thought she could budget for the loan.

Within months, though, she fell behind. In January 2018, Patterson took her first two extensions. She used the time to reorder her finances so she could resume payments.

To save on food, she drove her family to free church dinners every Wednesday and Thursday night. Donations from a nearby food bank allowed them to keep grocery bills at a bare minimum.

Patterson sent payments to Exeter for February and March. But by late spring, she was in trouble again, resorting to sending a few hundred dollars at a time. By the fall, she was on the verge of default.

She called the lender’s collections department and asked for a third extension. The lender granted it over the phone without question, Patterson said.

Exeter agents could see the exact cost of the added interest on their screens during calls like this, but they did not share it with borrowers, said Clair Groves, who worked in Exeter’s collections department in 2019. The company does not include specific price information in the scripts it requires agents to read when giving an extension, Groves said, and urges them to finish calls in less than three minutes, leaving little time to provide more information.

Exeter did not respond to questions about Patterson’s account or Groves’ statements.

Extension practices like Exeter’s, experts say, undermine the utility of the Truth in Lending law, which aimed to eliminate financial surprises for consumers.

“If you can manipulate the payment schedule in such a way that makes the original disclosures meaningless, that’s a huge problem,” said Erin Witte, consumer protection director at the Consumer Federation of America.

For Patterson, the true cost of the extensions would become clear only after she remarried two and a half years later. Her new husband, Andrew Patterson, had found the Exeter loan odd. He had bought a more expensive car from the same dealership, but because he qualified for a loan from CarMax directly, his monthly payments were far lower. He decided to take a closer look.

The numbers on her statements were staggering, he said. Even when she made payments consistently, so much money went to interest that she barely made a dent in the original debt. If they made the 20 remaining payments, there was still no way they’d be able to pay off the car.

Using her loan statements, ProPublica calculated that Patterson had paid Exeter $17,097 over three years. About 80% of that had gone to interest, leaving her with more than $11,000 in debt.

“Just let them repo it,” Andrew told his wife.

The lender seized the Kia in the fall of 2021 and auctioned it off for $13,800. Exeter collected more from Patterson’s failed loan than it would have if she’d paid on schedule.

A Giant Bill, Then Repossession

ProPublica’s analysis found that nearly a quarter of Exeter loans from 2020 and 2021 — more than 65,000 — ended like Patterson’s did, with borrowers stopping repayment early.

For people who take extensions and make it to the end of their loan, a large final payment typically awaits.

That news was crushing for Don Weaver, a disabled veteran living in Louisiana. In 2015, Exeter lent him $15,607.29 to buy a 7-year-old GMC Envoy. Over the next seven years, the company granted him 12 extensions by phone, Weaver said. Each time, the agent assured him he was “current,” he recalled.

The extensions had helped him navigate choppy economic waters, he said. He lived off VA disability payments, and unexpected expenses like a busted lawn mower or worn-down brake pads often made his $393.14 monthly payment difficult.

In September 2022, after Weaver had paid Exeter $29,125 — $819 more than his loan contract outlined — the company told him he still owed more than $9,000.

“I couldn’t get heads or tails about how much of that was actual payments and how much of that was fees,” Weaver said.

When he couldn’t pay, Exeter repossessed the Envoy, and today, a collections company is pursuing him for the $5,800.73 he still owes.

Although their loan outcomes were different, both Weaver and Patterson felt certain that local authorities should know about their experiences. Exeter “has a huge role in allegedly financing unfair, subprime auto loans,” Patterson wrote to Kansas Attorney General Derek Schmidt in November 2021. “They are a predatory company.”

Weaver’s complaint was strikingly similar, citing the settlements Exeter had entered into with Massachusetts and Delaware: “They had to pay millions back to consumers due to predatory practices,” he wrote to Louisiana Attorney General Jeff Landry. “I am wondering if that is happening to me.”

Kansas simply forwarded Patterson’s complaint to Exeter, which responded with a letter claiming that all the contract terms were properly disclosed; five extensions were granted “at Jessica’s request.” Months after it repossessed her Kia, Exeter added, it stopped pursuing her, “as a courtesy,” for the $51.63 she still owed.

Louisiana regulators didn’t press Exeter in Weaver’s case, either. After receiving a similar explanation from the lender, the attorney general’s office ended its inquiry, encouraging Weaver to hire a lawyer if Exeter’s response “does not result in a satisfactory outcome for you.”

The attorney general’s office confirmed that it did not investigate Weaver’s case. Landry, who is now governor of Louisiana, did not respond to requests for comment. The Kansas attorney general’s office also declined to comment.

In the fall of 2022, even with the bill collector after him, Weaver still needed a car. So, he headed to a nearby CarMax to start the process over. When the employee ran his information, he was told that Exeter had approved him for another loan.

“You’re telling me you got to charge me this extra interest and all this because I’m a bad risk,” Weaver said, “but you’re willing to risk it again?”

This time, he declined the offer.

Disclosure: The private equity firm Warburg Pincus owns a controlling stake in Exeter. Mark Colodny, one of the firm’s managing directors, is a member of ProPublica’s board.

Jeff Ernsthausen and Mollie Simon of ProPublica and Carrie Cochran and Patrick Terpstra of Scripps News contributed reporting.

Trump is busy getting ready for Day One of his presidency – but so is Truthout.

Trump has made it no secret that he is planning a demolition-style attack on both specific communities and democracy as a whole, beginning on his first day in office. With over 25 executive orders and directives queued up for January 20, he’s promised to “launch the largest deportation program in American history,” roll back anti-discrimination protections for transgender students, and implement a “drill, drill, drill” approach to ramp up oil and gas extraction.

Organizations like Truthout are also being threatened by legislation like HR 9495, the “nonprofit killer bill” that would allow the Treasury Secretary to declare any nonprofit a “terrorist-supporting organization” and strip its tax-exempt status without due process. Progressive media like Truthout that has courageously focused on reporting on Israel’s genocide in Gaza are in the bill’s crosshairs.

As journalists, we have a responsibility to look at hard realities and communicate them to you. We hope that you, like us, can use this information to prepare for what’s to come.

And if you feel uncertain about what to do in the face of a second Trump administration, we invite you to be an indispensable part of Truthout’s preparations.

In addition to covering the widespread onslaught of draconian policy, we’re shoring up our resources for what might come next for progressive media: bad-faith lawsuits from far-right ghouls, legislation that seeks to strip us of our ability to receive tax-deductible donations, and further throttling of our reach on social media platforms owned by Trump’s sycophants.

We’re preparing right now for Trump’s Day One: building a brave coalition of movement media; reaching out to the activists, academics, and thinkers we trust to shine a light on the inner workings of authoritarianism; and planning to use journalism as a tool to equip movements to protect the people, lands, and principles most vulnerable to Trump’s destruction.

We urgently need your help to prepare. As you know, our December fundraiser is our most important of the year and will determine the scale of work we’ll be able to do in 2025. We’ve set two goals: to raise $150,000 in one-time donations and to add 1,500 new monthly donors.

Today, we’re asking all of our readers to start a monthly donation or make a one-time donation – as a commitment to stand with us on day one of Trump’s presidency, and every day after that, as we produce journalism that combats authoritarianism, censorship, injustice, and misinformation. You’re an essential part of our future – please join the movement by making a tax-deductible donation today.

If you have the means to make a substantial gift, please dig deep during this critical time!

With gratitude and resolve,

Maya, Negin, Saima, and Ziggy